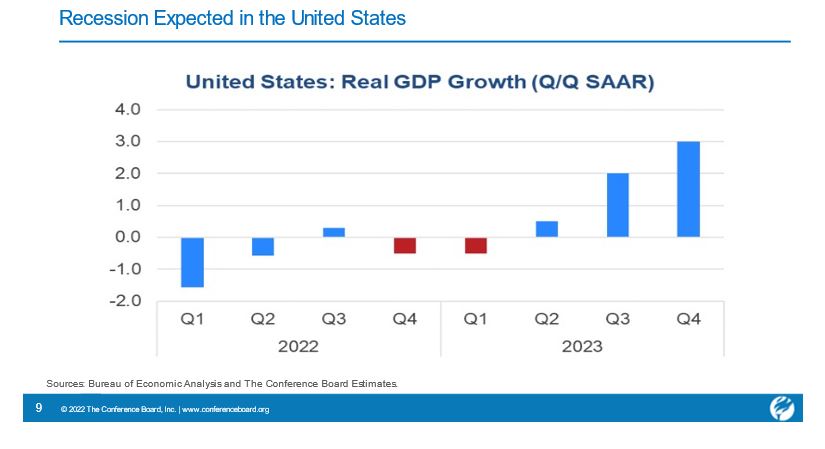

A recession is expected in the United States starting in the fourth quarter, according to The Conference Board, but it is forecast to be brief and shallow. There are risks, however, of a global recession.

Among the megatrends highlighted by The Conference Board are the pandemic and the war in Ukraine, which continue to dominate its outlook. Others include supply chain disruptions and inflation, central banks tightening monetary policy, and the impact of the lingering pandemic and demographics on labor markets.

“You can look at this from top down in terms of what can cause recessions in individual economies or bottom up in terms of what might cause a global recession,” Dana Peterson, chief economist at The Conference Board, explained during a media briefing in mid-September. “We don't see a global recession, but we do expect that there will be recessions – brief and shallow – in both Europe and the United States.”

She explained that the Federal Reserve’s actions to tackle inflation and to return key price gauges back to a 2% inflation target will push the U.S. into a recession.

“Our own forecast is for the Fed to raise its funds rate to the range of 3.75 to 4% with a midpoint of 3.758%, and that we think is going to cause the U.S. to go into recession,” Peterson said. “We're already seeing weakening in activities, certainly in housing and consumer spending.”

As such, The Conference Board is forecasting negative real GDP growth for the U.S. (seasonally adjusted annual rate, quarter-over-quarter) in Q4 2022 and Q1 2023 of about -0.5%, but then improving in Q2 (+0.5), Q3 (+2.0) and Q4 (+3.0) next year.

Erik Lundh, US economist at The Conference Board noted that retail sales and consumer spending on services – rather than goods – has been holding up a lot more than most observers expected.

“But we are really concerned about the fourth quarter and the first quarter of next year,” he said. “So, what we're envisioning at this point is a brief and mild recession,” Lundh added, “And once that period elapses, the U.S. economy should start to expand again towards the tail half of 2023.”

Both Peterson and Lundh caution that there are several major risks to the forecast. In the U.S. case, there is the possibility that the Federal Reserve will tighten monetary policy more than anticipated and that inflation will not abate as expected.

“The housing market is a big question mark in terms of whether or not we see a meaningful decline in prices,” Lundh said.

Government spending is also a wild card. “We're concerned about the rolling out of some of the infrastructure spending that was passed last year,” Lundh added. “We're expecting that to probably happen towards the end of this year and early next; but if that's delayed, it could mean downward pressure on our forecast as well.”

There is the possibility of a stronger upside too—should inflation in the U.S. start to fall more rapidly than predicted, according to Lundh.

Global Outlook

The group’s recessionary outlook is virtually the same for Europe, where it sees negative real GDP growth of about -0.6% and -0.5% in Q4 2022 and Q1 2023, respectively.

Europe’s recession also fades by Q2 next year, but The Conference Board expects slower positive growth than in the U.S. (Q2 about 0.5%, Q3 0.75%, and then sliding back to about 0.2% in Q4).

And what about a possible global recession? Peterson says to keep an eye on the economies of Europe, China, and the U.S.

“Together, these areas constitute roughly 55% of global GDP,” she said. “So, if these three economies descend and have troubles, that could cause the entire global economy to go into recession.”

Peterson pointed out that Ukraine and a Russia are already in recessions. While The Conference Board expects slow growth for China, it thinks the country may avoid a recession.

“We see China’s growth for next year well below their pre-pandemic growth rate,” she said. “But we’re still also very concerned about shortages – including in raw materials, food, energy, labor and other things that may be inflationary going forward.”

The housing market correction in China is largely behind its slowing growth and could also lead to a recession.

“We're not expecting a financial crisis associated with that, but of course, it's weighing on the housing market and consumer spending and activity.” Peterson explained. “Then you have repeated waves of COVID-19 and lockdowns,” she added. “We don't anticipate that there will be much softening in this policy until sometime next year, potentially as China is able to produce and distribute its own so vaccines,” Peterson said. “But with each of these lockdowns, it weighs on consumer spending, particularly services.”

Overall, there are three key paths to a global recession, according to The Conference Board: a recession trifecta (in China, Europe, and the U.S), escalation of the war in Ukraine, and intensified global food and energy shortages.

“We're very concerned about the escalation of the war in Ukraine,” Peterson said, noting that Europe’s energy crisis is related to that because it’s a function of Russia turning off its supply of natural gas due to sanctions on its economy.

Another key global risk is around environmental progress.

“I would say that Europe is pushing forward with greening whereas in the U.S. it's been a mixed reaction, like mainly going in the opposite direction where we're looking to increase our production of fossil fuels,” Peterson said.

“The Conference Board's view is that the energy transition is inevitable,” she emphasized. “But it's not going to happen overnight, and some of the 2035 and 2050 milestones may not necessarily be reached.”

Peterson added: “The process will be one of fits and starts. You're going to need a mix of energy sources because you just don't have enough supply of the renewables yet, and that this is going to be expensive. But in the longer run, hopefully, [greening] should be deflationary and beneficial for the global economy.”

For more information, visit: www.conferenceboard.org