Guiding clients through market cycles

Many young and tech-savvy investors will forego working with financial advisors to handle their own financial planning. The rationale is that they regularly use apps to simplify other aspects of their lives, so robo-advisors and investment technologies can help them to manage their investment portfolios. After all, what can a financial advisor do that technology cannot?

From a pure, practical standpoint, investment apps and technologies can do whatever a financial advisor can do. They can facilitate trades and purchases of stocks. They can notify clients when investments are going up or down, and list options available for achieving different investment goals.

However, robo-advisors have limitations. They cannot provide reassurance when the markets fall or investment returns take a turn for the worse. They cannot calm your fears or respond to worrisome phone calls. They cannot account for your life experiences, provide direction on when to take action, or offer personalized solutions that are geared to helping you achieve specific financial goals. You cannot form an emotional connection with a robo-advisor, nor can it determine what is most important to you, such as meeting philanthropic goals or leaving a legacy for the next generation.  “Advisors Magazine” spoke with Van Mason, CFP®, CLU, MBA, President and LPL Registered Principal of StoneRidge Wealth Management, one of the leading independent wealth management firms in the greater Portland-Vancouver metro area about the importance of the client/advisor relationship.

“Advisors Magazine” spoke with Van Mason, CFP®, CLU, MBA, President and LPL Registered Principal of StoneRidge Wealth Management, one of the leading independent wealth management firms in the greater Portland-Vancouver metro area about the importance of the client/advisor relationship.

“Our clients come to us for our experience, our careful and educated assessment of the economy and the markets, and for our written fiduciary pledge. We’ve guided our clients through the tech crisis, the attacks of Sept. 11, and the agonizing debacle of 2008. We utilize technology to make the investment process more efficient, but nothing can replace the trust and confidence that is earned from sitting down with our clients every single quarter,” said Van. “We review their statements to make sure our clients understand the confusing numbers, but more importantly, we try to listen and understand the issues that keep our clients awake at night.”

StoneRidge Wealth Management has been providing independent retirement and financial planning services for more than 20 years. Van’s comprehensive grasp of financial issues was established while completing his MBA from the University of Oregon, and later honed as partner and president of Mason-Daane-Hucke Inc., a construction products company. Amy Treat is Partner and Chief Operating Officer of StoneRidge Wealth Management, and has been with the firm since 2003. She has developed and managed the administrative, marketing, and technological efficiencies that have helped StoneRidge grow and succeed. Van and Amy internalize the importance of philanthropy and “giving back”. They launched The StoneRidge Foundation in 2008, a registered charity with the State of Oregon, that provides funding for low income children with serious hearing deficiencies. Their motto is “Help us flip the switch and let them hear the music”. Every dollar goes directly to support the kids.

An experienced financial advisor will help the client develop his or her own investment strategy, one that is flexible enough to adapt to the incessant challenges of the market and the economy, but also to the changes in the client’s personal life. The advisor must be an educator, filling in the gaps in the client’s knowledge base, and making sure that the client understands the consequences resulting from uneducated investment decisions.

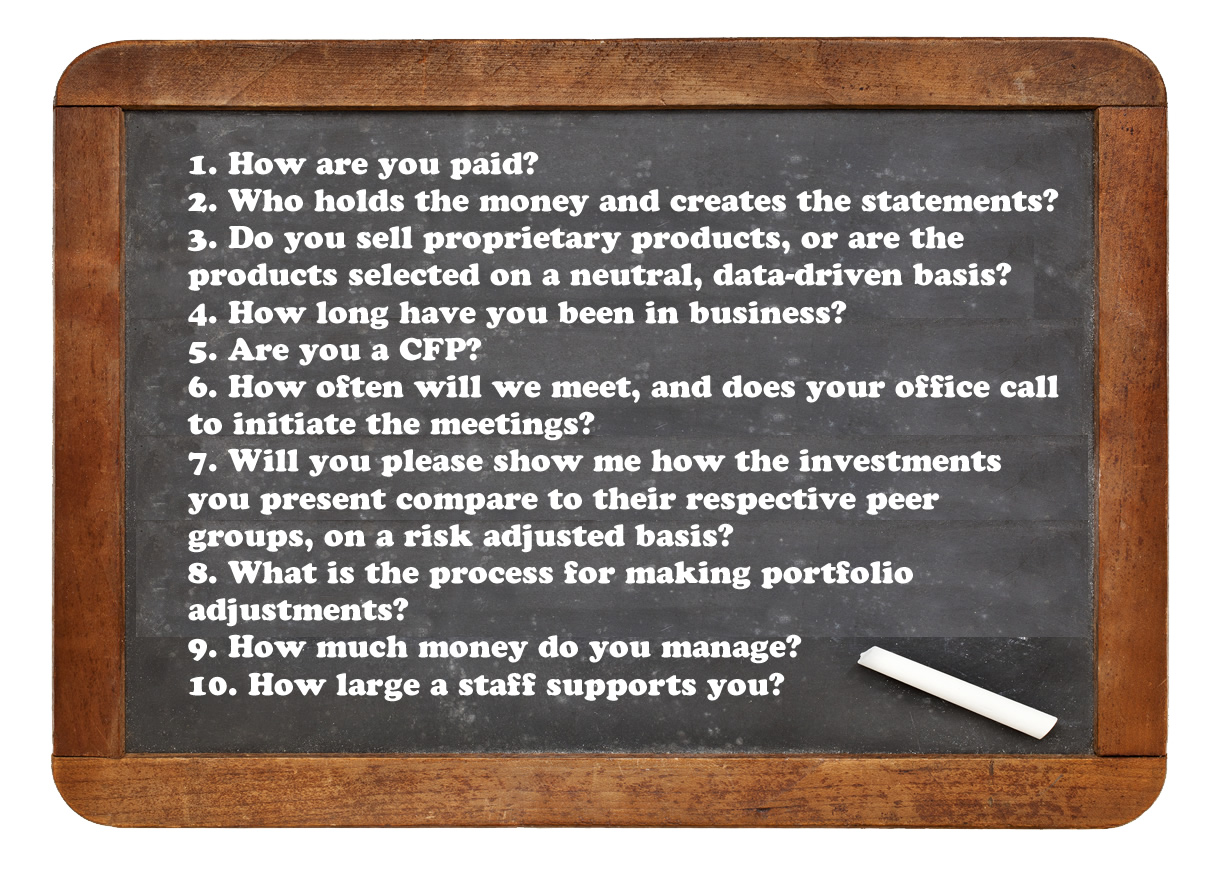

“Many investment savvy clients have come to me because the spouse has never shown much interest in the family investments, and there is an imperative to build a solid advisor-client relationship while both spouses are living,” Van said. “The surviving spouse who has always prepared for the next automobile, computer, or appliance purchase may be completely unprepared to interview a financial advisor, having no idea what questions should be asked. In our first meeting, I always make sure the prospective client asks me these critical questions:

We asked Van about portfolio risk, and how he approaches this frightfully complex subject with his clients.

“The first risk is serious portfolio loss of course, but the second risk is lost opportunity. Balancing these two threats is the million-dollar question, and this is why we meet with our clients every quarter,” he said. “With new clients, I usually begin the discussion with this observation: The market is always going up, except when it’s not. As silly as this sounds at first, it sets the stage for prospective clients to open up and tell me how they’ve felt during periods of significant market volatility.

I explain that there have only been four seriously negative markets since WWII, and that each of these has resulted in a market loss of about 40%. We had the oil embargo of 1973-1974, the tech bubble bursting in 2000 followed by the attacks of September 11, 2001 (the only consecutive three years of market loss since the Great Depression), and the financial crisis of 2008. Given that anything can happen, should we prepare our portfolio for the risk of a 40% or greater loss, or build the portfolio for a reasonable expectation of continued market growth?

Market volatility is uncomfortable for everyone, but routine market sell-offs usually recover within a few months. It’s my responsibility to help the client differentiate between serious market disruptions like the tech bubble and uncomfortable short-term sell-offs, as the fourth quarter of last year.”

“If clients are taking monthly distributions to maintain their retirement lifestyle, we project a conservative portfolio growth rate, and then work to shelter their distributions from serious market loss,” Van continued. “I call this strategy “The Cookie Jar.” As a hypothetical example, the client has $1 million portfolio. The markets have averaged between 9%-10% per year since WWII, so a conservative strategy reduces this market average by about 40%, and we schedule distributions of about 5.5% per year.

These distributions, coupled with the client’s Social Security, pensions, and other income will create their income base. Because the markets historically begin to recover from serious market loss within 18 months, investing 18 months of distributions (about $82,000) very defensively aims to shelter this money from serious and unexpected market loss, and can allow the client to continue their distributions without “selling low” during the negative cycle. Of course, the Cookie Jar’s annual returns will be relatively low during positive growth cycles, but the lost opportunity only applies to about 8% of the portfolio, while the other 92% may be allocated to growth. Then during positive markets, we urge the clients to “pay themselves a bonus” with the returns that have exceeded our projections.

We asked Mr. Mason how he selects the specific investments, relative to the various criteria of risk.

“It’s a good bet that the client’s eyes will glaze over if we start talking in terms of beta, standard deviations, Sharpe, etc. So, unless the client is an engineer who eats this stuff up, I try to avoid the technical terms. And from a practical standpoint, why should we emphasize such terms as beta, when leading health and biotech funds with a beta of approximately 1.3 (1.3 times market gain/loss) only lost 12% in 2008 when the markets lost 35%? Or medical devices with a beta of 1.06 outperforming the Dow 142% to 60% over the last five years? This is what an experienced advisor brings to the table. The robo advisor says “beta 1.06: buy”, while the experienced advisor recommends the purchase based upon the positive global demographics. I have a delightful 84-year-old client who refers to her medical devices ETF as her “global knee thingy” investment.”

For more information on StoneRidge Wealth Management, visit: www.stoneridgewm.com

Securities offered through LPL Financial, Member FINRA/SIPC.