Strategic planning pays off

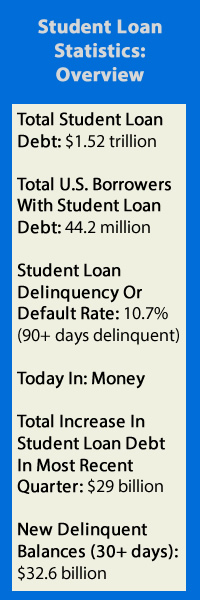

Americans owe $1.5 trillion in student loans, a slow-moving crisis that has left many unable to buy homes, start families, or pursue the careers they want. And the problem continues to grow, 69 percent of students took out loans in 2018 and graduates that year averaged $29,800 in debt. Students’ parents often take a hit as well, with 14 percent holding an average of $35,600 in federal Parent PLUS loans.  Student loans dwarf credit card and auto loan debt. Americans owed $840 billion on their credit cards and $1.21 trillion in auto loans in 2018. Add in the fact that student loans, generally, cannot be discharged in bankruptcy and that tuition costs continue to rise, and the need to effectively approach college planning becomes apparent. College planning needs to start early, however, to avoid the missteps so many student loan borrowers make.

Student loans dwarf credit card and auto loan debt. Americans owed $840 billion on their credit cards and $1.21 trillion in auto loans in 2018. Add in the fact that student loans, generally, cannot be discharged in bankruptcy and that tuition costs continue to rise, and the need to effectively approach college planning becomes apparent. College planning needs to start early, however, to avoid the missteps so many student loan borrowers make.

“Some parents put if off until ninth, tenth, or eleventh grade. Now they’re staring at a $60,000 per year expense coming in and they’re stuck between a rock and a hard place,” said Brian Safdari, president and founder of College Planning Experts, Inc. “We work with parents in high school. It’s a game – it’s a strategy. Just like there’s tax planning, there’s higher education planning on knowing how to position your income and your assets around the financial aid forms to determine how much money you’re going to get from the college.”

College Planning Experts works with families preparing to send their children to college. The firm guides parents through college selection, financial aid preparation, and helps clients develop a strategy to pay tuition without taking on excessive debt or lifestyle restrictions. The firm works with tools and approaches that go beyond the 529 savings plan or other generic strategies that a traditional financial advisor might use.

“We can’t be thinking about ‘Well can we reduce lifestyle expenses and use all of your savings and take that and just pay full price for college.’ Instead we can take that and go to private schools that are cheaper than going to a state school,” Safdair told Advisors Magazine in a recent interview. “We show parents how you can go to a private university that costs $60,000 or $70,000 per year and still get 40, 50, or 70 percent off the college expense so that it’s more manageable.”

Even middle- and high-income families need effective college planning strategies so that their children can avoid high debt loads, Safdari added. Financial aid, often thought of as exclusively for low-income students or those with academic or sports merit scholarships, can actually be taken advantage of by families across the wealth spectrum depending on which college or university they choose.

“Most middle- and high-income families don’t understand that because they hear the term financial aid and assume it’s for low-income families,” Safdari said. “The people that are giving them information they’re not doing anything malicious, they’re just sharing their experience. Well, it’s not a one-size fits all and every school is different.”

Parents need to take an active role in the college planning process as well, but they need to be careful with who they trust.

“There’s a lot of information and Google is very powerful. I tell parents that being reactive around this process, generally when you’re reactive versus proactive, that’s when you get yourself in a lot of mess because you’re asking so many questions, you’re talking to so many people—and parents typically like to talk to other parents—and one of the biggest mistakes that parents make is talking to another parent,” Safdari said. “That’s because they’re asking another parents that probably made a mistake and doesn’t understand the process or how the higher education system works.”

Parents who lack an understanding of the system should find a trusted advisor who can guide them through their options. Safdari said that many parents still burdened by their own student loans often walk through his door looking for help planning their children’s education.

“They probably did it themselves, they got into that mess because they didn’t plan ahead,” Safdari said. “When they come to me, if they had debt or still have debt on their own, one of the reasons they hire me is because they don’t want their kids to go through having that debt or taking out the wrong loans.”

College Planning Experts takes a holistic view of the prospective student, looking at what they want to do with their lives, which institutions they want to attend, and whether those universities can deliver the return on investment needed to make up for the cost of attendance. And while many families hope that financial aid officers and the institutions themselves can offer advice on how the system works, Safdari said those options often fall short.

“Unfortunately, the financial aid office at most universities doesn’t do a good job. They’re not there to sit down with a parent and look at all of their options,” he said. “Specifically, what we do is sit down with a parent and we work out their college costs.”

Without that tailored, professional advice, parents could find it difficult to play the college game.

“Education is so expensive,” Safdair said. “And because it’s so expensive you can literally be broke and be bankrupt before even coming into the workforce if you don’t understand how to handle the higher education system.”

If you are a parent of a high school student and would like a complimentary 30 minute phone consultation to quickly and easily show you how to avoid any pitfalls, or learn the strategies that apply to your family, email Brian at This email address is being protected from spambots. You need JavaScript enabled to view it. or call his office at (818) 201-4847.For more information on College Planning Experts, Inc., visit: collegeplanningexperts.com