The coronavirus pandemic and the resulting social distancing measures have disrupted many aspects of the economy. Employers — many who are dealing with the potential of lower revenue and managing remote work arrangements and the uncertainty of when things will return to normal — may choose to delay or cancel plans to put their defined contribution (DC) plans out to bid. This would significantly impact DC plan sales in 2020.

In April 2020, Secure Retirement Institute® (SRI™) and the Retirement Leadership Forum (RLF) surveyed 14 companies, representing approximately 23% of all U.S. record-kept assets, to explore what recordkeepers expect to happen in the DC market as a result of COVID-19.

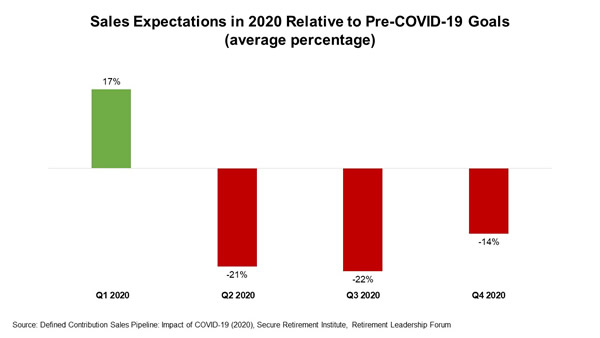

According to the DC recordkeepers surveyed, DC plan sales are predicted to be considerably lower in the second and third quarters of 2020, compared with pre-COVID-19 sales forecasts. The study reveals recordkeepers are optimistic that sales in the fourth quarter will rebound slightly but still fall below pre-COVID-19 expectations.

“This forecast aligns with what we saw during the last financial crisis more than a decade ago. According to SRI research, new plan formation declined nearly 40% between 2008 and 2010,” said Deb Dupont, SRI associate managing director. “During the same period, sales activity for existing plans (takeovers) increased slightly. If the current COVID-19 crisis results in a similar pattern, we would expect a moderate decline in sales with the new-plan/smaller-plan market to be impacted the most.”

The Small-Plan Market Will Experience the Greatest Challenges

The study found recordkeepers that focus on larger plans (i.e., $500 million or more in assets) appear to be faring somewhat better than those not focused on mid-sized and small plans. Generally, they expect their sales to be 5 to 10 percentage points closer to goal, compared with those who target smaller plans.

Researchers suggest there may be several explanations for this difference. Advisors who focus on smaller plan markets may have faced greater business disruptions, whereas the largest plans tend to be more direct- or consultant-sold for whom disruptions may have been less consequential. In addition, the person responsible for managing the DC plan in smaller companies is more likely to be responsible for more than the retirement plan — and more likely to be occupied by the challenges of the present environment.

Also, about a third of sales in the small-plan market are newly formed plans. Given the business disruptions caused by the pandemic, most small employers without a DC plan in place aren’t likely to add one until business normalizes.

The Pandemic Prompts Delays and Shifts Priorities

Survey participants report plan conversions for 23% of new plans or those under contract have been pushed out 3-4 months. However, for sales where a verbal agreement with the plan sponsor is in place, three quarters of surveyed recordkeepers report that on average, 20% have delayed or canceled signing the contract. All recordkeepers surveyed say at least some proportion of plan deals that are in the final stages were delayed or cancelled by plan sponsors.

The pandemic and its economic fallout have had an impact on plan sponsors’ priorities. Employers are placing significantly more importance around helping their workers through financial wellness programs and educational materials and capabilities, as well as higher quality call center capabilities for their participants.

With federal agencies reporting greater fraudulent activities and cybercrime during the pandemic, it is no surprise that recordkeepers report plan sponsors are interested in greater protections against fraud and increased cyber security.

“Insurance companies and recordkeepers have been keenly aware of the increased attacks on retirement plans,” Dupont commented. “Last year our company launched FraudShare, a program that helps financial services companies detect and deter account takeover fraud occurring in the life insurance and retirement markets. To date, 42 companies, representing nearly a third of DC assets, participate in or are in the process of joining the program. Recordkeepers can highlight this tool to provide peace of mind to plan sponsors worried about the security of their participants’ savings.”

While short-term prospects for new DC plan business appear to be unfavorable, historical sales data suggest the downturn will be brief. This research can help recordkeepers develop the tools and offerings that have become increasingly important to plan sponsors.