Unless you love leaving money on the table, there's no reason not to shop around for financial products. Whether your mama told you to or not, it pays to explore your options, particularly for checking and savings accounts.

The newest DepositAccounts study examines how much consumers can save — or leave on the table — by shopping (or not shopping) for the best annual percentage yield (APY) on checking and savings accounts, and the numbers are significant. For example, with balances of $1,000 to $25,000, the difference between the lowest and highest checking account APY could mean an additional $51 to $965 in a year.

"Interest rates can vary substantially, especially in today's interest rate environment in which the Fed has raised its benchmark rate to its highest level in more than a decade," says Ken Tumin, DepositAccounts founder. "Banks make money off of customers who don't monitor their interest rates."

In this article, we'll cover:

- Key findings

- How we conducted our analysis (explanation and methodology)

- How much you can save by shopping for the best APY on a checking account

- How much you can save by shopping for the best APY on a high-yield savings account

- What shopping for APYs can do for Americans with the median bank account balance

- We've highlighted what Americans can save, but are they doing this?

Key findings

- Shopping for the best APY on a checking account can boost your balance by as much as 5.1% in a year and 64.5% in 10 years. This is based on a Nov. 3 analysis of checking account rates on DepositAccounts, with APYs ranging from 0.01% to 5.00% on certain deposits. (Read our methodology for more explanation.)

- With balances of $1,000 to $25,000, the difference between the lowest and highest checking account APY can result in an additional $51 to $965 in a year and $646 to $11,685 in 10 years. It stands to reason that consumers with larger (and longer) balances will see the biggest monetary increases, but it pays to shop no matter how much you have in your account.

- High-yield savings accounts typically offer higher APYs than checking accounts, but the boost from shopping for the best APY is lower in this analysis. This is because a single institution offered a 5.00% APY on checking account balances up to $10,000. Meanwhile, the largest APY during our analysis of savings account rates was 3.50%, while the lowest APY was 0.01%. This equates to a balance boost of up to 3.6% in a year and 41.7% in 10 years.

- Using these high-yield savings account rates, the difference between the lowest and highest APYs can result in an additional $35 to $887 in a year and $417 to $10,434 in 10 years. With inflation up 7.7% year over year, every dollar helps.

- Despite the clear benefits of shopping for the best APY on a checking account or savings account, only 43% of Americans say they've done so. This is highest among Gen Zers (51%), residents in the West (48%) and six-figure earners (47%).

How we conducted our analysis (explanation and methodology)

Researchers analyzed the DepositAccounts database of 127 standard checking account and 193 high-yield savings account offerings. We found the lowest and highest APYs for both account types as of Nov. 3, 2022. (APYs may change at any point, so it's important to reiterate our analysis was conducted Nov. 3.)

We looked at four balance amounts — $1,000, $5,000, $10,000 and $25,000 — and assumed one deposit at the beginning of one and 10 years, compounded monthly with no additional contributions.

To determine the value of shopping for the best APY, researchers calculated the balance after one year and 10 years based on the four balance amounts and the lowest and highest APYs. Researchers then calculated the difference by dollars and percentage.

Separately, DepositAccounts commissioned Qualtrics to conduct an online survey of 2,033 U.S. consumers ages 18 to 76 on Oct. 18, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

- Generation Z: 18 to 25

- Millennial: 26 to 41

- Generation X: 42 to 56

- Baby boomer: 57 to 76

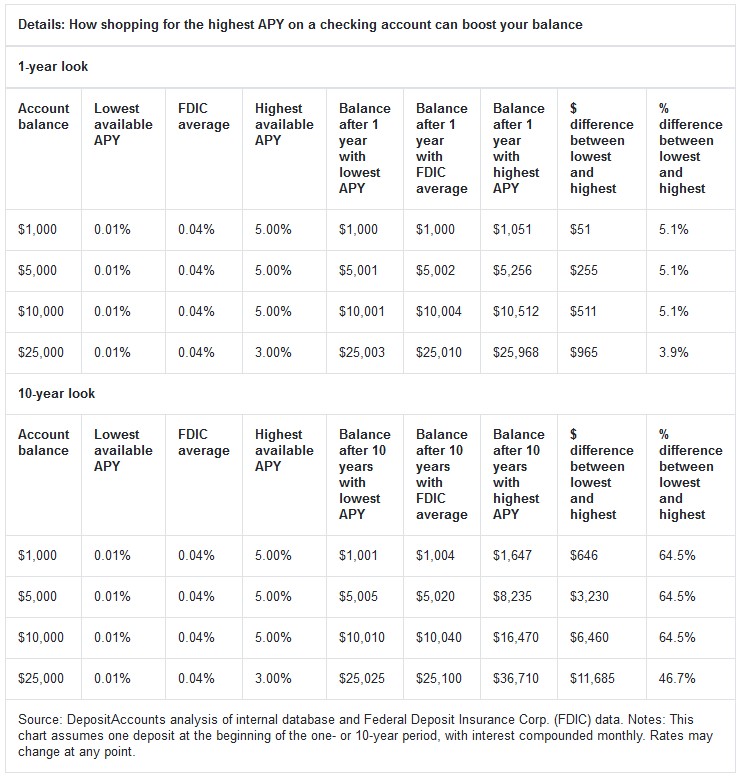

How much you can save by shopping for the best APY on a checking account

First, let's talk checking accounts in the DepositAccounts database, which have widely varying interest rates ranging from 0.01% to 5.00% (as of Nov. 3, 2022). Do those rates make that big of a difference? You bet they do — especially over time, and more so with greater balances.

Say you take the first checking account you see with a 0.01% APY. If you deposit $10,000, you'll earn $1 in the first year. Better than nothing, but if you had shopped around for a checking account with the highest APY of 5.00%, you'd have earned $512 in the same year, which is much better than nothing. After 10 years, you'd earn an extra $6,460 — 64.5% more than the one with the lowest APY.

If you up the ante and deposit $25,000 in an account with the best APY, you can boost your balance by $965 (or 3.9%) after a year and by $11,685 (46.7%) after 10 years than if you had put it an account with the lowest APY. This is despite a lower APY with a $25,000 account balance, as the institution with the 5.00% APY offering capped out at $10,000 as of Nov. 3.

Even with smaller balances over a year, there's money for the taking … or leaving. For example, if you deposit $1,000 in an account with the best APY, you'll earn an extra $51 after a year — a 5.1% increase — over what you would have if you put it in an account with the lowest APY. Over 10 years, you could earn $646 more, an increase of 64.5%.

The average Federal Deposit Insurance Corp. (FDIC) checking deposit rate — as of Oct. 17, 2022 — was 0.04%, which only boosts the balance on a $10,000 account by $4 in one year. But why settle for average when there's money to be made with better APYs?

3 things to look for in a checking account

While interest rates are important, they're not the only factor to consider when you're shopping for a checking account. Other considerations should include:

- Fees: Even more important to compare than interest rates may be the fees a checking account may — or may not — charge. "For the average consumer, fees can be the most important thing for a checking account," Tumin says. "Avoid checking accounts that have any monthly fees. Sometimes a bank will allow you to waive monthly fees with certain balance requirements or with direct deposit. That may be easy to meet when you have a job, but if you lose your job, it may not be easy to meet, and that's the time when you can least afford the monthly fee."

- Rewards and bonuses: Some checking accounts offer debit card rewards programs, usually in the form of cash back on purchases you make. That sounds great, but don't be blinded by rewards as they often require you to meet certain requirements, such as making a minimum number of purchases a month and/or come with annual account fees.

- Ease of use: Do you prefer to do banking in a physical branch or are you always searching for an ATM? Maybe a mobile app is most important to you. Make sure you choose a checking account that is easy to use in the ways you most want to use it.

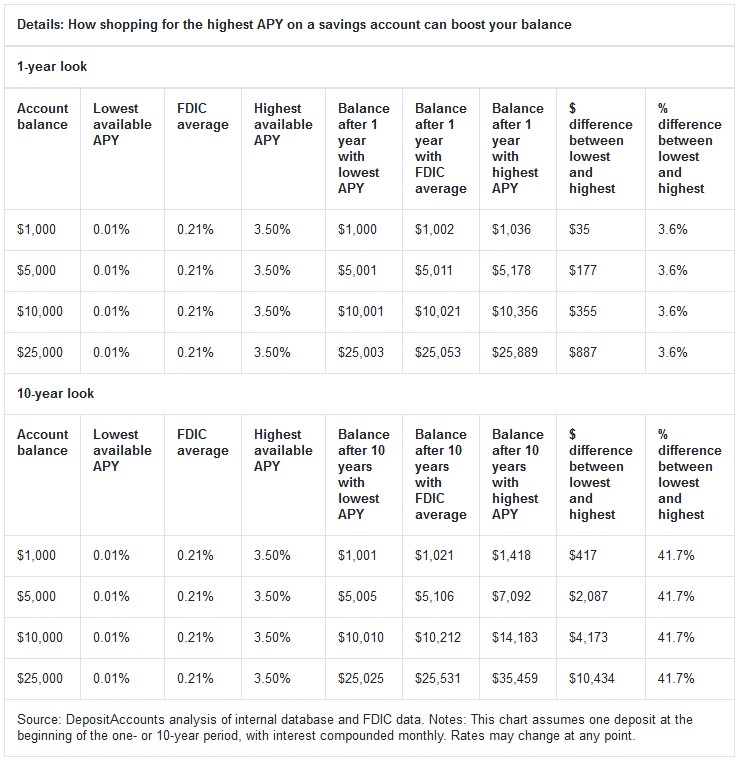

How much you can save by shopping for the best APY on a high-yield savings account

The same type of hefty differences in returns on your money can be found if you shop around for savings accounts with the best APYs. Currently, interest rates are on the rise as the Fed continues to increase its benchmark rate.

According to the FDIC, the national average APY on savings accounts was 0.21% as of Oct. 17, 2022. That's a 23.5% increase from the previous month's average APY of 0.17% on Sept. 19, 2022. Ten years ago on Oct. 21, 2012, the national average APY was 0.08%.

Again, why settle for average? Savings account APYs in our study ranged from 0.01% to 3.50%. That means if you deposit $1,000 in an account with the lowest APY, you wouldn't even earn a full dollar in interest in a year. But, if you choose the one with the highest APY, you would earn $36 in a year.

And the differences are typically more significant with the more money you have in your account. For example, if you deposit $10,000 in a savings account with the lowest APY, you would increase your balance by $1 in a year. If you instead shopped around and deposited the same amount in a savings account with the highest APY, you would boost your balance by $356 — a $355 difference in one year.

3 things to look for in a savings account

There are several things beyond interest rates to consider when looking for a savings account. Online savings accounts typically offer among the highest savings account APYs, so our tips skew in that direction:

- Transfer services: Ensure that the online bank makes it easy to link your checking account to the online savings account and makes it easy to electronically transfer funds with no fees back and forth. "Not all online banks offer an electronic transfer service," Tumin says. "Those that do may charge a fee or have small transfer limits."

- Bonuses: Bonuses can be, well…a bonus for a good savings account, but don't be too quick to pick an account based on them alone. Make sure you understand everything involved, including requirements to receive the bonuses, as well any tax implications.

- Free checking accounts: When looking for an online savings account, look for online banks that offer free checking accounts. "You don't have to immediately move your checking account to the online bank, but the online checking account can provide you another checking account option," Tumin says. "Several online banks offer free overdraft transfers on their checking accounts. If your checking account balance goes negative, a free overdraft transfer automatically takes place to keep the checking account balance positive."

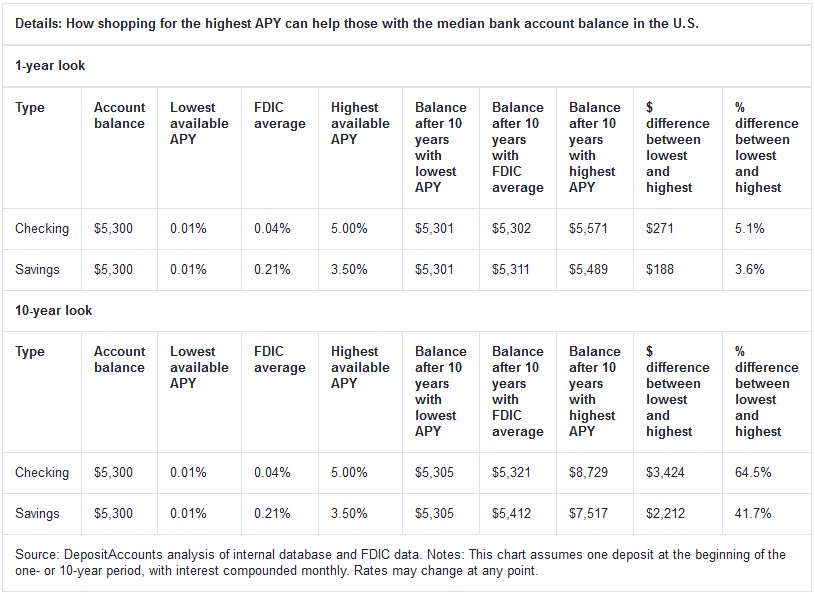

What shopping for APYs can do for Americans with the median bank account balance

Not everyone has a checking or savings account. In fact, according to the FDIC, 4.5% (or 5.9 million) of U.S. households were "unbanked" (i.e., they had no checking or savings account) in 2021.

For those who do, however, the median balance sits at $5,300, according to 2019 data from the Federal Reserve (the latest available). The impact of varying APYs on this amount is similar to the findings in the chart above where we looked at a $5,000 balance, but we wanted to show exact figures based on the median.

First up, checking. Having a balance of $5,300 in a checking account with the best possible rate could mean $271 more at the end of one year than if you put that same money in an account with the lowest APY. As for savings, if you keep $5,300 in an account with the lowest rate for one year, you'll grow your account by $1. If you keep it in the account with the best possible rate instead, you'll bring in $189— a $188 difference.

We've highlighted what Americans can save, but are they doing this?

We know what kind of interest Americans can earn by shopping for the best checking and savings accounts, but the question is if they're doing it. The answer: Not the majority of the time.

Only 43% of respondents in our survey of more than 2,000 Americans say they shop around for the best interest rates for their checking or savings accounts. Men are a bit more likely than women to do so — 46% versus 40%. Meanwhile, younger generations are significantly more likely to than older generations, with 51% of Gen Zers (ages 18 to 25) and 46% of millennials (ages 26 to 41) saying they shop around, versus just 39% of Gen Xers (ages 42 to 56) and 34% of baby boomers (ages 57 to 76). But there's still a lot of money being left on the table by a lack of shopping across the board.

What about once people put their money in a checking or savings account: Is it there for good, or do they continue shopping and move their money from time to time? Sometimes. Half (50%) of consumers with checking or savings accounts report switching banks, but that still leaves half who let their money sit still when there may be better interest rates elsewhere. The top reasons for not bank-hopping include:

- Loyalty to their bank (47%)

- The inconvenience of doing so (29%)

- The benefits their bank provides (23%)

Not doing so and not making sure your APY is the highest means you're likely leaving money on the table.

"You may be earning much less interest than you could earn by moving your money to a higher rate account," Tumin says. "That's especially important in today's interest rate environment. Some people may be reluctant to do this if they don't want to spend the time and effort, but with higher interest rates, there's more money to gain by switching."