Meet three advocates for special needs financial planning.

They work as financial advisors, but they live as special needs family advocates.

They are the wealth advisors at Burlington, Massachusetts-based Affinia Financial Group – John Nadworny CFP®, CTFA, Cynthia (Cindy) Haddad, CFP®, and Alexandria Nadworny (CFP®, CTFA). Recently interviewed by Advisors Magazine, the multi-generational team expressed that providing a full life for an individual with special needs is paramount. A financial plan – the money part – only goes so far. A comprehensive plan must include the people and support mechanisms for a child with a disability.

Those with a child or sibling with special needs find themselves facing many challenges; among the biggest is financial planning for not one, but two – sometimes more – generations. Caregivers for children with disabilities want to ensure secure financial futures – both for themselves, and for the family members who’ll require care long after.

Affinia Financial Group, LLC provides the typical planning and investment advice, but the lynchpin of the practice is its Special Needs Financial Planning practice. At the heart of the business, it’s a specialty that has been cultivated over some 25 years at other firms, and which now accounts for 65 percent of their business.

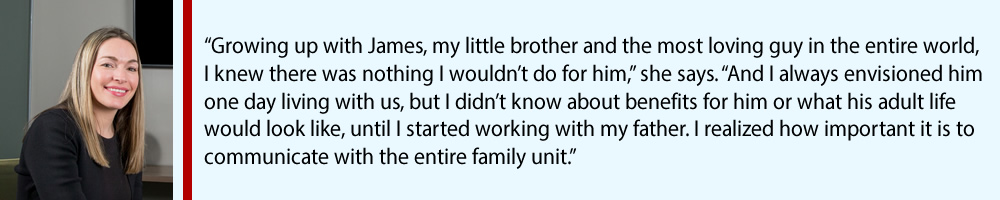

For any advisor, financial or otherwise, client relatability is enhanced when the advisors can walk the walk. John is the father of James who was born with Down syndrome. Alex is John’s daughter, big sister to James. And Cindy’s brother has developmental disabilities. Cindy recalls going to a workshop in her mid-20s with her mother for a session about how to pay for housing for family members with special needs.

Cindy recalls going to a workshop in her mid-20s with her mother for a session about how to pay for housing for family members with special needs.

“The presenter stressed that ‘the magic solution was life insurance,’ and I thought ‘Oh my gosh, that’s not the whole solution, there’s so much more to this,’” Cindy says. “Who’s going to be there? What about government benefits? What about legal assistance, and more?”

She visited a number of financial institutions at the time, driven by the desire to work with just such families. “I was shut down by many, many different companies,” Cindy remembers. “Oh, the state takes care of those folks, or they don’t live that long so why do you have to plan for the future? There’s no money in that,” she was told.

Then she went to a firm and the principle said he didn’t have any clients he knew of that had a child with a disability. “I kept thinking, yes, he does; he just didn’t ask,” Cindy says.

Turns out, at that firm was John Nadworny whose son was born with Down syndrome. That’s how the two were first introduced. They worked at that firm for many years, went to another, and then decided to partner-up and launch Affinia Financial Group in October of 2019.

The vision was to have a multi-generational firm so planning for clients’ futures could continue.

Enter Alex in September 2013.

John points out that he and Cindy have been building the “brand” for more than two decades, but he’s most passionate about their advocacy efforts.

“Once you develop an expertise in an area, it can really have an impact on a system and the way the system works,” he says. “Our goal has always been to do that and it’s like a multiplier effect. There are so many families in need of really good financial advice that it goes beyond one firm like ours being able to serve, and we feel it’s really important that the broader financial community understands some of the intricacies that you need to have in planning.”

A steady stream of educational workshops, conference presentations, newsletters, written- and video-blogs brings the firm’s clients to them.

“Cindy and I set a policy at the beginning – we’ll do a presentation, and then families call or email us. We’ve never had a list of to-call families,” John says.

“We offer different workshops to educate the special needs community as a whole,” Alex adds. “Whether or not someone becomes a client, we think it’s extremely important given our role as family members to pass our knowledge on to as many people as possible, and if there’s a good fit, they will reach out to us.”

Timing is everything

Planning for two or more retirements hinges on strong communication, timing, and prioritizing. Parents that have a family member with a disability still need to plan for all the usual types of financial goals – buying a home, getting other children through college, paying off a mortgage, building up savings, and so on – while also planning for their child with a disability. Helping families navigate certain key milestones led the group to develop their Special Needs Financial Planning timeline. One of the key moments in that timeline is when a parent opts to retire.

Helping families navigate certain key milestones led the group to develop their Special Needs Financial Planning timeline. One of the key moments in that timeline is when a parent opts to retire.

“A lot of the different entitlements that a child receives during their school years end, usually at almost the same time that a parent retires, so they have to think about how they can supplement what the government can provide in addition to what they need for their own retirement expenses,” Alex says adding that a tax-favorable approach is also needed. “In many cases, our families are spending just as much in retirement and it’s really important to have a balance between different types of assets in those retirement years. So, we look at things a little bit differently because of the timelines of families and what types of assets will make the most sense for flexibility purposes as well.”

Families need to be mindful of the rules, and especially whenever there is a change in government services and support, Cindy adds. Age 18 presents a huge change in eligibility for government benefits.

“This would include supplemental security income (SSI), but also making sure that assets are not in the child’s name so they can apply,” she says. Another consideration about this time is the decision-making around guardianship for the child.

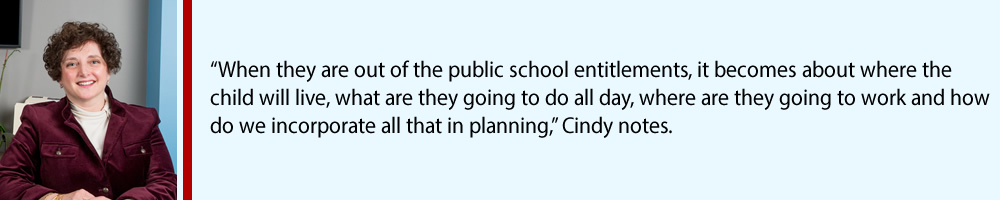

At around age 21 or 22, often as the parents contemplate retirement, the child may be about to lose entitlements from the public school system.

All three advisors understand full well that life can be extremely overwhelming when you have a loved one with special needs. Affinia Financial Group’s strategic timeline helps families to focus on the highest level of priority, and then move on to the next one, and as the process continues, families can feel a sense of progress.

Overlaid with the timeline is the firm’s focus on five factors that are then integrated into financial planning. These are:

• Family and support network factors. “In short, who’s who in the child’s life,” Cindy explains. “And that’s where Alex has been instrumental in helping to build the Team to Carry On™.” This is a trademarked planning service of the firm, which helps answer the parents’ foremost concern: Who will take their place when they can no longer do all that they do? It’s vital to get at the core of a family’s dynamic: considering if there are family members such as grandparents or siblings to help, support agency options, and more. Alex says it’s okay if some siblings don’t want to be involved in a disabled brother or sister’s future. “That’s fine too, because there is always a way to set up the team. And if siblings are looking to be involved, they don’t necessarily need to take on the full brunt of what a parent does,” she says.

• Emotional factors. “This is very important – the denial and acceptance, where are they in identifying all that they need?” Cindy says. Toward this end, the firm helps families create a Letter of Intent. “Only the parents know who’s who, or what their child’s habits and hygiene are, so we created the Letter of Intent to help with the transition around the emotional supports,” she adds.

• Legal factors. This area delves not only into the ADA – the Americans with Disabilities Act – but also all the legal aspects such as types of trusts, particularly special needs trusts, and lays out the specific legal documents families will need – especially for guardianship and alternatives to guardianship.

• Government benefit factors. These address which benefits the child might be eligible for or entitled to, and how they can be protected and maximized.

• Financial factors. Here the firm assesses what tools are available and the best fit. For example, should families use an ABLE account? The Achieving a Better Life Experience Act authorized states to establish tax-advantaged savings programs for persons with disabilities. Life insurance might also be considered, along with virtually any type of savings vehicle to be incorporated into the family’s planning.

For John, Cindy and Alex the practice provides their livelihoods. But the real rewards come with their work around family advocacy. And they are most proud of having been instrumental in shaping policy regarding how services are delivered to families of people with special needs.

For more information on Affinia Financial Group, LLC, please visit: specialneedsplanning.com