It’s a mixed bag when it comes to calling a recession for the U.S. economy sometime this year. Most economists still see a recession as the U.S. Federal Reserve sends signals of more interest rate hikes to decelerate inflation.

The good news is people are working and unemployment is low. Also, consumers have continued to spend—more recently on services, but the buying of goods, in particular durable goods like big-ticket items including appliances and cars, could slow down. That would be a positive because it would help drive slower inflation.

The bad news is many risks remain. Food prices, for instance, remain high and could fuel faster inflation. China’s resumption of economic activity post-COVID could mean a spike in energy prices and also accelerate inflation. The weakening of the U.S. dollar is also a concern.

The ugly situation revolves around the debate about the national debt and debt ceiling. Should a resolution be elusive, it could have a profound negative impact on the prospects for a robust recovery and result in negative economic growth.

Breaking it all down

The present situation, according to The Conference Board isn’t terrible in the eyes of consumers—the main driver—but their expectations are shaky. And these worsening expectations are dragging down the more favorable view of the current situation.

Specifically, The Conference Board Consumer Confidence Index® decreased in February for the second consecutive month. The Index now stands at 102.9 (1985=100), down from 106.0 in January (a downward revision). The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—increased to 152.8 (1985=100) from 151.1 last month. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions—fell further to 69.7 (1985=100) from a downwardly revised 76.0 in January.

Notably, the Expectations Index has now fallen well below 80—the level which often signals a recession within the next year. It has been below this level for 11 of the last 12 months.

“Consumer confidence declined again in February. The decrease reflected large drops in confidence for households aged 35 to 54 and for households earning $35,000 or more,” said Ataman Ozyildirim, Senior Director, Economics at The Conference Board. “While consumers’ view of current business conditions worsened in February, the Present Situation Index still ticked up slightly based on a more favorable view of the availability of jobs,” Ozyildirim added. “In fact, the proportion of consumers saying jobs are ‘plentiful’ climbed to 52.0%—back to levels seen in the spring of last year. However, the outlook appears considerably more pessimistic when looking ahead. Expectations for where jobs, incomes, and business conditions are headed over the next six months all fell sharply in February.”

“While consumers’ view of current business conditions worsened in February, the Present Situation Index still ticked up slightly based on a more favorable view of the availability of jobs,” Ozyildirim added. “In fact, the proportion of consumers saying jobs are ‘plentiful’ climbed to 52.0%—back to levels seen in the spring of last year. However, the outlook appears considerably more pessimistic when looking ahead. Expectations for where jobs, incomes, and business conditions are headed over the next six months all fell sharply in February.”

Also, at the end of February, The Conference Board acknowledged that 12-month inflation expectations improved—falling to 6.3% from 6.7% last month. It said consumers may be showing early signs of pulling back spending in the face of high prices and rising interest rates.

“Fewer consumers are planning to purchase homes or autos and they also appear to be scaling back plans to buy major appliances. Vacation intentions also declined in February,” Ozyildirim cautioned.

Specifically, as far as the present situation, 17.8% of consumers said business conditions were “good,” down from 19.9%, while 17.7% said business conditions were “bad,” down from 19.0%.

Consumers’ appraisal of the labor market was consistently more favorable: 52.0% of consumers said jobs were “plentiful,” up from 48.1%, and 10.5% of consumers said jobs were “hard to get,” down from 11.1%.

But when assessing business conditions six months ahead, consumers at the end of February were more pessimistic about the short-term outlook.

Just 14.2% of consumers expect business conditions to improve, down from 18.4%. And 21.9% expect business conditions to worsen, down from 22.6%.

In looking ahead, consumers were also less upbeat about the short-term labor market outlook. Only 14.5% of consumers expect more jobs to be available, down from 17.7%. Yet, 20.3% anticipate fewer jobs, down from 21.4%.

Consumers’ short-term income prospects also were considerably less upbeat in February: 13.4% of consumers expect their incomes to increase, down from 17.4% last month, and 11.6% expect their incomes will decrease, down from 13.4% last month.

The monthly Consumer Confidence Survey® is based on an online sample, and is conducted for The Conference Board by Toluna, a technology company that delivers real-time consumer insights and market research through its innovative technology, expertise, and panel of more than 36 million consumers.

Different than other recessions

In a media briefing preceding the release of its latest Consumer Confidence Survey®, Conference Board economists pointed to the indicators that are still flashing signs of a recession.

So, is the U.S. in a recession or not?

“That’s the question of the day,” said Dana Peterson, chief economist at The Conference Board. “And if we are, what might it look like?” She said a recession this time is different from others, primarily because the labor market is robust. Other key questions revolve around how the Fed will manage monetary policy this year and next, and what are the other main risks.

“Our own leading economic indicators suggest that if we are going to have a recession it's probably starting right about now – February, March or even later at the beginning of the second quarter,” Peterson said.

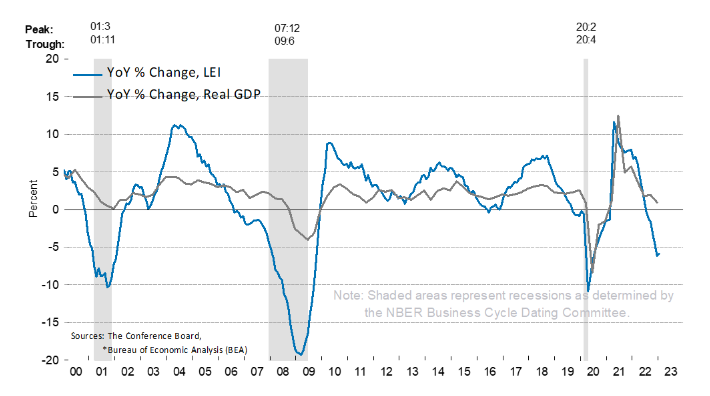

In pointing to the above chart, Peterson emphasized that the leading economic indicators on a year over year basis show that when the change drops below 5%, it pretty much matches up with when the recession will start.

In pointing to the above chart, Peterson emphasized that the leading economic indicators on a year over year basis show that when the change drops below 5%, it pretty much matches up with when the recession will start.

Fact is, the recession warning signal has been flashing red since March of last year.  “When we look at our LEI in different ways it tends to signal when there's going to be a recession,” Peterson explained. “The light blue line is essentially the 6-month change in the LEI and whenever it falls below 4% it sends out a warning signal that maybe there's a recession coming—and it fell below 4% in March of last year and it's been below 4% ever since.”

“When we look at our LEI in different ways it tends to signal when there's going to be a recession,” Peterson explained. “The light blue line is essentially the 6-month change in the LEI and whenever it falls below 4% it sends out a warning signal that maybe there's a recession coming—and it fell below 4% in March of last year and it's been below 4% ever since.”

But The Conference Board has also been getting a red recession signal from its diffusion index—a reflection of how many of the indicators of are above or below zero.

“Whenever this diffusion index falls below 50, and also you have a -4% growth rate on the 6 month change in the LEI that's the red recession signal and essentially it's been signaling a recession at some point for a year now,” Peterson added.

The good news, according to Peterson, if there is a recession it will probably be short.

“It’s likely to be shallow, maybe will start in the first quarter and perhaps more pronounced in the second quarter—but we are not anticipating major declines in GDP growth; instead we're defining this more as domestic demand growth turning negative.”

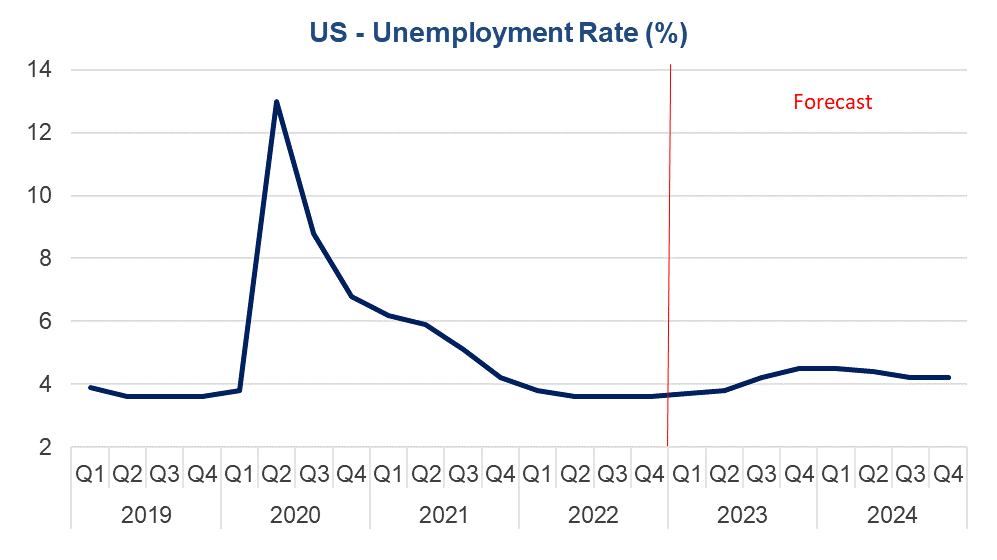

And even though The Conference Board is expecting a short and shallow recession in the U.S., The Conference Board does not see material deterioration in the labor market.

“You could see the unemployment rate rise to as high as 4.5% (it was 3.4% in January), and then just kind of hang there, which is really right around the neutral rate,” Peterson said. “So, we would still experience a very tight labor market even with a 4.5% unemployment rate, which is roughly equivalent to about 900,000 jobs.” Labor shortages will continue to squeeze the labor market overall, according to The Conference Board.

Peterson noted that Baby Boomers are retiring, a trend that is shrinking the overall working-age population. What’s more, the lingering effects of the pandemic are suppressing labor force participation.

Debt Ceiling Debate

In terms of Washington policy, the debt ceiling debate this year is looming as critical.

“The reason why the debt ceiling debate is so important this year is because of the vulnerability of the U.S. economy and the global economy as far as a recovery,” said Dr. Lori Esposito Murray, president of the Committee for Economic Development at the public policy center of The Conference Board.

Dealing with inflation, hoping to avert a recession and spark economic growth are all critical, but Esposito Murray emphasized that the debt ceiling debate is the “most front and center issue that can actually disrupt the entire apple cart.”

“On the one hand, it's similar to where we were in 2011 when a number of lessons were learned,” she explained. “One of the most important was even the debate itself, as it gets close to the cliff, is disrupted.”

Esposito Murray recalled that in 2011 the downgrading of the U.S. credit rating came not because we went off the cliff, but because the debate itself sparked fear that would happen, which then has ripple effects throughout the economy.

“It’s very easy, basically, to have the crisis and hit the cliff, but it’s much harder to recover from it,” she said, noting that if the crisis is extended for three or four months it could have serious impact on gross domestic product (GDP).

Other lessons from 2011 include the fact that Republicans in the House had a stronger majority and a mandate. “So, looking at this debate and where it goes and how it gets resolved is more complicated with today’s more divided Congress,” Esposito Murray noted.

She said given the fragility of the Republican caucus in the current Congress, it’s a tough situation, even though Speaker Kevin McCarthy has stated he does not want to do into default.

“So then the question becomes what can he (McCarthy) deliver that will meet the spending decreases they want to see happen, which will keep enough of his caucus together,” Esposito Murray noted.

Some observers have pushed the idea of a trillion-dollar coin to help avert the debt ceiling crisis. Simply put, there’s an obscure law that would presumably let the U.S. Treasury mint a special coin for depositing in the Federal Reserve that would prevent the nation from defaulting on its debt.

But Esposito Murray sees that as a form of just kicking the can down road. What happens with the next crisis? Just keep minting coins?

“The trillion-dollar coin idea doesn’t solve the real problem,” she said. “We need to get our fiscal house in order.”

An inflation tug-of-war

Any recession will be driven by the Fed’s tightening policy in an effort to bring down inflation, according to The Conference Board. But Peterson pointed out that two or three more 25 basis-point interest rate hikes are likely and that the Fed will probably keep the terminal rate fixed for the rest of this year. “Considering any interest rate cut is unlikely until early 2024,” she said.

The good news is inflation has peaked. The Conference Board expects prices to decelerate the rest of this year and into 2024, but the Fed’s 2% inflation target will probably not be achieved until the end of 2024.

The primary drivers of still-lofty inflation are housing costs and strong consumer demand for post-pandemic services, according to The Conference Board. In short, people want to get out and do things, which drives prices higher.

Helping to push inflation lower: home price valuations have peaked and are slowing, and new rents are lower than during the pandemic.

“This bodes well for consumer inflation gauges ahead,” Peterson said.

Nonetheless, there are several inflationary risks and uncertainties. For instance, will food prices remain sticky? The war in Ukraine, flooding and droughts, avian flus and other events have stoked higher food prices. China’s post-pandemic reopening could increase consumption of services and energy—and any spike in China’s demand for oil could raise prices and add to global inflation.

If U.S. consumers continue to spend, however, inflation could linger and even accelerate. The Conference Board noted that consumer spending slowed in November and December, but that warmer-than-expected weather may have meant strong consumption in January.

The U.S. Economy: The Good, the Bad and the Ugly