While already underway prior to the COVID-19 pandemic, many life insurance policies are now underwritten through “simplified” or “streamlined” processes, which are less reliant on physical data (e.g., blood, urine, examination) and more reliant on readily available datasets (e.g., medical, financial, personal).

According to LIMRA’s Consumers & Underwriting study, conducted in October and November of 2020, most consumers are aware of this type of underwriting and it has a positive influence on their likelihood to buy life insurance.

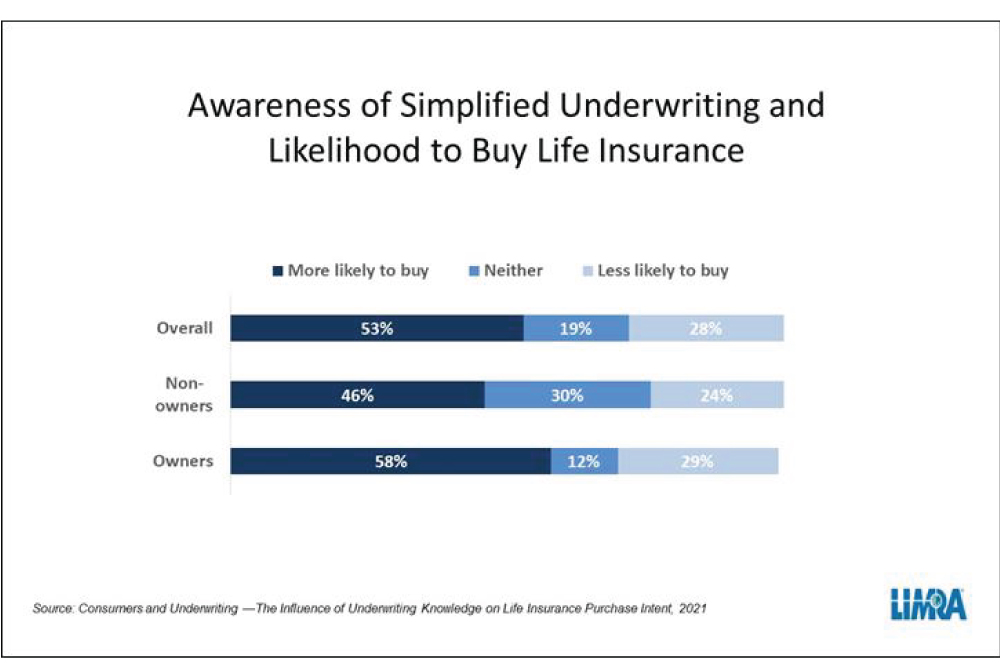

Awareness of simplified-issue has a positive influence on the likelihood to buy coverage for over half (53%) of all respondents. Of those who already own life insurance, almost 6 in 10 (58%) indicate they are more likely to buy via simplified-issue, compared with 46% of non-owners.

“This is especially important since our research shows that about 60 million Americans are either uninsured or underinsured,” says Jim Scanlon, assistant vice president, LIMRA Insurance Research. “The easier life insurance companies can make it for consumers to get coverage, the more likely they will be to purchase life insurance to protect their loved ones should the unexpected happen.”

The study also revealed the appeal of simplified underwriting. Top reasons consumers gave include:

- It is fast and easy (74%)

- It provides transparent explanations of risks and pricing (69%)

- It is unbiased and objective (69%)

- It avoids the need for a medical exam (68%)

The appeal of simplified underwriting is universal across all generations, although Baby Boomers are more likely to buy via simplified underwriting than Millennials or Generation X. Women are slightly more likely to buy life insurance using simplified underwriting (55% versus 52% for men).

Scanlon notes that emphasizing the availability of simplified-issue systems also gives financial professionals an opportunity to deepen relationships and enhance their clients’ financial security, and to do it a time-efficient manner.

“This was especially important to financial professionals during the pandemic when meeting face-to-face with clients was a challenge,” Scanlon says.

Although consumers expressed more of a likelihood to buy when simplified underwriting was used, some are unsure about what it actually involved. On a 16-question assessment of underwriting knowledge, consumers were given options of true, false or don’t know. Consumers correctly answered only 41% of the questions; were incorrect on 42% of their responses; and used the “don’t know” option for 17% of the questions.

“This indicates consumers are sometimes aware of their lack of underwriting knowledge, but, in general, they believe they know more than they actually do,” Scanlon says. “This is a problem because our research finds people who lack knowledge of the basics about life insurance are less likely to purchase the life insurance they need.”

LIMRA, along with seven other trade associations, launched the Help Protect Our Families campaign in February to help the industry — carriers and distribution — engage consumers, help them understand the importance of having life insurance coverage and ultimately, get more families adequately protected.