It’s often said that keeping money is much more difficult than making it. Premium financing is one of the tools available to high-net-worth-individuals (HNWI) proven to help retain the optimal value of an estate or legacy while providing the level of insurance protection appropriate to the level of wealth. Evolution, Inc. reports the premium finance industry currently finances approximately $40 billion in life insurance premiums on an annual basis.

As a founding member and principal of Vérité Group LLC and a Forbes Finance Council member, Seltzer has married the disciplines of great finance and insurance protection through premium financing. Rather than placing optimal life protection at odds with optimal insurance pricing, Seltzer has built his legacy through tirelessly researching and transparently informing his clients of the true best solution.

Seltzer began his career in financial services as an accidental recruit selling life insurance as a summer job. His natural aptitude in the field soon found success that extended into a quarter-century of experience in the high-end insurance market. In 1999, he founded his first premium insurance company, Metcap, to offer tax efficient strategies to real estate partnerships and joint ventures. He expanded his base from Greater New York to New Jersey as principal of Insured Capital Management in April 2002.

After founding Vérité in 2009, Seltzer subsequently became an owner in Lion Street in 2015. This combination established Vérité as a national company. Most recently, Vérité has expanded further into the international market with cases in Vietnam, Brazil, Columbia and Hong Kong.

Although Vérité Group exercises a discriminating philosophy when choosing clients and conducting business, readers at all levels can learn a great deal from Seltzer and Vérité. For instance, Seltzer’s focus on quality informs everything he does. “We spend a huge amount of time educating potential clients and client advisors at a very high level,” Seltzer tells us. “We first educate them on the premium finance work that we do and then how that discipline applies to them specifically. The reason that our firm is admired is because our education is akin to full disclosure. After reading our white paper, people know not just the benefits of premium finance, but also the risks. We also tell people quite straightforwardly if they do not yet have the profile to properly receive our brand of high-level financing.”

“We spend a huge amount of time educating potential clients and client advisors at a very high level,” Seltzer tells us. “We first educate them on the premium finance work that we do and then how that discipline applies to them specifically. The reason that our firm is admired is because our education is akin to full disclosure. After reading our white paper, people know not just the benefits of premium finance, but also the risks. We also tell people quite straightforwardly if they do not yet have the profile to properly receive our brand of high-level financing.”

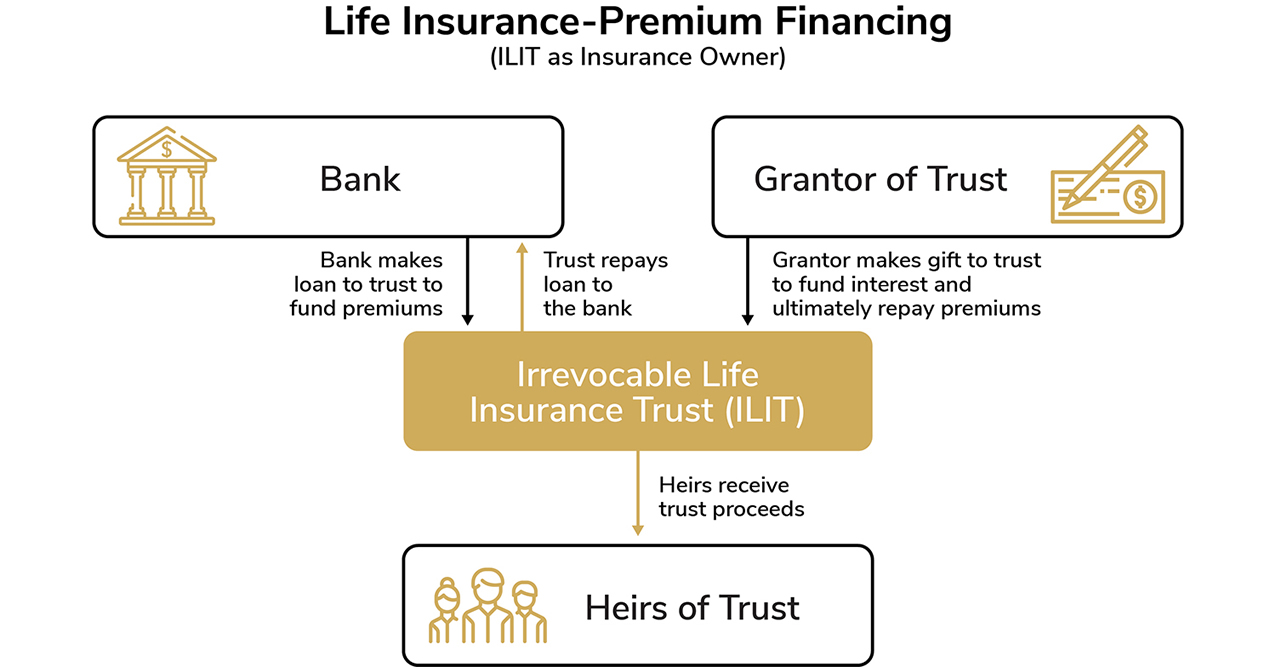

Premium financing takes a personal turn when dealing with legacy planning. Seltzer described to us a scenario in which his firm would save his real estate developer clients tens of millions of dollars in premiums on a life insurance policy. Using leverage, Vérité would be able to grow the policy from $50 million to $100 million by expected time of death.

“Vérité minimizes the need for outside collateral as well,” Seltzer informs us. “We have different methodologies in order to control the cash flow that clients pay into the debt service. No two illustrations of a design are the same.”

Most importantly, Vérité has the ability to fine tune its financial designs to fit the needs of its clients.

“Our designs come directly from accumulated information from the client,” says Seltzer. “Once we have our initial design, we perfect it through conversations with our clients, translating their needs into their optimized financial realities. No one size fits all.”

At the same time, Seltzer provides a word of warning and something to aspire to when comparing his services to the growing amount of accessible financial services applications. We had to ask the question – with technology putting the financial services market within reach of everyone with no middleman, is there any correlation between what Vérité achieves for its clients and what a high net worth individual might achieve for himself?

“The answer is no,” Seltzer warns. “There are no self-service online apps that I’ve seen that deal with premium finance. The commercial apps that most people can utilize are usually at the low end of the market. It completely shocks me that some of our very wealthy clients have their fortunes with an online broker system – hundreds of millions of dollars with no professional advice of any kind should that money need to be moved or utilized.”

J. D. Power conducted a study that found self-service apps to be far too text heavy and lacking in security. Although 69 percent of HNWI use mobile banking apps, they yearn for a personal connection with their wealth managers. Seltzer gave us some poignant insights as to why people at the level of wealth he considers (around a $5-10 million minimum net worth) – of whom one would assume a corresponding level of sophistication – might still engage in robo-technology too heavily.

“As rich as these people are and as smart as they are, they don’t know who to trust. As a result, they just push everybody away,” Seltzer notes. “We had a San Francisco client with a net worth of $100 million who got suckered into a really bad deal. We had to aid him in litigation to get him out of it.”

“A lot of people procrastinate about buying life insurance whether financed or not. People don’t want to pay large premiums, people don’t want to discuss their demise, people feel skeptical about a product they do not understand,” Seltzer said. “A lot of it has to do with control and facing your demise as well. Others simply don’t want to pay for the appropriate amount of insurance. My experience is that all of these are mental blocks that people have when it comes to escape planning and insurance planning.”

This is not to say that cautious behavior is not warranted. If you are looking into the premium finance market, you must be careful who you talk to. One of the major negative trends that Seltzer told us about was rogue insurance agents who claim to have knowledge of premium finance while having none. The proliferation of technology without a matching security function also increases instances of fraud. According to iii.org, no surveyed insurance company in any level of business has reported a decrease in fraud over the past six years

.

“We see more and more deals on a regular basis that are blowing up because they are not situated right,” says Seltzer. “Banks need to have some discipline about how they distribute premium finance loans and premium finance products. The consumer can be best protected by the due diligence of insurance carriers and lenders, not regulators.”

So according to Seltzer, what is the first question that someone seeking premium finance advice should ask? The answer is easier than you think – simply check their website. Vérité Group has a wealth of information that you can reference before you get Seltzer on the phone personally to discuss your insurance needs. 40 years of life insurance experience taking back the word “premium” has given him the experience to customize a plan with optimal value for your life.

For more information about Vérité Group and Lion Street, visit veritegroupllc.com and lionstreet.com