Insist on Straight Talk

Financial services industry insiders often throw jargon around in client meetings, newsletters, and even marketing materials – but when an advisor uses jargon, what does the client actually hear? Advisors Magazine asked advisors across the industry and across the country for their thoughts on how to relate to clients and why clear, jargon-lite communication matters, even to investors who know their way around financial concepts.

Prospective investors often find themselves overwhelmed by the number of financial terms, products, and advisor qualifications that bombard them during early client-advisor meetings. Less experienced financial advisors may even think industry jargon impresses prospective clients, although typically it just confuses them. Indeed, quite a bit of the financial world’s jargon can be misleading – consider bottom-up investing, for example. And many terms – like the much-discussed word “fiduciary” – can mean different things to different advisors. The result is that many advisors leave their would-be clients behind before the work even begins.  “Effective communication to help investors make informed decisions seems in short supply with no clear uptrend. Too often the dialogue centers around the perceived expertise of the broker, advisor or even the firm and the goals of the client become an after-thought,” said Dave Wilson, social media manager for Fairhaven Wealth Management in Wheaton, Ill. “A good advisor and, for that matter, a good financial services company should be committed to discussing financial topics and strategies in relatable language. No jargon.”

“Effective communication to help investors make informed decisions seems in short supply with no clear uptrend. Too often the dialogue centers around the perceived expertise of the broker, advisor or even the firm and the goals of the client become an after-thought,” said Dave Wilson, social media manager for Fairhaven Wealth Management in Wheaton, Ill. “A good advisor and, for that matter, a good financial services company should be committed to discussing financial topics and strategies in relatable language. No jargon.”

Stripping jargon from the dialog allows the uninitiated investor to join the conversation. Financial literacy continues to lag across the United States, and financial advisors need to break down complex concepts into easy to understand language to make sure their new clients know how their money works.

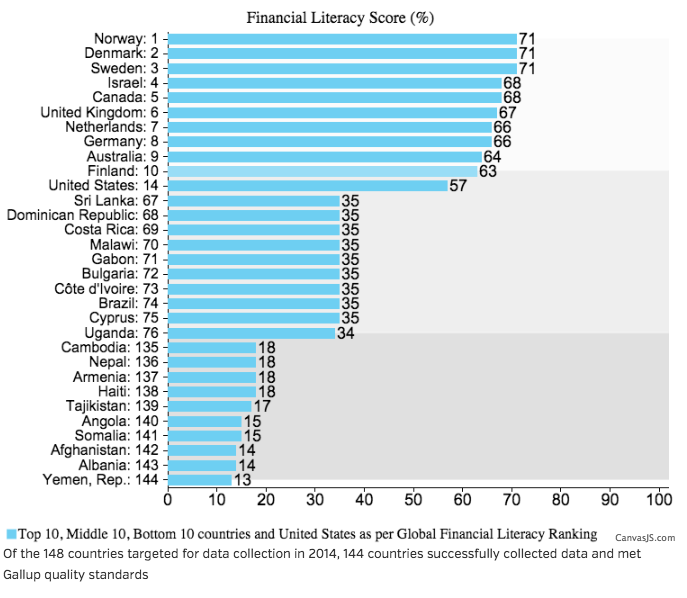

Americans continue to perform poorly on financial literacy studies year-over-year. According to the FINRA Foundation’s National Capability Study, produced every three years, only 37 percent of the 27,564 respondents correctly answers four out of five basic financial literacy questions, down from 42 percent in 2009. FINRA is a quasi-governmental organization that regulates brokers and many Wall Street institutions. The study also showed that America ranks 14th world-wide in financial literacy, above Botswana but below other industrial nations such as Germany. Many advisors pin the lack of financial awareness on limited exposure to money management concepts in schools and universities, and as a result, financial services firms interviewed by Advisors Magazine over the past decade often describe in-house literacy programs designed to get clients up to speed.  “When I was in college and treasurer of my fraternity, I was amazed at how many freshmen did not know how a checking account worked. Looking back on your high school and college days did you have any classes concerning basic money management? I know I did not,” said Jack Meyer, CLU®, ChFC®, the founder of Meyer Wealth Advisors in Aurora, Ill. “In my early years I listened to the instructions of the financial institutions – that’s like having your opponent interpret the rulebook for you.”

“When I was in college and treasurer of my fraternity, I was amazed at how many freshmen did not know how a checking account worked. Looking back on your high school and college days did you have any classes concerning basic money management? I know I did not,” said Jack Meyer, CLU®, ChFC®, the founder of Meyer Wealth Advisors in Aurora, Ill. “In my early years I listened to the instructions of the financial institutions – that’s like having your opponent interpret the rulebook for you.” Investors need to be able to interpret the rulebook themselves, and the rules need to be written clearly. Advisors need to be ready to reframe the “rules” and get clients to the point where they can parse how the rules apply to their situation.

Investors need to be able to interpret the rulebook themselves, and the rules need to be written clearly. Advisors need to be ready to reframe the “rules” and get clients to the point where they can parse how the rules apply to their situation.  “Financial literacy is critical as it helps people make rational decisions when it comes to almost all the essentials in their lives as managing money is the lifeblood of lifestyle,” said Arthur D. Kraus, CAP, ChFC®, an LPL Registered Principal at Capital Intelligence Associates, Inc., based in Santa Monica, Calif. “The absence of financial wisdom leads many of our neighbors into poor decision making and financial stress.”

“Financial literacy is critical as it helps people make rational decisions when it comes to almost all the essentials in their lives as managing money is the lifeblood of lifestyle,” said Arthur D. Kraus, CAP, ChFC®, an LPL Registered Principal at Capital Intelligence Associates, Inc., based in Santa Monica, Calif. “The absence of financial wisdom leads many of our neighbors into poor decision making and financial stress.”

Meyer, for his part, learned several financial lessons through experience, but many investors lack the background or exposure to learn money management as they go. Instead, the average investor needs strong upfront guidance from a solid, trusted advisor.

“A wise man woke me up one day to the fact that if you are not careful you lose much of your wealth to the government, financial institutions, and even other wealthy people. Do people really understand how a mortgage works? How credit cards work? How a 60-day interest-free purchase works?” Meyer said. “The amount of people in the United States living paycheck-to-paycheck is astounding. They are probably, for the most part, hardworking good people. Our industry has a big job ahead – we need to spend more time as a true fiduciary and sit on the client side of the table and educate the public on sound financial principles.”

The term “fiduciary” remains difficult to pin down, with many financial professionals falsely claiming to be one. Most advisors define fiduciary as putting clients’ best-interests before the bottom-line, meaning that insurance agents and product salesmen do not qualify. Still, the average investor usually comes to an initial meeting with a limited, or non-existent, understanding of what fiduciary means, several advisors said. Getting a prospect up to speed on fiduciary and breaking the term down into relatable language goes a long way toward building trust.  “I find that most clients do not know the difference between a fiduciary, a broker or a dual registered advisor. When we meet with a new potential client, we need to explain to them that we are a fiduciary and are required to work for their best interest,” said Israel Guitian Jr., CFP®, a financial advisor at Guitian Wealth Management in Pembroke Pines, Fla. “I think the financial services industry needs to take a holistic approach to helping clients. We need to know that each client is different and that each has different goals and risk tolerances. We need to look to the big picture for each client and do what is in their best interest.”

“I find that most clients do not know the difference between a fiduciary, a broker or a dual registered advisor. When we meet with a new potential client, we need to explain to them that we are a fiduciary and are required to work for their best interest,” said Israel Guitian Jr., CFP®, a financial advisor at Guitian Wealth Management in Pembroke Pines, Fla. “I think the financial services industry needs to take a holistic approach to helping clients. We need to know that each client is different and that each has different goals and risk tolerances. We need to look to the big picture for each client and do what is in their best interest.”

For fiduciary advisors, the concept is simple: the client comes first.  “Unfortunately, all advisors do not consider themselves to be fiduciaries – but we are. When a client entrusts us, we are fiduciaries, period,” said Steve Booren, the owner and founder of Prosperion Financial Advisors in Denver. Booren also is the author of Intelligent Investing: Your Guide to a Growing Retirement Income.

“Unfortunately, all advisors do not consider themselves to be fiduciaries – but we are. When a client entrusts us, we are fiduciaries, period,” said Steve Booren, the owner and founder of Prosperion Financial Advisors in Denver. Booren also is the author of Intelligent Investing: Your Guide to a Growing Retirement Income.

The transition to a more client-focused approach, riddled with fewer pieces of jargon and designed to put the investor first is being driven by the need for customized solutions. Investors today are deluged by financial information and headlines, and sorting through it all to find how their investment goals can be met requires a skilled advisor. Advisors have noticed a shift over the past decade from a sales-based approach where products are king, to a more “consultative” approach built around clients’ financial goals. Smaller advisors tend to have the advantage in this, as they can offer a more personal experience than the major players.

“What clients need is someone who can listen to their financial and non-financial matters and prescribe a roadmap to allow a client to advance on their wishes to what matters.  Unfortunately, the big wirehouses like Fidelity and Vanguard sell on price – assuming cheap results is best,” said Frank Fantozzi, CPA, president and founder of Planned Financial Services in Cleveland. “The investment part of our industry is easy. It is the consultative, financial planning that takes time and effort.”

Unfortunately, the big wirehouses like Fidelity and Vanguard sell on price – assuming cheap results is best,” said Frank Fantozzi, CPA, president and founder of Planned Financial Services in Cleveland. “The investment part of our industry is easy. It is the consultative, financial planning that takes time and effort.”

Relating to clients and developing a relationship based on providing fiduciary advice and financial literacy education requires effective communication. Clients need to hear from their advisors often and with messages that carry useful information – and not just a rehash of what they can read or see elsewhere. As more clients and advisors work digitally, clear communication that provides real value will become even more important.  “I am heavily committed to, and invested in, electronic communications. I have been selling life insurance for almost three decades now. During that time, I have seen the sales process evolve from the ‘kitchen table’ featuring face-to-face meetings with your clients, to remote communications via phone, email, and text,” said Steven H. Kobrin, LUTCF®, founder of the firm of Steven H. Kobrin in Fair Lawn, N.J. “I have served clients all across the country, and have not personally met the vast majority of them. The challenge is, of course, establishing credibility and trust with people that have not met you in person. Thus far, I have been able to establish strong relationships with people remotely, and earn their business.”

“I am heavily committed to, and invested in, electronic communications. I have been selling life insurance for almost three decades now. During that time, I have seen the sales process evolve from the ‘kitchen table’ featuring face-to-face meetings with your clients, to remote communications via phone, email, and text,” said Steven H. Kobrin, LUTCF®, founder of the firm of Steven H. Kobrin in Fair Lawn, N.J. “I have served clients all across the country, and have not personally met the vast majority of them. The challenge is, of course, establishing credibility and trust with people that have not met you in person. Thus far, I have been able to establish strong relationships with people remotely, and earn their business.”

Effective communication leads to a good client-advisor experience. If an advisor wants to relate to clients, developing the right communication strategies and tools is essential.

Electronic or face-to-face, clear communication is the basis of financial education, advisor-investor relationships, and the ability to maintain the ongoing, years-long relationships with clients that will allow them to meet their financial goals. Without it, the relationship risks falling flat and clients can be turned away by what they perceive as an unresponsive – and disinterested – advisor. Many advisors would even consider clear communication to be a part of their fiduciary responsibility to clients.

“‘Intentional relatability’ is our mission at Fairhaven,” said Wilson of Fairhaven Wealth Management. “We cannot help our clients achieve their goals without effective communication and that starts with relatability.”