Sound habits help future payoff.

Chaotic financial markets offer nearly endless opportunities for investors to snap up distressed properties, lower-cost stocks and bonds, and other investments. Opportunities only come to investors who kept enough assets liquid to actually take advantage, however.

“Ready money is Aladdin’s lamp,” said John Smallwood, CFP®, senior wealth advisor at Smallwood Wealth Management, quoting his grandfather. “Liquid money can help you take advantage of opportunities, if you don’t then you’re stuck like everyone else.”

“Ready money is Aladdin’s lamp,” said John Smallwood, CFP®, senior wealth advisor at Smallwood Wealth Management, quoting his grandfather. “Liquid money can help you take advantage of opportunities, if you don’t then you’re stuck like everyone else.”

Smallwood Wealth Management, based in Red Bank, New Jersey offers comprehensive wealth management services to clients large and small so that they can be ready to take charge when opportunity knocks. The firm does not maintain a minimum asset level or investment to sign on as a client, and instead looks at each prospective investor’s future potential to be a long-term partner. Smallwood Wealth Management acts as a fiduciary, meaning that clients’ best interests come before the bottom line.

“I want somebody that has a future and they’re willing to grow, and they’re willing to invest in themselves,” Smallwood told Advisors Magazine during a recent interview. “I have one client who, when he came to us, had started his own company and it was rocky and there was credit card debt and he really didn’t have much. We built this whole protection area up, made sure that his plan was perfect. Then his business became successful and he accumulated millions of dollars, if I had said no to him when he didn’t meet my minimum then he’d be somewhere else right now.”

Working with investors to develop good habits allows them to unlock the “magic lamp” later. Smallwood works with clients to develop the right attitude toward savings, asking them to set aside 15 or 20 percent of their income each month.

“If you have that habit from day one then you’re fine. The rest of your spending doesn’t matter,” he said. “That habit is going to solve the majority of your future problems.”  Investors often hesitate to take charge of their financial futures and need a trustworthy advisor to explain how their money works for them. Financial literacy is key, Smallwood said, but added that applying that knowledge is even more important. Investors who understand their goals and how to make the right decisions to achieve those goals come out on top.

Investors often hesitate to take charge of their financial futures and need a trustworthy advisor to explain how their money works for them. Financial literacy is key, Smallwood said, but added that applying that knowledge is even more important. Investors who understand their goals and how to make the right decisions to achieve those goals come out on top.

“At five years out you can help yourself, at 10 years out you can really make plans, and at 20 years out there’s a lot you can do,” Smallwood said.

“The problem in the industry is that there’s so much misinformation, there’s so much teaching that’s half the story,” he added, also noting that study after study shows retirement preparation remains weak from generation to generation. “Despite all the information, despite all the technology, despite everything, financial success is still harder. Fundamentally, we all know we should save money but it’s shiny objects – all of those things weren’t in people’s financial plans 30 years ago.”

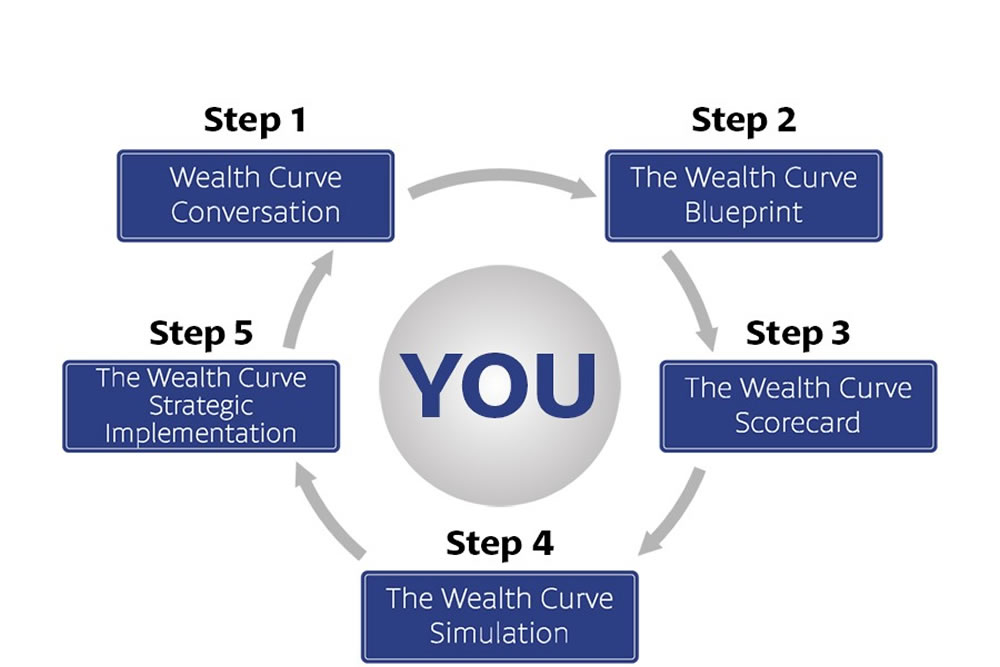

Smallwood takes investor education seriously and his new wealth management book, It’s Your Wealth, Keep It, is slated for publication early next year. Smallwood said the book targets investors who need a clear picture of what, and who, is putting pressure on their wallets and how they can protect their money.

Investor education recently became a hot topic in the financial services industry as retirements get longer and literacy continues to lag. A 2017 study from The American College of Financial Services found that 87 percent of baby boomers scored “D” on a set of questions designed to test basic financial reasoning. Smallwood Wealth Management works with clients to ensure they can make the best financial decisions possible.

Disclosure is one area where investor education proves critical. Investors often find it difficult to sort through the abundance of disclosures and overlong, legalese prospectuses that come with financial products such as 401(k) plans. The 401(k) catches the most flak, but other products present unique issues as well, Smallwood said.

“The 401(k) disclosure needs to be more robust like other financial services are,” he said. “But the mutual fund industry and the ETF industry have basically hidden trading costs which come on top of the expense ratio. There’s a lot of non-disclosure that’s actually going on.”

Smallwood learned the financial industry’s ropes at his father’s firm – but no special privileges came from working with family.

“He was a firm believer in failure and learning from failure,” Smallwood said. “He had seen so many people bring their children into the business and put their children behind a computer screen and never let them talk to the clients. They never really understood how to do financial planning.”

Smallwood’s father created a set of “rules” for the junior Smallwood to follow such as acquiring a Certified Financial Planner (CFP) credential. The chief rule, however, was that his son had to learn effective client communication.

“My father never wanted to give me a client – he wanted me to find my own clients and that would teach me, in turn, to be a more resilient person,” Smallwood said. “The goal was to be self-sufficient in the industry.”

The Smallwood’s broke away from a major financial services firm and went independent more than 25 years ago. They ran their firm as partners until Smallwood’s father retired last year. The father and son team make up a minority of advisories that make it through the first few years of operation.

“Not a lot of people make it and survive, the numbers are stacked against us for it,” Smallwood said.

With several generations of financially savvy relatives, however, it might not come as a surprise the Smallwood’s made it since they lived and breathed the industry and, in turn, passed along that dedication to their clients.

“I want as many sources of income as possible when I hit retirement. If one dries up, I can step in,” Smallwood said. “That was our dinner table conversation, it was in my blood.”

For more information on Smallwood, visit: smallwoodwealth.com

Securities offered through Purshe Kaplan Sterling Investments, Member FINRA/SIPC. Headquartered at 18 Corporate Woods Blvd., Albany, NY, 12211.

Purshe Kaplan Sterling Investments and Smallwood Wealth Management are not affiliated companies.

Investment Advisory Services provided by Smallwood Wealth Investment Management, LLC an SEC registered investment advisor.