Distressed investing is often characterized as a cyclical strategy dependent on macroeconomic factors that focuses primarily on the undervalued distressed debt of struggling companies that may require a restructuring through bankruptcy or another form of reorganization. Benefits presented by investing in this asset class can include equity-like returns with lower volatility and risk, illiquidity premiums, differentiated return drivers and portfolio diversification opportunities. Since its inception in 1990, the HFRI ED Distressed/Restructuring Index returned 9.7% annualized with a standard deviation of 12.7%. This compares favorably to the Russell 2000 which, over the same time period, returned 8.7% annualized with a standard deviation of 18.7%, and to the Credit Suisse High Yield Index which returned 7.84% annualized with a standard deviation of 17.9%.

Current environment for distressed investing

Investor interest in distressed investing is growing rapidly and rightfully so. Nearly two-thirds of investors surveyed by Preqin in the first half of 2023 intend to increase their allocation to the asset class. While the current economic cycle has been prolonged due to high levels of liquidity, fiscal stimulus and suppressed default rates, the tides have begun to shift. Sectors including commercial real estate, hospitality and retail face higher levels of leverage and lower revenue. Higher interest rates, a weakening macro environment and a reduction of regional bank lending are putting pressure on many businesses and cracks are beginning to surface.

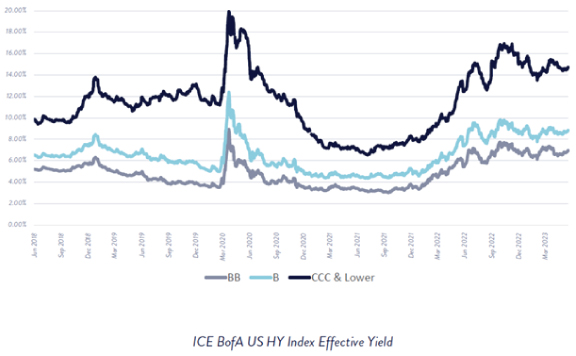

As we enter the third quarter of 2023, bankruptcies are set to accelerate and the pipeline of distressed debt is growing rapidly. US corporate debt yields are nearing COVID-19 panic highs and loan market yields are at multi-year highs with significant and excess spread between distressed and non-distressed debt.

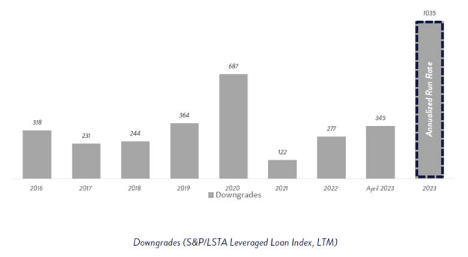

Credit downgrades are also increasing rapidly and are on track to exceed COVID-19 highs while monthly US bankruptcy filings are at a multi-year high (year-to-date through June 30th US bankruptcy filings are at a 12-year high).

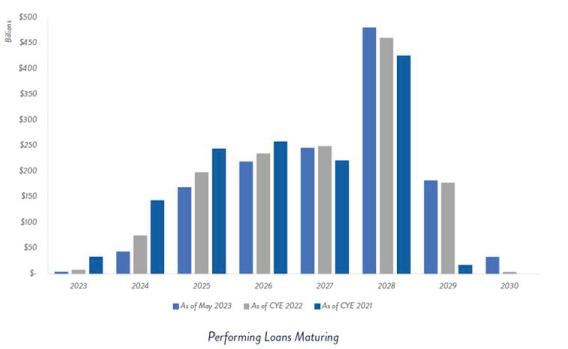

The upcoming loan maturity wall will require refinancing at much higher rates, assuming it is possible to refinance based on the increase in interest rates and substantially higher lending standards by banks. This should create a significant opportunity for distressed investors for years to come.

Globally, the total amount of high-yield bonds, BB-rated bonds, leveraged loans and middle market loans outstanding is now over $12 trillion, more than four times what it was in December 2007 amid the early stages of the global financial crisis.

Should distressed be a core long-term allocation?

Many investors believe that this segment of the capital markets can be timed and should be scaled into and out of at different stages of the economic cycle. Some large distressed funds confirm this strategy by including triggers in their operating documents that limit what percent of committed capital can be called based on default rates or credit spreads.

While it is true that the size of the distressed universe generally has an inverse relationship to the business cycle (peaking when the economy is at its worst), investors can miss out on significant opportunities by staying on the sidelines.

The reality is there are always pockets of opportunity, and individual and broad distressed situations can emerge in any market environment whether during an economic expansion or a contraction. Instead of attempting to market-time, investors should consider a broader mandate that allows for investing across the capital structure and across the distressed and economic continuum that can be increased or decreased based on market conditions. Additionally, as we will explore below, the middle market offers a highly compelling opportunity set for investors to achieve their goals.

Benefits of a flexible distressed mandate

Successful distressed investing requires a high level of proficiency navigating the reorganization process (whether out of court or a formal Chapter 11), modeling various possible outcomes and quantifying risk. It also requires experience across market cycles and strong relationships with bankruptcy attorneys, restructuring advisors, lenders, distressed trading desks and industry experts to help source opportunities, understand shifting industry dynamics and navigate complex legal situations. Another key to successfully investing in distressed situations is the ability to look at the entire capital structure for opportunity.

Investing across the risk spectrum, including debt and equity-oriented securities of a business’s capital structure during distress, restructuring, emergence and turnaround, can unlock significantly more value versus investing in credit-oriented securities alone. Relative valuations across the capital structure change over time and a broader mandate allows managers to focus on the most attractive parts of a company’s capital structure, from secured debt, unsecured debt, hybrid debt, preferred equity, equity, warrants and contingent value rights. This flexible approach across the balance sheet helps maximize risk/reward as relative value changes.

The ability to invest upon emergence from bankruptcy often offers the best risk adjusted return due to the taint of bankruptcy and the liquidating of the post-reorganization securities by creditors, which can cause these securities to trade well below intrinsic value.

As an example, once a company has restructured with an improved balance sheet and a turnaround is underway, the healthier performing company’s senior debt may be refinanced or appreciate in price closer to par. In addition, post-reorganization equity tends to be liquidated by creditors in thinly traded markets, either because of bankruptcy fatigue or the securities no longer meet their investment guidelines making them forced sellers. This can create significant upside potential.

During the last full credit cycle (Great Financial Crisis to COVID-19 pandemic), companies that emerged from bankruptcy with >$100mm market cap averaged +860bps outperformance versus the Russell 2000 in the first year following emergence. Importantly, there tends to be a wide dispersion between winners and losers.

Benefits of focusing on the middle market

The bulk of stressed and distressed opportunities historically reside within middle market companies. Over the past 20 years, of the 2,379 US bankruptcies tracked by Bloomberg, approximately 90% (2,161 companies) had liabilities below $2bn and only 10% (218 companies) had liabilities over $2bn.

The smaller distressed middle market companies tend to have greater pricing inefficiencies and larger potential returns due to lack of Wall Street coverage, elimination of bank proprietary trading departments and larger distressed funds often avoiding them due to sizing constraints.

Middle market and smaller cap distressed opportunities also tend to be diversified across sectors where larger capitalization distressed opportunities tend to be concentrated in a specific, troubled sector or cyclically driven. In addition, middle market companies tend to hit bumps in the road more frequently versus their larger cap peers, creating more opportunities to generate strong returns throughout the business cycle. They are more prone to labor shortages, supply chain issues, have less access to public markets and tend to pay higher interest rates regardless of the fundamental soundness of their business.

Conclusion

The current environment for distressed investing is highly compelling and the opportunity set that is expected to continue to grow in the coming years is creating significant investor interest.

Distressed should be viewed throughout market cycles as a core allocation with a broad mandate across the capital structure and a focus on middle market opportunities.