As a consultant to some of the best and brightest financial advisors, CPAs, and attorneys in the Southeast, I spend my time helping financial professionals land more high-net-worth clients. If there is one thing these investors are accustomed to it is personalization. Whether it is buying a house, a car, or a portfolio, wealthy investors want their purchase tailored to them.

As advisors, we must be able to articulate our formula for portfolio customization to our clients. For high-net-worth clients, I often find that there are three main tenets of a custom approach, which I outline below.

Pillar 1: Personalized Portfolio Management

One of the cornerstones of a custom strategy is the ability to personalize a portfolio. High-net worth clients tend to be sophisticated investors with complex needs — assets in many different places and in many different types of vehicles. Each client has unique investment goals, and many also express the desire to align portfolios with their moral compasses and personal feelings about the economy or markets. In addition, it is rare that a client comes to a manager with a completely blank slate, so we often need to work around existing portfolios, unrealized gains/losses, and other behavioral biases that may exist with the client and his/her investment holdings.

To meet the goals and expectations of high-net worth clients, investment consultants and portfolio management teams work with clients to develop unique plans for each unique goal. Once the plan is in place, an Investment Policy Statement that serves as a guide for portfolio construction and investment decision making is typically built, basically putting the plan into a formal document.

ANALYTIC TOOLS

Investment firms and industry software typically will include personal benchmarks to measure each portfolio’s performance and adjust investment allocations to suit client goals and objectives. Using analytic tools, advisors can develop a plan based on each client’s target return goals.

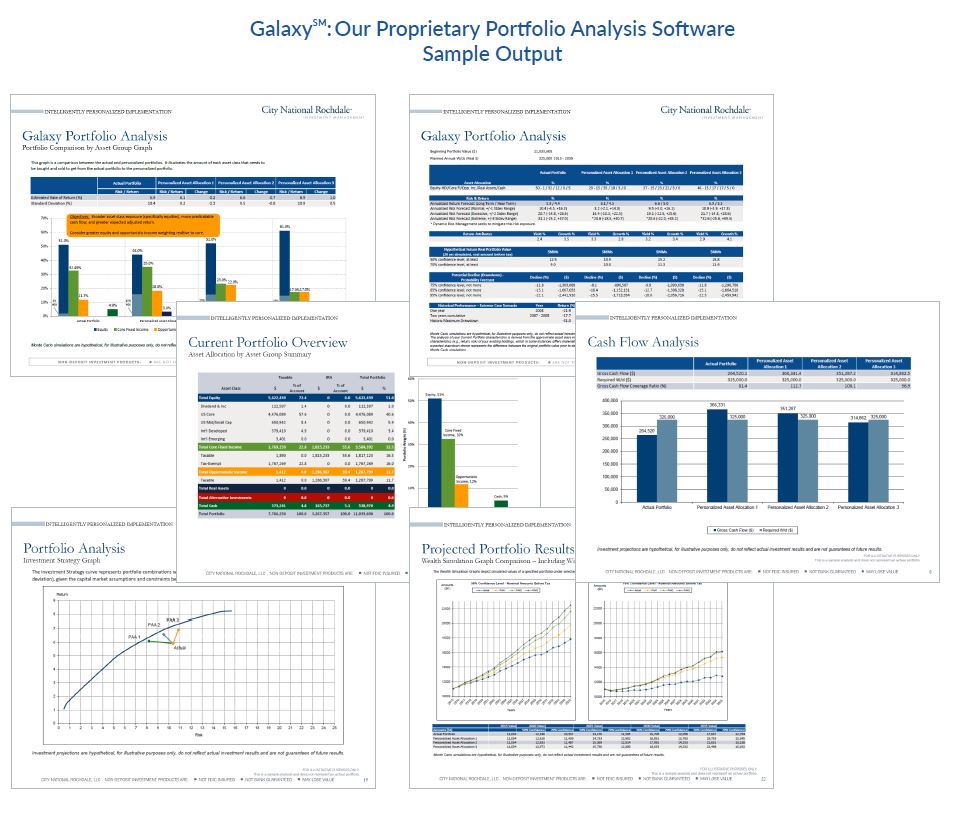

Our firm uses proprietary portfolio analysis software to help illustrate how our custom strategies work for each client. We input key data about the client’s portfolio and investment strategy into the tool, which simulates the portfolio’s outlook over the long term and helps give clients a complete financial picture. The result is one comprehensive report that takes a holistic look at clients’ assets — retirement accounts, trusts, IRAs, etc. — including the tax aspects. Based on variations in strategies and asset allocations, the software generates possible portfolio outcomes.

What makes this tool particularly powerful is that it’s not just a hypothetical portfolio — it shows the possibilities for a client’s existing assets. With these simulations, clients can compare and contrast our recommendations to what they’re currently doing. Software and analytical tools are very important in advising high-net-worth clients and building custom strategies.

Pillar 2: Active Tax Management

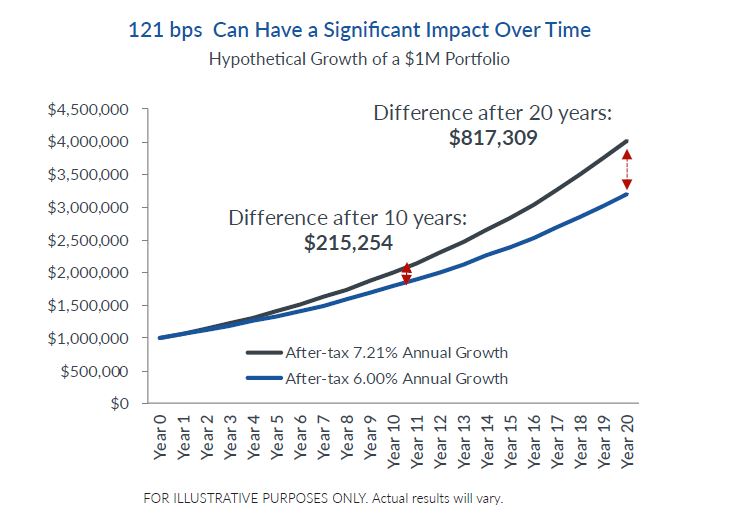

Active tax management is a key element of any wealth management plan. While it is difficult to pinpoint what percentage of after-tax return is added through tax alpha, our in-house study shows that it may be up to 121 basis points.1 Over time, this can have a significant impact. Furthermore, the lack of tax management can cost an investor as much as 25% of returns.2

Prudent advisors take a methodical three-step approach that is a function of open communication among the client, financial advisor, tax professional, and portfolio manager:

STEP 1: Planning and Tax Budget

One key element of the Investment Policy Statement is tax. Advisors must formulate a tax budget for each client which defines the annual budget for ordinary income, short-term gains, and long-term capital gains.

The portfolio manager should work closely with the client’s financial advisor and tax professional (CPA) to develop and manage the tax budget.

From the very start of the relationship, when clients transition assets to their manager, the firm should proactively manage to the tax budget. That budget then becomes an ongoing part of the portfolio’s active management at money management firm.

STEP 2: Asset Location and Implementation

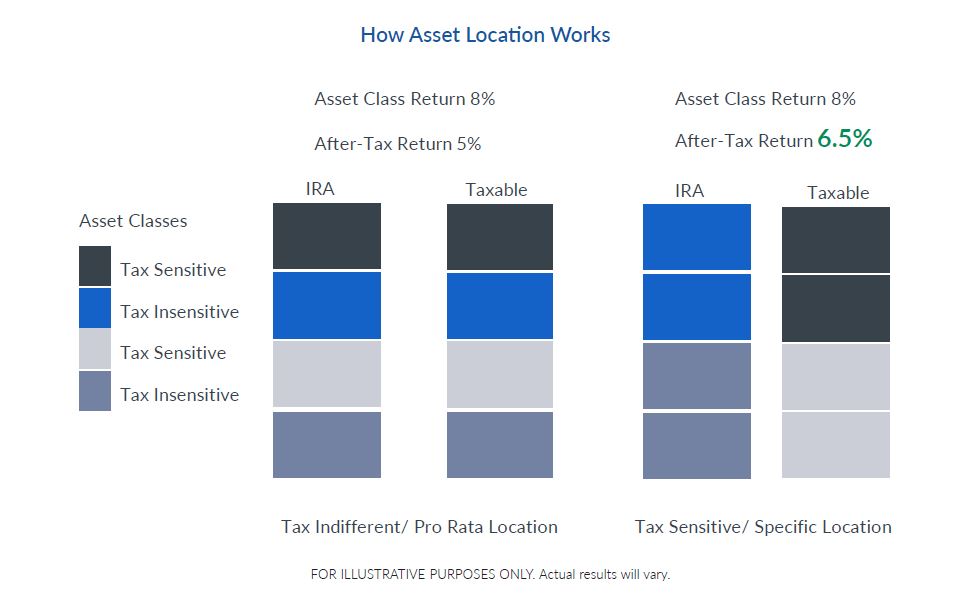

As advisors begin building a client’s portfolio, the first consideration of active tax management is the concept of “asset location”— in other words, putting the right securities in the right accounts to create tax efficiency and maximize the client’s after-tax returns.

Asset location also applies to the mutual fund space. We typically prefer to minimize mutual fund holdings in high-net worth client portfolios, opting to own individual stocks and bonds as core holdings. However, we understand that there are situations in which mutual funds may be appropriate (particularly with regard to specific market niches). Mutual funds distribute their capital gains annually, which can provide a tax management challenge. Nevertheless, we strive to implement appropriate strategies to minimize the tax burden.

STEP 3: Tax Budget Management

Portfolio managers take active steps toward managing to the client’s tax budget and finding efficiencies where possible through strategies such as:

Long-Term Capital Gains

Realizing Losses

Offsetting Gains with Losses

Tax Lot Management

The key to tax management is ensuring that the financial advisor, the accountant, and the portfolio manager are all on the same page. Good advisors take pride in their work helping clients create and implement their own customized tax plans.

In our next column, we look to explore more about these individual steps and strategies, as it relates to tax management in portfolios.

Pillar 3: Customized Risk Management

Last, but not least, any sound investment management plan includes a robust risk management strategy. A good advisor should customize these strategies to each client — a necessary step since individuals have unique levels of risk tolerance. Investors tend to dislike losses more than they like gains — a concept known as loss aversion. At the same time, some risk is necessary to achieve financial goals. It’s our job to help clients develop and define a risk budget and then adjust the investment strategy to match.

Perhaps the most salient story about the markets recently has been the return of volatility. The U.S. is currently nine years into the bull market, and the present economic expansion is on its way to becoming the longest in history. Eight years of federal intervention has suppressed market volatility and minimized the need for risk management as a source of alpha.

However, many market participants believe the extended period where low volatility and beta have dominated will change over the next few years. When the market declines, active risk managers have historically outperformed beta managers since active managers have the ability to reduce risky asset exposure and take advantage of opportunities.

Sound risk management solutions should provide active risk management techniques such as strategic asset allocation, rebalancing, and downside loss controls, implemented through three levels of portfolio risk management:

LEVEL I: Strategic Asset Allocation

As a first step, one would custom-build a portfolio for each client’s investment goals using the appropriate asset allocation, seeking an efficient risk/return trade-off. I like to think of this as designing your asset allocation plan, utilizing the tenets of modern portfolio theory and hoping to end up somewhere close to the efficient frontier.

Most “do-it-yourself” investors stop here.

LEVEL II: Dynamic Asset Allocation

Research and economic factors should drive strategic and tactical investment decisions. Research teams at investment firms should proactively monitor changing risk factors over time, including risks associated with individual sectors or securities. This should lead to the overweighting and underweighting of various asset classes as they come in and go out of favor. The goal here is to have an opinion and then do something about it and strive not to be the type of advisor that says, “here is what is going on in the economy, but let’s stay the course, hold your hand and never do anything about it.” Let’s be the type of planner that says, “here is what is going on and here is what we are doing about it.”

Some investment firms employ this but most stop here.

LEVEL III: Personalized Downside Risk Management

Managing volatility is especially important during non-normal market periods. The ability to customize a risk plan is an important piece of a personalized approach. Having the ability to develop a unique risk budget for a client allows the consultant to potentially limit losses in the portfolio while adhering to the client’s overall risk budget.

RAISE CASH TO MANAGE AND MITIGATE RISK

During times of adverse market conditions, an advisor may recommend a move to cash based on a recession outlook. Individual portfolio managers managing custom portfolios can then tailor the amount to move based on guidance from the firm’s asset allocation committee and adjust based on each client’s personal strategy and risk tolerance.

What makes risk management strategy powerful is when it’s customized to each client, providing a truly personalized investment management experience. No two investors are exactly alike, and so no two risk strategies at the firm can be exactly alike.

Conclusion

I believe differentiated and sophisticated investment management capabilities can help clients grow and protect their assets, further increasing the probability that they achieve their financial goals. The three key tenets of portfolio customization add further value for clients. Through personalization, tax management, and risk management, portfolio manager are empowered to implement and customize individual strategies which are tailored to each client.

Each client’s dedicated portfolio manager should personally implement and manage the investment strategy after crafting the Investment Policy Statement and further assess the current market volatility along with any updates to the client’s personal situation. After this, the advisor should make the appropriate changes to each individual client’s portfolio. Good advisors will consistently examine the portfolio to expose inefficiencies and highly additional investment opportunities.

![]()

1Average tax alpha generated between 2008 and 2017 from five randomly selected real client accounts (from five separate senior portfolio managers) used in a City National Rochdale internal study. For more information, see our white paper, Tax Alpha: Enhancing Returns Through Active Tax Management.

2Weinberg, Ari I (2012, October 16). A magical tax-loss harvesting machine? Forbes. Retrieved from https://www.forbes.com/sites/ariweinberg/2012/10/16/a-magical-tax-loss-harvesting-machine/#6f09b0f47a5e