Poor Money Knowledge Challenges Young People

As young Americans continue to struggle with financial literacy, the lack of preparation for making sound money management decisions increasingly threatens their future prosperity and happiness.

“Financial literacy is a 21st century survival skill,” said Jonathan Brandt, CFP®, RIA at Journey Tree Financial Planning and Investments in Eugene, Oregon. “Financial planning is such an important aspect of personal financial wellness and – just like learning any other good behavior – it should be learned at a young age.“

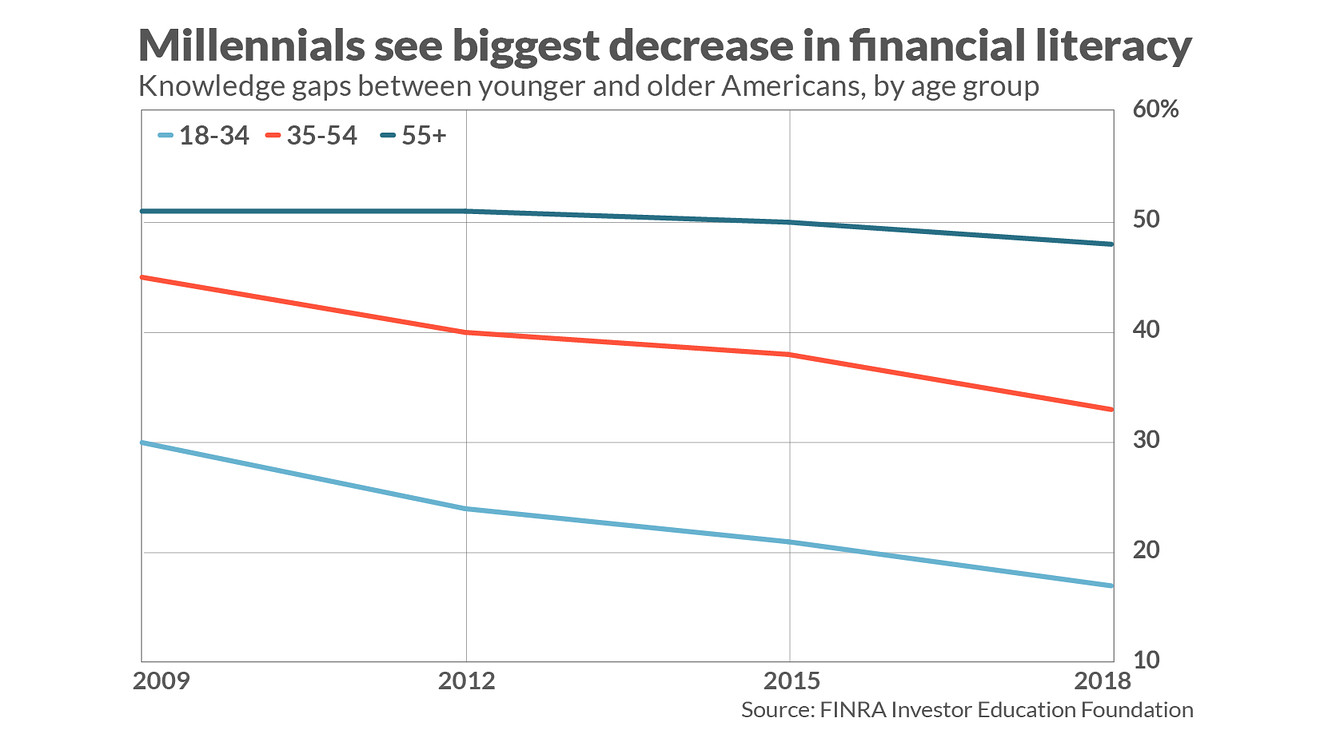

A recent study by the FINRA Investor Education Foundation found the sharpest decline in financial literacy over the past decade occurred among 18- to 34-year-olds. The number of young Americans who could answer four out of five basic financial literary questions correctly fell from 30 percent in 2009 to 17 percent by 2019. Over the same period, 34 percent of the 27,000 people surveyed answered correctly, including more than 50 percent of those ages 55 and older. Another study by consulting firm PwC placed financial literacy among millennials at 24 percent. “Education and collaboration with young adults, and even teenagers, is vital to put them on the right path and empower them to make smart financial decisions,” Brandt added. “If they have the appropriate toolbox, they can face difficult financial decisions and come out relatively unscathed.”

“Education and collaboration with young adults, and even teenagers, is vital to put them on the right path and empower them to make smart financial decisions,” Brandt added. “If they have the appropriate toolbox, they can face difficult financial decisions and come out relatively unscathed.”

Kristin McKenna, CFP®, managing director of Darrow Wealth Management in Boston, said financial literacy is important because all adults make decisions about money – often on a daily basis. People may pay taxes, decide how to spend money, or take on new debt.  “There aren’t too many subjects in school that have the same universal relevance,” McKenna noted. “Unfortunately, only a small number of schools incorporate personal finance lessons into the curriculum.”

“There aren’t too many subjects in school that have the same universal relevance,” McKenna noted. “Unfortunately, only a small number of schools incorporate personal finance lessons into the curriculum.”

While U.S. high school personal finance training has expanded in recent years, more work is needed. The Council for Economic Education’s 2020 “Survey of the States” found 21 states now require high school students to take a course in personal finance before graduating, versus 17 in 2018. However, five states plus the District of Columbia have no personal finance training standards. While almost 70 percent of high school students have the option to take at least a one-semester personal finance elective, the CEE noted, less that 17 percent are required to do so.

“Today, financial literacy is not taught consistently at any schooling level, yet is one of the most critically important learning topics among young teenagers and adults,” agreed Indya Yuill, managing director of Beacon Pointe Advisors in Newport Beach, California. “Saving and the power of compounding – when started at an early age – can make life-changing differences in one’s long-term financial health. Even the simple concepts of budgeting and being ‘money smart’ at a young age create habits for long-term success.”

Yuill said Beacon Pointe leaders consider personal finance topics and financial literacy so important for individuals and families that they wrote a book, “Your Dollars, Our Sense: A Fun & Simple Guide to Money Matters.” The book features easy, quick-to-digest concepts to help people know what to do on their own personal finance journey.

McKenna added that, without formal real-world financial literacy education, children and teens mostly learn about money by watching their parents. Financial conversations are taboo in many homes and take place behind closed doors, she continued. Plus, many adults are simply not good financial role models.  “If financial literacy were expanded to adequately prepare tomorrow’s leaders to manage their financial future,” McKenna said, “I think the benefits to society would be pronounced. ‘You don’t know what you don’t know’ is one of my favorite sayings. If someone doesn’t have the toolkit to evaluate a financial decision or consider alternatives, how are they supposed to make the ‘right’ decision?”

“If financial literacy were expanded to adequately prepare tomorrow’s leaders to manage their financial future,” McKenna said, “I think the benefits to society would be pronounced. ‘You don’t know what you don’t know’ is one of my favorite sayings. If someone doesn’t have the toolkit to evaluate a financial decision or consider alternatives, how are they supposed to make the ‘right’ decision?”

Jake Jansen, financial advisor/managing partner at Shillin Wealth Management in Altoona, Wisconsin, noted that most young teenagers are still financially dependent on their parents. Coupling that with a lack of required financial learning in the education system, he said, creates “a recipe for indifference.”

Money mismanagement or lack of attention usually stems from naivety, Jansen continued. Most people do not encounter a finance course until they enter college, and often that class is an elective.

“A fundamental understanding of basic financial concepts can lead to a much more stable financial lifestyle and promote a better pattern of consumer spending,” Jansen added. “In our industry, clients are unable to ask questions (or know what questions to ask) if they do not have a baseline knowledge of what we are discussing.”

Jeff Bush, president of Informed Family Financial Services in Norristown, Pennsylvania, also said the financial services industry had fallen short in meeting the educational needs of its customers. He said consumers need more instruction to enhance their decision-making process.

Independent advisors are in a unique position to boost financial literary, Bush added. He said his firm channels its professional efforts towards keeping clients educationally engaged. That process takes on many forms, including one-on-meetings, distributing a monthly newsletter, posting educational content on the firm’s website, and hosting live events.

Chet Schwartz, RICP®, financial representative at Strategies for Wealth in New York City, said he has been taught that money can be a wonderful servant or a terrible master. The difference between those two alternatives comes down to how people value money and what they understand about it, he said. “The challenge is that money matters are so infrequently taught to us growing up that it creates a ‘financial literacy gap’ between where people are and where they want to be or should be,” Schwartz continued. “This is true for teenagers but, unfortunately, it is often no different for an adult.”

“The challenge is that money matters are so infrequently taught to us growing up that it creates a ‘financial literacy gap’ between where people are and where they want to be or should be,” Schwartz continued. “This is true for teenagers but, unfortunately, it is often no different for an adult.”

Schwartz said he asks new clients, “How many classes did you have in K-12 that taught you about money?" The answers range from zero to two – usually on the low end of the scale. Personal finance is also rarely addressed in college or in advanced degree curriculums, he added.

“Without financial literacy, how can someone possibly know how much to save every year; whether they can afford that vacation or new toy (no matter how much they think they deserve it); what size home they can afford; how to interpret their company benefits; or how to know what prudent investing entails?” Schwarz asked. “It's a taboo topic in this culture. That has to change if people stand any chance of reaching a satisfactory financial destiny.”