Due diligence and approachability are vital

Much has been written recently about the wealth gap in the United States. The growth in income in recent decades has tilted to upper-income households, according to The Pew Research Center. “At the same time, the U.S. middle class, which once comprised the clear majority of Americans, is shrinking,” the Center noted in a 2020 report. “Thus, a greater share of the nation’s aggregate income is now going to upper-income households and the share going to middle- and lower-income households is falling.”

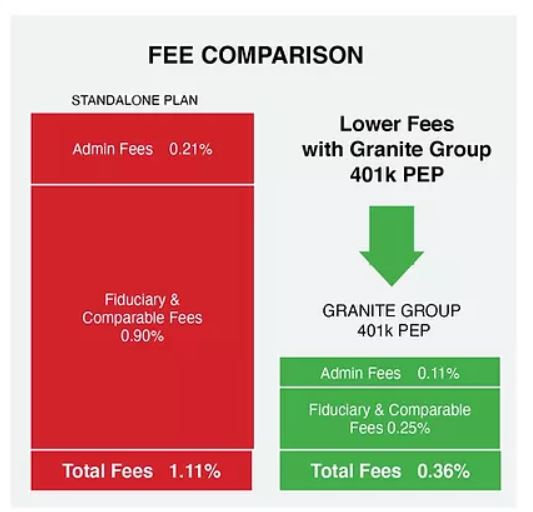

Financial consultants and advisors who understand the full income landscape are well-positioned, according to Stamford, Connecticut-based GGA Retirement. GGA Retirement is an experienced, independent consultant for 401(k) plans, serving as a 3(38)-plan fiduciary. In short, GGA provides wholesale 401(k) management services to other financial advisors, as well as 401(k) retirement plan management for employers. It’s a division of Granite Group Advisors, a wealth management firm established in 2003. “We look at both the normal and the uber-wealthy,” Lyle Himebaugh, co-founder of GGA Retirement, told Advisors Magazine in a recent interview. “This gives us ideas about what we should be doing for our clients. We don’t want to be complacent…if you are complacent, you are dead.”

“We look at both the normal and the uber-wealthy,” Lyle Himebaugh, co-founder of GGA Retirement, told Advisors Magazine in a recent interview. “This gives us ideas about what we should be doing for our clients. We don’t want to be complacent…if you are complacent, you are dead.”

Himebaugh said such conversations across the income spectrum help him to better manage his business.

In fact, Himebaugh says his firm is known for its due diligence—whether it be as a 401(k) consultant on the 3(38) side to other financial advisors and employers or serving its private clients.

“We speak directly to the portfolio managers, whether it’s a mutual fund or a separate managed account,” he said. “We look into the eyes of the manager to make sure that we are understanding their investing philosophy,” Himebaugh added. “It really makes a big difference when you do real due diligence that is 25% quantitative, and 75% qualitative. So, we concentrate on making sure that the manager does what they’re supposed to do so we can allocate efficiently to each individual client.”

As a double major in business and economics major in college, Himebaugh always had an interest in finance, and in how money and markets worked. He and his co-founding partner, Richard Zipkis, received their early training at firms including DLJ, Bernstein and then Credit Suisse.

“We just got frustrated with how firms did things for their own benefit over the clients,” Himebaugh recalled. “And we wanted to create an antithetical environment to that philosophy by always putting the client first. People say it, we do it.”

Their own firm started off as a family office practice catering to mostly wealthy families around the country, providing a full complement of services.

About 10 years ago, a private business-owner client of Granite Groups wanted to provide the same money management he was personally receiving within the 401(k) for his employees.

At first, GGA resisted because Himebaugh insisted on maintaining a high-level of ethical standards by not being paid by the mutual fund. After figuring out the proper way to avoid compensation compensated by mutual funds, GGA Retirement was born.

At first, GGA resisted because Himebaugh insisted on maintaining a high-level of ethical standards by not being paid by the mutual fund. After figuring out the proper way to avoid compensation compensated by mutual funds, GGA Retirement was born.

“The ethical standard really is we don’t have anything to sell,” he said. “We have a process that works, but we have no proprietary products. And that allows us to go out and pick from any private or public investment in the world,” Himebaugh emphasized.

He noted that his firm sits on the same side of the table as the client. All the vendors, the custodians, the managers, and all the record keepers and everyone else is across the other side. “And that gives us free reign to hire and fire,” Himebaugh said.

That’s an important structural distinction, which is also much safer in his view, from bigger firms.

“Instead of having a vertical as the advisor, the manager and the custodian, we take that model and put it aside,” Himebaugh explained. “We have independent managers, Granite Group, and an independent custodian. And that creates a system of checks and balances.”

GGA also uses a rigorous quantitative and qualitative fund selection process aimed at delivering strong investment outcomes for your clients. Coupled with the firm’s structural foundation, Himebaugh believes it affords a good combination of safety and great returns over a long period of time.

“So, that’s how we relate to our clients — whether they’re a private client with us that have 10, 20, 30, or 100 million dollars with us or 401(k) with us — the process is the same,” he said.

Himebaugh notes that most investors and advisors tend to look at everything through rose-colored glasses.

“That’s not how we work, and not how things should work,” he said. “We will look for things that can go wrong. “We will look for things that can go wrong. When we can’t find items that are wrong, that is when we buy.”

Assessing the downside is standard operating practice for both arms of the business—whether it’s GGA providing consultation to other financial advisors and employers on 401(k) management, or Granite Group advising individual clients directly.

On the private side, clients may be wealthy individuals, a foundation, endowment, a family business, or a profit-sharing plan. On the 401(k) side, it could be managing a 401(k) or 457(b) plan. Some become clients of GGA directly, while others come to the firm through advisors and GGA will often partner with the advisors.

“We manage money,” Himebaugh said, “We do our best to duplicate what we do for private clients inside the 401(k). That means managed money and a system for the employee to get the right allocation for them and not a product. That’s why advisors hire us.”

For more information on GGA Retirement, visit: granitegroupadvisors.com