Companies weigh new options to raise capital

Traditional IPOs – already facing tough competition from special purpose acquisition companies – are expected to encounter further challenges in 2021 as new rules for direct listings provide another path for companies to raise funds through public markets.

On December 22, 2020, the Securities and Exchange Commission approved new rules for the New York Stock Exchange allowing a company to raise new capital by selling shares through a direct listing of its stock. Previously, direct listings could only be used to sell stock already owned by executives or investors – not to sell new shares and raise additional capital for the company itself.

Approval for the new primary direct listing capped a year during which the IPO market had already been upended by the dramatic rise of SPACs (special purpose acquisition companies, also known as blank-check companies). SPACs are publicly-listed companies that raise money through the markets, yet have no operating businesses. They are formed strictly as platforms to finance the acquisitions of private companies and take them public through a reverse merger with the SPAC.

During the late 2010s, SPACs exploded in popularity, accounting for almost half of all IPO activity in the United States by 2020. Statistics from Renaissance Capital at the end of November indicated the IPO market had enjoyed its best year since 2014, with 194 traditional IPOs raising $67 billion. However, during the same period, 200 SPACs raised $64 billion. By the end of the year, SPAC Research reported, 247 SPACs had raised $83 billion. The uptick corresponded with a surge in M&A activity overall as the economy rebounded from its mid-year decline.

Both SPACs and private listings have benefited from regulatory and marketplace changes that make them more useful vehicles for companies to raise money. They are also growing in popularity because they offer less expensive and more flexible alternatives to raising funds through the traditional IPO process.

To illustrate the pros and cons of each technique, consider how the traditional IPO, and then contrast it with the newer funding choices.

Traditional IPOs Bounce Back

Taking a company public is a significant milestone in an enterprise’s journey from start-up to thriving business. Going public enables the company to raise new capital from the general public for additional expansion and allows its backers to more easily reap profits from their investments.

For centuries, the vehicle to accomplish those goals has been the initial public offering (IPO). An IPO allows a company to list its shares for sale to the public on U.S. stock exchanges such as NYSE and Nasdaq. Once the company is listed for the IPO, it can raise more money through future secondary stock offerings. However, becoming a public company through an IPO is a cumbersome and expensive process. The process begins with a pre-marketing phase in which teams of underwriters, investment bankers, lawyers, and regulatory compliance experts conduct due diligence on the company. They help prepare the necessary paperwork to obtain regulatory approval, such as an S-1 form with the SEC for approval. Investment bankers may also conduct “road shows” where they present the company to potential investors ahead of the IPO, helping them set an initial share price for the stock. Underwriters can also guarantee demand by pre-selling shares through their network of investors (often at discounted prices). Once the IPO is approved and its shares listed on an exchange, the company begins selling stock to the public.

However, becoming a public company through an IPO is a cumbersome and expensive process. The process begins with a pre-marketing phase in which teams of underwriters, investment bankers, lawyers, and regulatory compliance experts conduct due diligence on the company. They help prepare the necessary paperwork to obtain regulatory approval, such as an S-1 form with the SEC for approval. Investment bankers may also conduct “road shows” where they present the company to potential investors ahead of the IPO, helping them set an initial share price for the stock. Underwriters can also guarantee demand by pre-selling shares through their network of investors (often at discounted prices). Once the IPO is approved and its shares listed on an exchange, the company begins selling stock to the public.

An IPO carries a number of benefits to companies, such as increased prestige, better access to capital, and more flexibility to make acquisitions. Consumers can benefit by the additional transparency arising from SEC regulation and public disclosures. However, the IPO process itself is expensive, with investment banks and other professionals charging hefty fees for their work. The company stock can also fall short of the IPO target price if investors in the often-volatile IPO market do not value the company’s stock as highly as the underwriters anticipated.

Direct Listings Gathering Steam

Direct listings (aka direct public offerings) have a long history in the marketplace but were rarely used in prior decades. The best-known companies going public via direct listings were Spotify in 2018 and Slack in 2019. Over the past year, the NYSE and Nasdaq proposed new rules to expand their use. In August 2020, data-miner Palantir Technologies and software firm Asana avoided the turbulent IPO market by using direct listings, drawing additional attention to the technique.

A typical direct listing appeals to private companies that do not need to raise new funds in the public market yet have investors or executives who want to sell their shares on the broader public market. Direct listings do not use underwriters to help establish demand and prices for their shares. This reduces expenses by eliminating underwriting fees (although investment bankers still advise on the listing). However, it also brings more risk of price volatility on the open market.

The outlook for direct listings increased dramatically at the end of 2020 when the SEC approved new rules for the NYSE for a hybrid approach called the primary direct listing. Companies will now be able to sell new shares and raise capital through the direct listing while sidestepping Wall Street underwriting fees. Companies and their investors can avoid “the pop”: the common gap between the initial price investment bankers set to open trading and the higher prices the stock draws during first day of trading. A commonly-cited example is Airbnb, which targeted $68 per share but opened at $146.

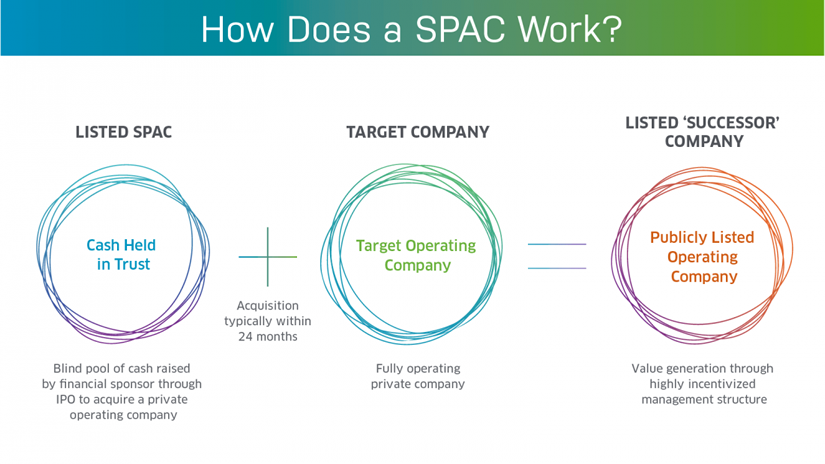

SPACs Quadruple During Pandemic

Like direct listings, SPACs (aka blank-check companies) have been around for decades. They have fallen in and out of favor before becoming widely used in recent years – especially after the COVID-19 pandemic disrupted public markets during the first half of 2020. The vehicle grew from 10 SPACs raising $1.4 billion in 2014 to 59 SPAC IPOs at $13.6 billion in 2019, according to SPAC Research, before quadrupling in 2020 to $83 billion and 247 SPAC IPOs. The sector has drawn numerous high-profile financial professionals (and even celebrities) planning to leverage their skills and connections to find and facilitate profitable M&A deals. SPACs are publicly-listed shell companies that have no operations, existing solely as vehicles to buy other companies. SPAC investors buy shares in the SPAC’s IPO on the assumption that its organizers will be able to find suitable acquisition candidates within their target industry. Units typically run $10 each, and include one share, warrants to buy more stock, and sometimes convertible rights.

SPACs are publicly-listed shell companies that have no operations, existing solely as vehicles to buy other companies. SPAC investors buy shares in the SPAC’s IPO on the assumption that its organizers will be able to find suitable acquisition candidates within their target industry. Units typically run $10 each, and include one share, warrants to buy more stock, and sometimes convertible rights.

Sponsors pay the legal and underwriting costs to list the shell company, following the S-1 process for a typical IPO. The SPAC then sells shares to raise capital and has two years to find a suitable acquisition target. When the SPAC agrees to merge with a private company, it files an S-4 form with the SEC that covers much of the same ground as a normal S-1, ensuring transparency.

The SPAC approach brings several advantages. Sponsors typically get a 20 percent stake in the SPAC (known as the “promote”) in exchange for covering the startup costs, and end up with a significant stake in the target company for relatively little cost. Investors who buy SPAC stock can sell their shares if they do not want to back the company being acquired, or they can keep their interests in the newly-merged entity. The acquired company becomes a public company without incurring many of the expenses and delays of a typical IPO, a strong draw for private equity firms taking their portfolios public. On the downside, if the SPAC is unable to make a deal within two years, the money it raised is returned to stockholders (often with interest).

However, SPACs’ current popularity could also weaken their success in the near future. The explosion in blank-check companies means more SPACs fighting for limited number of attractive take-over targets. (In October 2020, 27 SPACs that launched in 2019 were still seeking deals.) With only two years to complete a merger, some SPACs could find themselves making less-than-ideal acquisitions or returning investors’ funds. SPACs also got a big boost from the poor IPO market during the first half of 2020, reflected in stock underperformance among several newly-listed unicorns such as Uber. But IPOs came back strong in the second half of the year as such successes as Airbnb and DoorDash encouraged more executives to reconsider the IPO route.

With continued growth in both the SPAC and IPO markets, plus the new primary direct listing option now on the table, investors and pundits generally expect more growth in all three funding vehicles as they anticipate a robust market in 2021.