Do retail investors move markets? Did an influx of funds from retail investors drive the recent stock market rebound?

While the debate continues over how big a role private investment played in the recovery, San Francisco-based lender Stilt, Inc., has added its own analysis indicating a direct correlation between investments through the Robinhood app and the spring 2020 rebound of the S&P 500. When the stock market bottomed out the week of March 16-22, Stilt research found Robinhood also experienced the largest inflows of retail investments. As the S&P 500 rebounded through mid-May to recover more than half of losses, Robinhood also saw a major influx of retail investments.

Research by Bespoke Investment Group focusing on lower-priced shares also concluded Robinhood activity played a significant role in the markets’ recovery. However, not everyone reached the same conclusion. A June study by Barclays PLC analyzing at the entire S&P determined when more Robinhood customers bought a stock, the result was lower returns rather than higher ones. Industry analysts also suggested the May rebound was more driven by such factors as low interest rates, $2 trillion in government stimulus, and Federal Reserve actions to backstop securities and bonds.

The Stilt research was based data about its customers’ activities. Stilt primarily targets recent immigrants for its loan products. As a part of the application process, applicants agree to link the Stilt platform with their bank accounts. That connection provides Stilt with information at a transaction level to support credit decisions – and with raw data for further analysis.

The company’s Robinhood study was based on 5,000 randomly selected applicants who applied for new loans with Stilt during the first five months of 2020. These applicants ranged from 18 years old up to as much as age 80, although the customer base skews more to the younger ages.

The company added in its blog about the study, “With COVID-19 still a significant impediment to stock market health in the U.S., it remains to be seen if retail investment on Robinhood will continue to drive stock market recovery.”

Since the study, Mittal added, his firm has seen consistent Robinhood activity by its customers, but no real increase in the amount of money invested.

The Robinhood study is one of many that Stilt undertakes using customer data. For example, the company recently found that immigrants prefer the cash transfer app Zelle over Venmo.

“We do a lot of analytics,” Mittal said. “Our team is constantly analyzing the data to learn more about our customers and their habits. We have massive datasets that we are constantly analyzing for insight. When we find something interesting, we make it a blog post and share with everyone.”

Data analysis is a key component to Stilt’s corporate mission to bring more financial services to recent immigrants and underserved American.

Mittal said the company grew from the obstacles he and co-founder Priyank Singh encountered as recent immigrants attending Columbia University. When he moved to the United States to pursue his masters, he was unable to rent an apartment in New York for several weeks.

“Everywhere I went, people would ask for a credit report, or a co-signer, or for six- to 12-months’ deposit. I had none of those things. I had to sleep on a Columbia alumnus’ couch for three weeks while searching for an apartment, said Mittal.”

Singh, a roommate in the apartment, had been through similar struggles when he came to New York the year before. When he moved out, he rented Mittal a room in his new apartment.

Finding an apartment is one example of the many financial challenges new immigrants encounter, Mittal said. It is difficult to get credit card or any kind of loan. (For example, when Singh began working at Microsoft, he had to take public buses to the office because he could not get an auto loan.)

After graduation, Mittal was employed by a credit consulting firm in New York before moving to the West Coast to work as a data scientist. Mittal and Singh began working on side projects based on the previous experiences. One of those side projects evolved into Stilt, Inc., which the former roommates co-founded in 2015 and launched through the Y Combinator startup program the following year.

“Our personal experiences, plus my experience working in credit analytics, promoted us to think about different ways of solving this problem for the immigrant population,” Mittal said. “That's why we started the company: all of our friends, our colleagues, everyone we knew had faced similar challenges. We were just trying to build something that would make their lives easier.”

Access to most financial products in the United States is based on credit scores and credit history, he noted. New immigrants often do not even have a Social Security number. Even then, it can take at least six years to build a strong enough credit profile to qualify for high-qualify credit products.

“Because of this problem, many immigrants have to resort to sub-optimal solutions – or they just have no solutions at all, “Mittal said. “It’s a burden on your parents back home because you have to constantly ask for them money. It creates a host of problems without any real solution. You can't take money from friends. You can't really go to a bank and you really don't have personal savings. Immigrants are on a back foot for years until they settle, get a job, and build their credit.”

The company initially focused on immigrant students and has slowly branched out. Many students take out loans in their home countries but find those funds do not last long in the United States. Even after graduation, many need money to relocate for a new job, buy a car, or secure housing. Stilt’s first product was a personal loan that could be used for many purposes.

Mittal describes his firm as a fintech – a technology company operating in financial services industry. Every aspect of the business is technology-driven.

“Looking at people without a credit history requires a lot of technology,” Mittal explained. “We use the latest in machine learning in customer service and underwriting loans. That allows us to scale the business. Today we are a total of 16 full-time employees serving many thousands of customers.”

Mittal said the company takes a broad look at applicants when evaluating potential loans. Factors considered include their potential to make money, their potential to save, and financial responsibility.

“They're able to take out a good quality loan at decent interest rates to make their dreams of working in the U.S. come true,” he said. “They are able to do so without straining their families too much, without going for really high interest rate loans, or without finding other sub-optimal solutions.”

Over the past five years, Stilt has experienced significant growth. Mittal said applications volume grows monthly and loan originations increase by millions of dollars each month. He said 40 to 50 percent of customers return for additional loans. Since Stilt was the one company to loan them money, he added, it has built a trusted relationship with its client base.

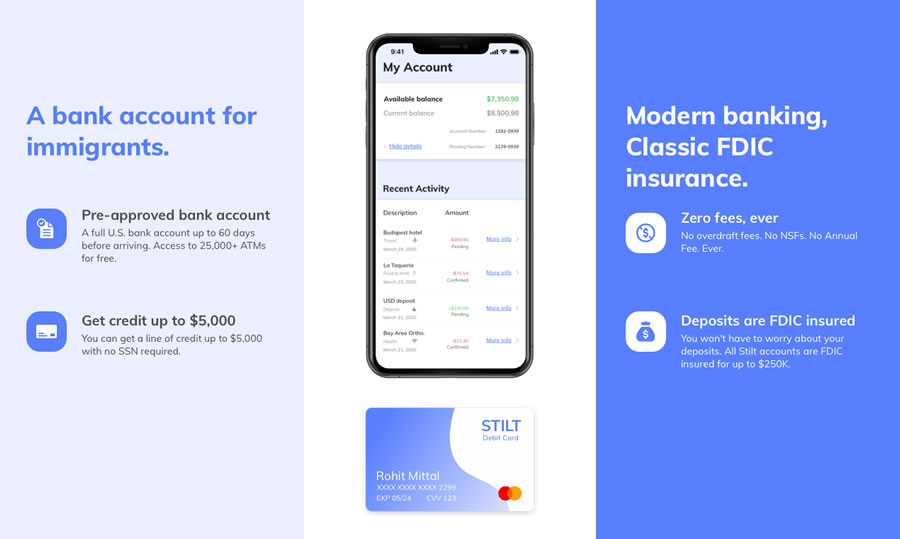

The company is currently developing a bank account program for immigrants and U.S. citizens. Stilt expects offering bank accounts in addition to loans will help it grow faster and help more customers.

“We are trying to democratize access to credit for everyone – including underserved U.S. citizens – and provide them high-quality financial products,” he said. “We’re trying to figure out how we can serve them better, and who else can be served. We learn from our customers every day so we can improve the product and our operations, just to make someone's financial life a little easier.”

Over the long term, Mittal said, the company’s goal is to become THE bank for immigrants and the neglected, underserved U.S. population. The fintech firm plans to eventually add credit cards, mortgages, and other loans, providing provide end-to-end financial solutions that will create lifetime customers.

Despite the company’s progress, easing the financial hurdles faced by the underserved remains a significant challenge that demands solutions across the financial industry, Mittal said.

“It's not just going to be Stilt solving all these problems. It will require a lot of other companies to make sure we build a more financially inclusive, more equal, and more empathetic world for people who are left behind by the current financial system. Our expectation is that with Stilt and some of the companies that we are able to bring together, we can make these customers’ lives a little bit easier than what exists today.

For more information on STILT Inc., visit: Stilt.com