As life spans increase, retirement planning becomes increasingly complex. Long-term care concerns, saving enough to retire for almost as long as a retiree worked, and optimizing Social Security all pose complications for savers who want their hard-earned money to work for them in retirement. Today’s low interest rate environment further complicates the retirement scene and savers need an advisor able to guide their transition to retirement.

“The key to retirement planning is finding the appropriate intersection of income, growth and guarantees, but the low interest rate environment makes this difficult,” said Jeremy Nelson, a partner in Element Wealth, adding that his firm works to maximize guaranteed income streams for clients, often against the prevailing wisdom. “Social Security optimization, a lot of people make the mistake of drawing early because they fear dying and not getting out, what they put into the system … [But] a loss is a loss whether you lose by one goal or 10. Delaying where possible provides income security and protects us against longevity and gives the plan an inflation hedge.”  Element Wealth, based in Ridgeland, Mississippi, provides financial, retirement income, asset management, and legacy planning to clients ready to take charge of their financial futures. The firm does not require a minimum asset level to sign on, instead Nelson looks for clients who agree with his holistic view of financial planning and who are ready to make difficult decisions about their retirement.

Element Wealth, based in Ridgeland, Mississippi, provides financial, retirement income, asset management, and legacy planning to clients ready to take charge of their financial futures. The firm does not require a minimum asset level to sign on, instead Nelson looks for clients who agree with his holistic view of financial planning and who are ready to make difficult decisions about their retirement.

“Ultimately people have limited resources, they have differing views on investing and risk, and they all have differing goals for themselves and their families. Our service model is built around pulling all of those things together so that clients can feel comfortable about their financial future,” Nelson told “Advisors Magazine” during a recent interview.

Life expectancies – despite modest declines the past two years due to a rising suicide rate and substance abuse issues among certain population segments – continue to rise overall and current savers can expect to live into their 80s or 90s. The traditional worker who wants to retire at 65 needs to grapple with the fact that he or she probably will be retired for almost as long as he or she worked. A good advisor who can ground investors in financial literacy, and prepare them for considering the wide variety of products and services available to ensure their golden years go as planned, is a must.

The Key Elements of Successful Wealth Planning

Building a successful retirement plan and resisting the urge to make hasty decisions when the market turns can make or break a saver's financial situation. Element Wealth works to educate clients on the options available for their portfolios and the risks involved with different types of investments. The firm also communicates frequently with clients to ensure their financial plan remains on track, and to make adjustments if needed.

“Education is everything. We’re not in a business where we’re able to make a lot of guarantees,” Nelson said. “The future is unknown. Markets are going to go through periods in which they test our plans. Clients must have a long-term focus. The key to a successful retirement plan is to stick to the plan. We have to monitor and adjust over time, but if we freak out and flip every time that markets turn then ultimately we’re setting up clients to fail.”

Nelson walks his clients through their finances step-by-step, making time for questions and ensuring that investors “get it” before moving on. Financial literacy, even among educated clients, tends to lag due to the industry’s tendency to rely on jargon, over-written prospectuses aimed at attorneys, and advisors who fail to realize that while money is second-nature to them, it can be foreign to new investors. Getting clients up to speed requires an environment in which advisors listen, questions are given the time and attention they deserve, and no topic is off-limits.

“If you come into our office, we have whiteboards in our meeting rooms, and my favorite thing to do is just get up on the whiteboard and draw these things out because I think that simple visuals help clients understand these concepts,” Nelson said.

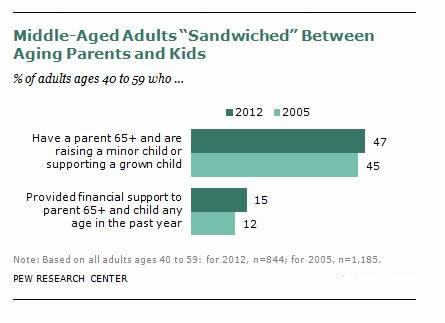

Each client’s unique situation also makes investor education tricky. Nelson has to carefully plan for each client, explaining to them what they need to know to tackle their individual financial challenges. A number of investors today, for example, find themselves locked into the “sandwich generation,” meaning they care for both an elderly relative and teenage or adult children. Assisting sandwich generation investors requires a different approach from traditional retirement planning.  A 2013 Pew Research Center study found that 47 percent of adults in their 40s and 50s are members of the sandwich generation, defined as taking care of both an adult or minor child and an elderly relative older than 65. Burgeoning health care costs for an elderly parent can maul a retirement plan and advisors also need to consider the emotional toll of being “sandwiched.”

A 2013 Pew Research Center study found that 47 percent of adults in their 40s and 50s are members of the sandwich generation, defined as taking care of both an adult or minor child and an elderly relative older than 65. Burgeoning health care costs for an elderly parent can maul a retirement plan and advisors also need to consider the emotional toll of being “sandwiched.”

Nelson uses a few money management shortcuts to keep these investors on track.

“[We] bucket and designate money for different time periods,” he said, adding that clients who could reasonably become “sandwiched” need to manage their plans very carefully. “There are variables that are going to come up that they weren’t expecting when they sat down and made that plan.”

Elderly investors, or their sandwich generation children, also need to consider the possibility that they will require long-term care for serious ailments such as infirmity in old age or dementia.

The long-term care insurance market, however, is seeing many insurers pull-out as regulations raise the cost of doing business; the insurers left, meanwhile, have jacked up prices while cutting back on benefits. The remaining long-term care plans often leave consumers with little choice and, possibly, no realistic options.

Nelson instead proposes to many clients that they use “asset-based long-term care,” in which investors determine how much they can afford to self-insure. Asset-based long-term care comes with an opportunity cost, but investors will “always get back at least what [they] put in,” Nelson said. He added that the strategy also acts as a hedge against extended care for illnesses such as Alzheimer’s.

No matter the financial situation, knowledge of basic money management is essential for investors. Without a grounded advisor, however, investors can easily be led astray by misinformation or let their emotions influence their financial decision-making, resulting in poor outcomes.

Battling Misinformation

Few retirement savers come to their new financial advisor with a thorough knowledge of the market and how it works.

“The financial planning process, investing, markets, all these things, are very complicated,” Nelson said. “People generally don’t have education on these topics.”

Fragmentation drives financial misinformation with the internet, 24-hour business news, and uninformed laypeople all feeding into market frenzies. It can be difficult, in this chaotic environment, for investors to resist the creeping anxiety that can influence their decisions for the worse. Nelson said that he works with clients not only to educate them about the market, but also on his responsibilities as a professional advisor.

That standard of disclosure is lacking in many corners of the financial services industry, where advisors often neglect to give clients a full picture, he said.

“We need to hold advisors to the same standard of care. This isn’t just about how people are compensated because there are times when a commission-based product is right for a client,” Nelson said. “We should have to demonstrate that we’ve gone through a process to ensure that the recommendations we’re giving to people are the appropriate solution.”

Nelson acts as a fiduciary to his clients, meaning Element Wealth puts investors’ best interests before bottom-line concerns such as commissions. To Nelson, that means presenting clients with options and then educating them to make their own choices; and it also means being upfront with clients about how he is compensated for advising them.

Client education, financial goals, and tolerance for the unknown all come together to create an investor’s plan. Nelson works with investors to find where all of the possibilities inherent to the market could potentially interact, and to then help clients set their own limits, choose their own products, and make their money work for them. As a fiduciary, however, that sometimes requires being firm with clients who might be headed in the wrong direction. Clients who hesitate to pull the trigger on suitable investments, or who are too concerned about losses to take action, need an advisor to encourage them to accept the realities of the market – even if that can be difficult.

“We find the intersection of income, growth, and guarantees for each individual client,” Nelson said. “We help them understand the difference between risk tolerance and the need for risk; some people are very risk-averse but if they have no growth in their plan then they aren’t going to make it.”

For more information, visit: myelementwealth.com