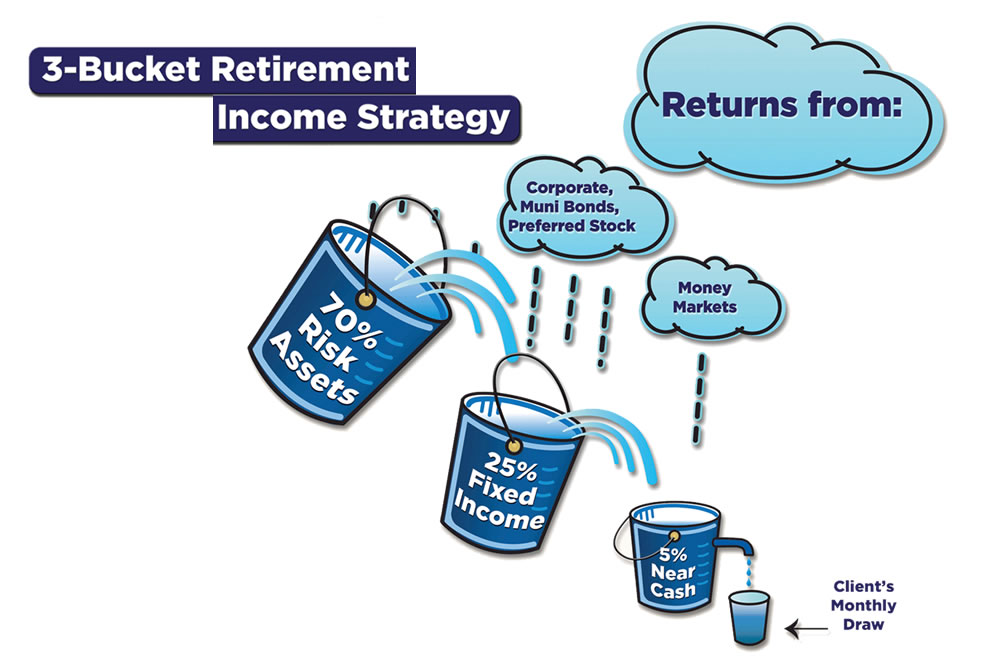

Damian Rothermel CFP®, founder and financial planner of Rothermel Financial Services, LLC, believes in the bucket approach to retirement portfolio planning – the notion that a client’s total assets are divided into a series of four to five buckets.

This approach allows funds allocated for immediate use such as living expenses within the next three to five years to be invested with less risk so as not to jeopardize cash flow.

Buckets identified for one, two or three decades in the future contain monetary assets for which greater risk in an effort to keep ahead of cost-of-living increases and inflation is acceptable. That’s the bottom line of how Damian Rothermel approaches his current and potential clients.

His 18-years in the financial services business prove his belief that being an investor’s advisor requires much more than just product selection.

“It is the mantra that I preach to my people,” Rothermel said from his Portland, Oregon office. “Even before we start working together, I tell them, we plan first and we invest second. There are plenty of good products out there. But there are not perfect products. That is why we need to know what the heck we are trying to accomplish before we go out to buy something so we can select the absolute best product to fit the client needs.”

Rothermel said he takes more than just one or two meetings to get to know a client and his or her specific needs. Developing that authentic advisor-client relationship characterized by an advisor owning a deep and thorough understanding of what the client’s true needs are takes more time than just a couple of office visits, he said.

He’s heard the horror stories from potential clients who felt rushed into investment decisions by other financial advisors. He doesn’t want anyone to be able to tell that sort of story about his work.

“I find for myself as a professional, that taking it slow and getting the diagnosis right for each client is the way to go,” Rothermel said. “The biggest thing that I provide for my clients is trust by going through that financial planning process first and coming up with a plan that suits their needs that they support and agree on. Then we look at investing to make that plan reality.”

He understands and uses the philosophy of asset allocation, but for Rothermel, the more accurate way to describe his investment method is perhaps one of account identification.

“We identify each account based on what its purpose is,” Rothermel said. “My clients know that the funds they are going to live off for the next five years are safe from market risk. They also know what the purpose is for other accounts and what triggers or events in the future could prompt us to change investment strategy with those funds.”

Properly applied knowledge is indeed power.

It’s why his thoughts on the explosion of online financial planning tools is somewhat mixed.

“I worry about the information overload that so many people experience today,” Rothermel said.

“There are so many voices out there saying, ‘this is the best product or account,’ or ‘buy this, don’t buy that.’”

He’s not sure what available online is at the level where most consumers can gain the best knowledge or increase their financial literacy from using the plethora of online tools. He thinks those currently using online tools in a successful manner are folks who were already financially educated and are simply capitalizing on the value proposition that some online platforms offer.

“To some extent, it is just a new tool to do what people have already been doing, he said. “You can have all the online tools you want, but there is still a huge value in having someone you can sit down with and talk to.”

That doesn’t mean he’s against technology.

His take on the use of tech in his industry is an arms-wide open approach.

His firm stays abreast of the industry’s latest and greatest software programs that nearly instantly provide the calculations he shows clients to give them progress reports, forecasts and an ability to better grasp the “what ifs” of the investment world.

“Having the software to do those calculations is wonderful,” he said. “Five to ten years ago, those calculations took up so much of my time. Now, I lean heavily on my technology staff to provide those performance numbers for client reports, but it saves me a tremendous amount of time that is now free to focus on meeting with clients.”

He acknowledges the pending regulatory changes by government agencies in an attempt to herd his industry toward operation under a full fiduciary method.

For Rothermel, the changes won’t alter his current course. As a certified financial planner®, he already operates under the fiduciary standard of putting client interests and needs ahead of his own.

But he does worry about his industry as whole.

“It concerns me that so much of our industry is a buyer beware type of situation rather than advisors automatically doing the right thing,” Rothermel said.

For his practice, his plan is to continue getting to know his clients – their beliefs, dreams, fears, goals and risk tolerance – before selecting their investments.

“I am going to be there to help them,” he said.

For more information visit: www.rothermelfinancial.com

Damian Rothermel is an investment adviser representative of, and securities and advisory services are offered through, USA Financial Securities Corp. (Member FINRA/SIPC). USA Financial Securities is a registered investment adviser located at 6020 E Fulton St., Ada, MI 49301. Rothermel Financial Services is not affiliated with USA Financial Securities.

Bucket System Approach to Retirement