Squished between meeting the needs of aging parents and coping with the demands of boomerang children, the current members of the “sandwich generation” – folks who are in their mid-40s to mid-60s – have become a challenging demographic for today’s financial advisor to effectively serve.

Details of the situations that many people in this life-stage find themselves in are the stuff economic nightmares are made of. Their parents are living longer thanks to medical advances but aren’t necessarily prepared financially for the draining cost of in-home or long-term residential care. Simultaneously, the children of the sandwich generation are landing back in the family nest.

Yes, some are victims of an unstable economy and unable to make ends meet on their own, but some are also casualties of their “instant gratification” generation trademarked by impatience with the traditional concept that years of consistent hard work lead to the rewards of a nice home and the latest model car.

![]() “Flat out, the issues faced by our clients in the ‘sandwich generation’ are some of the toughest,” said Larry Welder, owner of Granite Financial Solutions, LLC, with offices located in Georgia, Iowa and Texas. He notes that as “sandwichers” watch their parents enter the geriatric years, their awareness of their own pending aging become impossible to ignore. Yet, “no one wants to believe they are going to get old. Right now, they feel invincible, but when you start to talk about retirement and aging and the problems with our Medicare system, people get frightened and overwhelmed.”

“Flat out, the issues faced by our clients in the ‘sandwich generation’ are some of the toughest,” said Larry Welder, owner of Granite Financial Solutions, LLC, with offices located in Georgia, Iowa and Texas. He notes that as “sandwichers” watch their parents enter the geriatric years, their awareness of their own pending aging become impossible to ignore. Yet, “no one wants to believe they are going to get old. Right now, they feel invincible, but when you start to talk about retirement and aging and the problems with our Medicare system, people get frightened and overwhelmed.”

The struggle is real. Or to put it in more sandwich-friendly terms – this is no baloney.

The issues on the full plates of the sandwich generation are more like one of those monstrously-long party subs stuffed with so many different types of deli meat and cheese that it is nearly impossible to enjoy.

Issues such as:

- Cracking down on Mom and Pop’s poor driving skills – even having to be the one to take away their driver’s license or worse yet, sell their vehicle.

- The endless phone calls from parents with dementia or Alzheimer’s Disease not yet in full-time care who become increasingly confused and need verbal direction and reassurance numerous times each day.

- Johnny or Susie move back in to the basement due to a job loss or a divorce – sometimes with their significant other or their children.

- Disagreement with adult children as to how they should spend their paychecks now that they are back under their parent’s roof.

- Worries that elderly parents will lock themselves out of the house on a cold winter night or that grown children will bring “undesirables” home after hours.

The list could go on and on and mostly centers on variations of financial worry and health concerns. It leaves members of the sandwich generation feeling more like a thin piece of baloney slapped between two pieces of nutrient-void white bread and jammed into a kid’s lunch box mushed between the thermos full of apple juice and the fruit snacks.

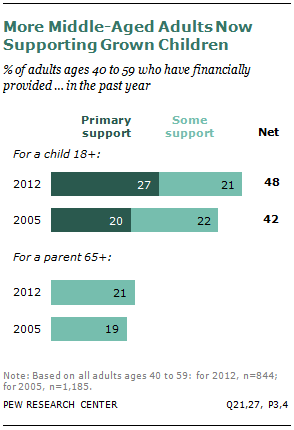

According to the Pew Research Center, one in eight Americans between ages 40 and 60 is raising a child and caring for an elderly parent at the same time.

In reality, the existence of the sandwich generation isn’t a new phenomenon – multi-generational relationships have always been part of the human experience. The difference today – especially in Western societies; particularly in the United States – is that multi-generational living just isn’t something we really do anymore. Mom and Dad live in their home; we live in ours. Our children are supposed to leave the nest and build their own.

Yet, more and more as a sagging economy infringes on that dream, three generations – each with their own life viewpoint – end up together under one roof and often in conflict.

“It is a hindrance to the way we live,” Michael Hall, owner and president of Hall Financial Group, LLC, based in Eau Claire, Wisconsin, said. “In other cultures, the parents are taken in, no questions asked. That is just the way it is. But not in the United States. We do not want to be inconvenienced in this way.”

“It is a hindrance to the way we live,” Michael Hall, owner and president of Hall Financial Group, LLC, based in Eau Claire, Wisconsin, said. “In other cultures, the parents are taken in, no questions asked. That is just the way it is. But not in the United States. We do not want to be inconvenienced in this way.”

He is speaking of trends he sees, not his own personal viewpoint. His father died just 18 months into his retirement leaving his mother penniless because he had not understood the importance of a pension. Hall took care of his mother, but he has seen just the opposite occur far too often.

“Long-term care most certainly is the greatest fright of anyone that is aging,” Hall said. “We work and save and save our entire lives and then only to have it wiped out because of medical care.”

It leaves the question of what steps can a financial advisor encourage clients to take when they find themselves pinched between their parents and their kids?

Create Your Own Safety Net Sooner Than Later

Across the board, financial advisors agree that current long-term care plans are simply far too expensive. Yet, the sooner one buys into a plan – in other words “the younger” one buys into a plan, the better.

Wait until age 60 to buy in to a plan and expect to pay a higher premium.

![]() “So many people that come to me wanting to know about long-term care are usually coming to me too late to buy a long-term care policy at a reasonable rate that is going to be a good value for them,” Ronald Ray, CEO of Turning 65 Solutions Tax and Insurance based in San Antonio, Texas, said.

“So many people that come to me wanting to know about long-term care are usually coming to me too late to buy a long-term care policy at a reasonable rate that is going to be a good value for them,” Ronald Ray, CEO of Turning 65 Solutions Tax and Insurance based in San Antonio, Texas, said.

Noting that government programs offered to pay for long-term care require a significant divesture of personal assets to qualify, Ray recommends the use of life insurance policies or fixed annuities with long-term care riders as a way to leverage personal assets against the astronomical cost that often drains a retiree’s savings.

Set Funds Aside for Health Care Only

![]() This idea comes from Bryan Burkhart, president of Burkhart Investment Group based in Morgan Hill, California.

This idea comes from Bryan Burkhart, president of Burkhart Investment Group based in Morgan Hill, California.

At age 48, his wife had a hemitropic stroke. She was paralyzed on her right side. She needed constant, 24-hour care. She faced a year of recovery that involved eight-hour physical therapy days five days a week.

And Bryan wasn’t ready financially for this.

Now, he encourages his clients to establish a personal health care fund – monies derived from a market portfolio conservatively set up for this purpose only – for when the unthinkable happens.

Engage the Uncomfortable Conversation

It might not be the most fun you’ve ever had with your parents, but an honest talk regarding what financial plans they have made and what expectations they have of you is certainly in order if you are a member of the sandwich generation.

So says Rita Cheng, a certified financial planner and chief executive of Blue Ocean Global Wealth based in based in Gaithersburg, Maryland in an interview with CNBC.

So says Rita Cheng, a certified financial planner and chief executive of Blue Ocean Global Wealth based in based in Gaithersburg, Maryland in an interview with CNBC.

“It's important to talk about financial things, but allow your parents some space," Cheng said. “You don't need to be completely involved in their business, because they still want to be independent and in charge. But ultimately, if they want to be in charge of how they are cared for, they need to be proactive and plan for it.”

Inflation-Proof Your Savings

The power of inflation against your money is the silent killer of many financial plans.

![]() “Far too many people have not taken inflation into consideration when planning,” Alicia Lewis, co-founder Layman Lewis Financial Group based in Loveland, Colorado, said. “Inflation is not going away. It is going to happen to your account whether you prepare for it or not.”

“Far too many people have not taken inflation into consideration when planning,” Alicia Lewis, co-founder Layman Lewis Financial Group based in Loveland, Colorado, said. “Inflation is not going away. It is going to happen to your account whether you prepare for it or not.”

Smith notes recent studies documenting that healthcare costs required by an average geriatric patient doubles every 23 years. That means that a person in their 40’s ought to plan that their healthcare at age 65 will cost them twice what it does today.

Hedging a portion of one’s investment portfolio in acknowledgement of this mathematical fact is something she advises.

Closing Thoughts: Encourage Clients to Take Care of Their Own Health

The National Center on Caregiving based in San Francisco, California, notes that as many as 50 percent of “sandwichers” report experiencing depression and neglecting their own physical health leading to higher rates of cardiovascular conditions, diabetes, high blood pressure and weakened immune systems.

Financial advisors seeking a holistic approach to client care can easily incorporate health-related questions and updates in regular client meetings. Simply asking, “how is your health?” may not suffice.

![]() Carolyn McClanahan of Life Planning Partners, Inc. based in Jacksonville, Florida, suggests starting with this: “Tell me what you do to take care of your health.”

Carolyn McClanahan of Life Planning Partners, Inc. based in Jacksonville, Florida, suggests starting with this: “Tell me what you do to take care of your health.”

It is a loaded question, but it may spur on a lengthy discussion a “sandwicher” client ought to have with a professional who can help him or her set boundaries and prioritize.