Investors forge a comprehensive response

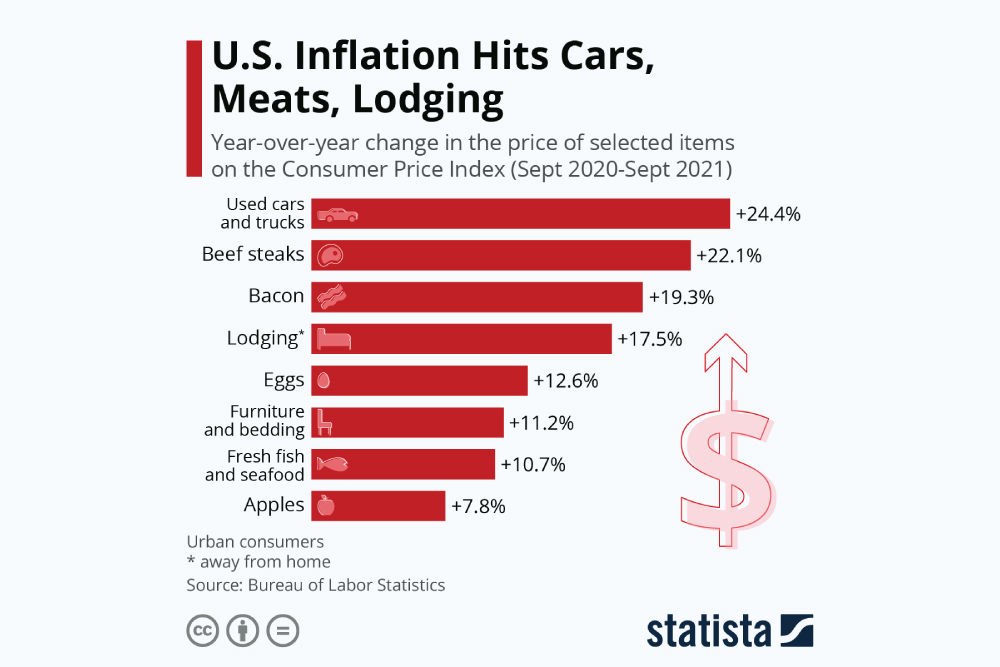

Even before energy prices began their upward spiral or the US Congress passed its enormous infrastructure spending and tax increases, countless news sources were signaling: inflation is here to stay. For example, a July survey of economists by the Wall Street Journal concluded that “Americans should brace themselves for several years of higher inflation than they’ve seen in decades.”

A potentially worsening scenario

Sean Cooper, CFA, CFP® and president at Fit Financial Consulting LLC in Wenatchee, WA agrees, saying “inflation is already here, and then given another round of massive government spending, things are likely to get worse before it gets better. In fact, my greatest concern at this point would be a combination of high inflation in conjunction with a recession.” So the question becomes, how should investors, especially those soon to retire, respond? And the answer is: they need to reevaluate their retirement glide paths to reflect this new reality. Matters are not desperate, but financial plans formulated in a low inflation environment definitely require reassessment and adjustment in this newly inflationary era.

So the question becomes, how should investors, especially those soon to retire, respond? And the answer is: they need to reevaluate their retirement glide paths to reflect this new reality. Matters are not desperate, but financial plans formulated in a low inflation environment definitely require reassessment and adjustment in this newly inflationary era.

Even so, options are limited. “Traditionally, says Cooper, “there are several asset classes that perform well as hedges to inflation including equities, real estate, natural resources/commodities, and Treasury Inflation Protected Securities (TIPS). These asset classes can help investors outpace, or at least better keep pace, with inflation.”

That said, “both equities and real estate are already overheated and relatively overvalued,” says Cooper. “Even many commodities have already experienced outsized returns, like timber, which is already midway through a pullback correction. Conversely, TIPS offer such a low yield currently that they are not all that attractive either.”

Overall, continues Cooper, “While the working class will see some wage increases and even have upward mobility in their job hunts to partially offset inflation, the impact of reduced purchasing power and a resulting lower standard of living will be most keenly felt by fixed income retirees and lower income earners.”

What is the best approach?

What this calls for, says John W. Olson, CFP®, MBA and president at 2250 Financial Services Inc. in Millersville, MD, is a comprehensive response. As Olson explains, “Comprehensive financial planning tends to help clients weather any storm, whether it is inflation, COVID, or any other personal experiences. If I do my best to help clients invest for the long term, save for emergencies, and have the appropriate amounts of life, disability, long-term care and health insurance to allow them to meet their goals and face the risks in their lives, then they will be as ready as they can for whatever happens.” The same applies to business operations; some of the products and reasoning differs, but the logic remains the same – figure out your goals and risks and plan for those with the appropriate tools.

The same applies to business operations; some of the products and reasoning differs, but the logic remains the same – figure out your goals and risks and plan for those with the appropriate tools.

Adjustments to personal financial plans could range from accelerating current levels of saving and investing to delaying retirement. Soon-to-be retirees should also consider downsizing their home or moving to location with a lower cost of living with less real estate tax. The inflation environment has shifted; soon-to-be retirees needs a comprehensive response.

What about my business?

Of course, many of those planning to retire soon are also small business owners. Garrett Boorojian is CDO and Managing Partner at WaveCapital Partners, a group with offices nationwide and focusing on structured financing solutions a wide range of business needs. For small business owners on the path to retirement, Boorojian offers a handful of suggestions for adjusting to inflation.  “I advise my clients as small business owners, that in the face of increased inflation, stagflation, or shrinkflation occur, be careful not to try to grow and expand their companies too quickly. Moving too far or too fast can become a detriment to their businesses’ reserves and personal savings. So it’s important for my clients to be selective regarding how much money they spend or borrow. Buying power during inflation is lower and the increase in the monetary supply is not sustainable in the long-run.”

“I advise my clients as small business owners, that in the face of increased inflation, stagflation, or shrinkflation occur, be careful not to try to grow and expand their companies too quickly. Moving too far or too fast can become a detriment to their businesses’ reserves and personal savings. So it’s important for my clients to be selective regarding how much money they spend or borrow. Buying power during inflation is lower and the increase in the monetary supply is not sustainable in the long-run.”

Alongside inflation, small businesses are also incurring labor and materials shortages. Here, says Boorojian, “where clients are currently dealing with certain price points of goods and services for their companies to offer to their clients, upsetting those metrics one way or another could jeopardize my clients’ reputations.” Small business owners need to be aware “that if the quality of services or products go down, or if they become too expensive, my clients’ clientele might look elsewhere to their competitors. I am advising my clients to try to avoid these scenarios.”

Inflation is a genuine concern for today’s investors on the glide path to retirement. Beyond that shared above, what can you add to the discussion? We’d love to hear at This email address is being protected from spambots. You need JavaScript enabled to view it..