Financial literacy: filling the gaps.

Industry professionals tend to agree that financial literacy among investors remains surprisingly low. However, the investors who do know the basics might not be any more prepared than their peers.

“Even if someone knows some of the basics: budgeting, saving, investment, and insurance, many still don’t truly understand how the pieces fit together and the value of having a financial plan,” said Ira G. Rapaport, chief executive officer of New England Private Wealth Advisors, LLC. “Not enough is done to promote financial literacy. Sometimes classes are available in high school or college but typically as electives. At that point, most people may not be that receptive as they likely haven’t really started to make any significant financial decisions. Often times, it isn’t until people get their first job, have access to a 401(k), or have to start paying back college debt that financial literacy becomes important to them.”

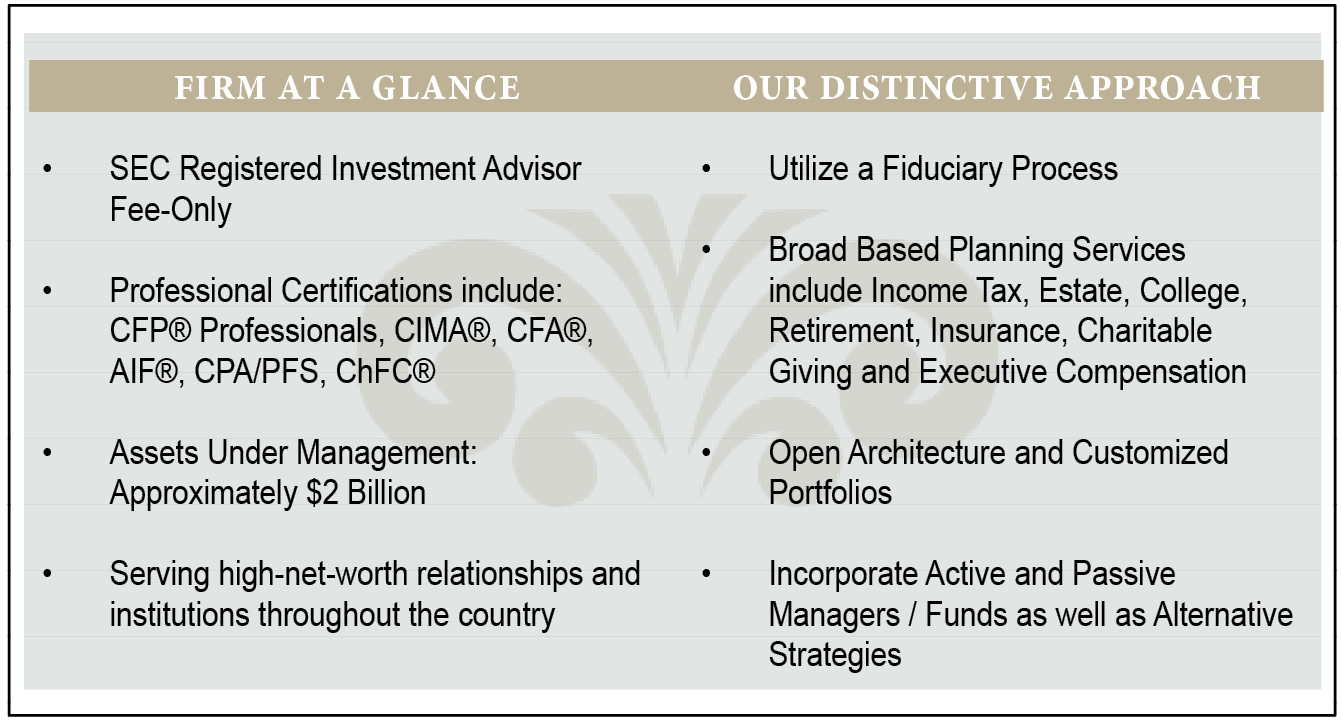

New England Private Wealth Advisors, based in the Boston suburb of Wellesley, provides comprehensive wealth management services to high net worth individuals, families, and institutions. The firm is an independent, fee-only advisor registered with the Securities and Exchange Commission, and they act as a fiduciary, meaning that clients’ best interests come first.  No matter how many studies experts conduct on financial literacy, the results remain stagnant.

No matter how many studies experts conduct on financial literacy, the results remain stagnant.

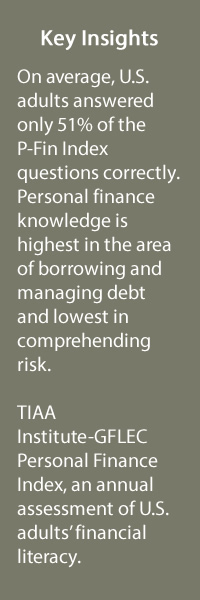

The 2019 TIAA Institute-GLFEC Personal Finance Index Study – which measures financial literacy and wellness annually – found that American adults could correctly answer just 51 percent of the survey questions, on average. The 2019 results topped 2017 and 2018, but only by 1 percentage point year-over-year. The study results show that many Americans lack the skills to manage their own money, and with that comes the risk that they may fail to fully prepare for emergencies, market downturns, and/or retirement.

Those with greater financial literacy are more likely to save and plan for retirement,” Rapaport told Advisors Magazine. “Eighty-eight percent of those with high financial literacy save for retirement on a regular basis, compared to 37 percent of those with low financial literacy.”

New England Private Wealth Advisors works with clients to ensure they understand how their money works. Understanding financial concepts can be difficult, especially for busy professionals who need to devote time to their own endeavors, so Rapaport and his team work carefully to find what troubles clients and where the gaps in their knowledge exist.

“Confusion can arise in any conversation. Each party brings a separate base of knowledge, experiences and concerns. This is especially true when it comes to talking about something as emotional as money or retirement,” Rapaport said. “In all of our discussions with clients, it is our job to listen intently, develop an understanding of their point-of-view and concerns, and provide relevant education.”

Clients who master, or at least grapple with, financial literacy will likely be better positioned long-term, Rapaport added. Boosting clients’ financial literacy is key in preparing them to take control of their future and achieve the retirement, home purchase, or investment goals they seek.

“Those with greater financial literacy have a greater propensity to track spending. Sixty-three percent of those with high financial literacy usually or almost always tracked their spending, compared to 54 percent of those with low financial literacy,” he said, citing the 2019 TIAA study. “Those with greater financial literacy are less likely to be financially fragile. Eighty-five percent of those with high financial literacy could certainly come up with $2,000 if an unexpected need arose within the next month, compared to 25 percent of those with low financial literacy.”

New England Private Wealth Advisors works with clients to break down complex concepts into language they readily understand. But there comes a point at which information overload sets in, so Rapaport and his team take care to keep things simple and to present only what clients need.  “Providing clients with choices is important, however, too many choices can lead to confusion and clients feeling overwhelmed,” he said. “We typically focus on presenting the one or two solutions that best meet the client’s need. We then review the solutions presented in detail to help ensure the client understands them fully before making an informed decision.”

“Providing clients with choices is important, however, too many choices can lead to confusion and clients feeling overwhelmed,” he said. “We typically focus on presenting the one or two solutions that best meet the client’s need. We then review the solutions presented in detail to help ensure the client understands them fully before making an informed decision.”

And while commission-based advisors might take a hurried approach to getting a client “in and out,” Rapaport’s team works with investors to make sure they stay focused every step of the way. As a fiduciary advisor, Rapaport does not push products or insist on certain asset allocations, each client is instead taken as a whole and has a custom plan tailored for them.

“We take a holistic view, involving our clients and their spouses in every aspect of the planning process and frequently engage their other professional advisors in the discussion. We welcome any questions and are willing to spend whatever time is necessary to ensure our clients fully understand and are comfortable with any recommendations we present,” Rapaport said. “Depending on a client’s current financial understanding, we tailor our explanations to best help them understand our thought process and recommendations.”

Financial literacy has taken on greater importance as employers continue to reduce retirement support. Whereas pension plans once provided the bulk of a retiree’s income, most firms have cut back and left savers to navigate 401(k) plans, Roth IRAs, and the stock market themselves. A trusted advisor, however, can help fill the gap left by the employers of previous decades.

At the same time, increased longevity has complicated retirement planning. Today’s saver can expect to live roughly six to 10 years longer than their grandparents did, and that future technological or health advances may push those numbers higher. Retirees now face a 10, 20, or even 30-year retirement and could potentially be retired for as long as they were working.

“Longer life expectancies imply individuals may need to depend on their accumulated savings to provide income for a longer period in retirement compared to previous generations. Among evolving personal and family goals, calculating financial needs for a period of more than 20 years can be an extremely daunting task,” Rapaport said. “Since most companies are no longer offering pension plans, individuals and families are now asked to take more responsibility for their own financial security in retirement.” Families can share that responsibility with a trustworthy, fiduciary advisor who can guide them through the steps toward building a sustainable financial plan. Financial literacy is a big part of that as well, as investors need someone who can guide them through the years of evolving financial goals, plans, and shifting priorities.

Families can share that responsibility with a trustworthy, fiduciary advisor who can guide them through the steps toward building a sustainable financial plan. Financial literacy is a big part of that as well, as investors need someone who can guide them through the years of evolving financial goals, plans, and shifting priorities.

“In the years before retirement, working with an advisor and becoming more financially literate can help individuals develop an understanding how to best allocate financial resources to meet immediate needs and maximize the potential for achieving future goals,” Rapaport said.

Many investors may shy away from “education,” feeling that they already are experienced, capable professionals in their own right. But a lack of financial literacy does not mean a lack of education, it means only that the investor is working outside their comfort zone and needs a guide. Investors who have accumulated significant assets face even greater challenges in learning the financial ropes; their assets typically require a detailed approach and a professional eye to ensure sufficient care is taken to protect and grow those investments.

“The vast majority of our clients have been very successful in their lives and typically have a firm grasp on many basic and intermediate level financial concepts,” Rapaport said.

"However, their unique situations often require more sophisticated planning and a greater depth of knowledge or understanding. Our consultative team approach is designed to educate our clients, whatever their situation may be, empowering them to make sound financial decisions consistent with their core goals and values.”

Empowerment is the goal. Investors, whether just starting out or nearing retirement, need to be fully informed to make the best choices possible. Financial literacy is a first step, but developing a strong relationship with a capable advisor also is necessary. Finally, the advisor-client relationship has to be strong enough to build investor confidence to the point of taking action, because days, weeks, months, or even years of financial literacy education amount to nothing if clients fail to use it.

“Clients should look for an advisor willing to serve as a patient educator, providing as much detail and assistance as necessary,” Rapaport said. “The most effective financial advisor is not there to make decisions for clients, but to provide the tools and assistance needed for the client to comfortably make their own prudent choices.”

For more information on New England Private Wealth Advisors, LLC, visit: nepwealth.com