A dilemma for government, professionals, and consumers

Studies show that investors cannot tell the difference between fiduciary and non-fiduciary advisors. Here’s our guide to sorting the real deal from a sharp-dressed product-pusher.

Several studies show few investors can spot the difference between a fiduciary advisor’s disclosure and a broker-dealer’s. Investors, however, often fail to realize that the difference eludes them, allowing less-than-forthright service providers to take advantage of clients.

A RAND Corp. study, released earlier this year, bears this out. The study, conducted for the Securities and Exchange Commission (SEC), found that 90 percent of respondents said proposed Form CRS – a draft investor-advisor relationship disclosure document – would help them make informed decisions regarding financial products. In addition, 75 percent reported that the proposed form helped them understand the terms related to conflicts of interest that broker-dealers and advisors may bring to their client relationships. But when put to the test the survey participants, who were interviewed following the questionnaire, showed that they correctly comprehended very little, and large gaps in their knowledge persisted.

“They did not appear to have synthesized the information and be able to apply it,” the study authors reported. “Others seemed to misunderstand the differences between account types and financial professionals from the beginning, never fully grasping it.”

Financial services professionals, too, often define fiduciary differently from each other.

“My clients see me as a truly unbiased advocate,” said Derek Kilgore, a financial representative of Northwestern Mutual Investment Services, LLC. “They trust me because they see that not only am I morally on the right track to make decisions in their best-interests, but legally I am obligated to do so.”

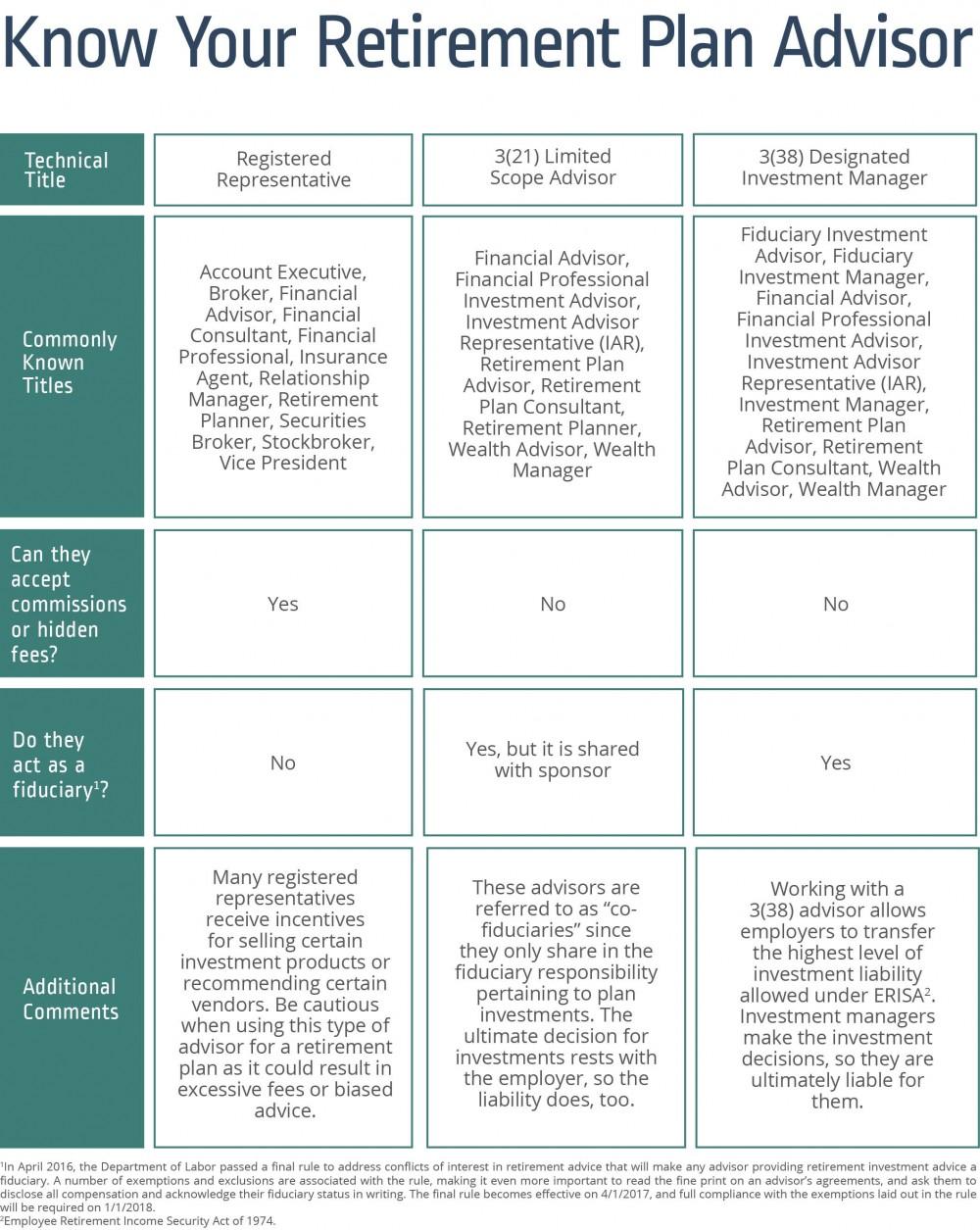

Certified Financial Planners, Registered Investment Advisors, and the Series 65 license all require some form of fiduciary commitment from the professionals who hold those designations. The details can vary, but generally the fiduciary obligation boils down to putting clients’ best interests before the potential payoff from commissions or the impact on firm fees.

“Rather than quote legal jargon … For us it means that you make decisions that are in the absolute best interest of the client,” said Clinton Canon, chief executive officer of Canon Capital Management, Inc., a fiduciary firm that includes an annual fee review for clients to ensure they understand what their fees pay for and why.

“Advisors Magazine” has long asked financial services professionals to define fiduciary. The most common responses given by fiduciaries include putting clients’ interests first, charging fees only, and not holding any vested interest in the products sold to investors. Broker-dealers, meanwhile, tend to follow the less-stringent “suitability” standard – which means that a client can be sold a product so long as it will benefit their investment picture. The product does not, however, have to be the best option available to that client in the marketplace, so proprietary investments, such as some annuities, can be ethically sold according to this standard. The difference between the fiduciary and suitability standards, however, means little if clients fail to comprehend it.

Fiduciary defined.

Defining fiduciary has challenged officials for some time. SEC Chairman Jay Clayton several times has emphasized that fiduciary is a nebulous term, and one that self-described fiduciaries can easily work around. The SEC currently is soliciting feedback on its proposed Regulation Best Interest, which seeks to define the disclosure responsibilities of different financial services professionals; the word “fiduciary” does not appear in the proposal.

The SEC proposal comes after the controversial Department of Labor (DOL) fiduciary rule was struck down by a federal appeals court last year. The Obama Administration pushed the DOL to develop a fiduciary rule after the SEC resisted doing so. The then-incoming Trump Administration delayed the rule’s implementation to 2018, and the Fifth Circuit Court of Appeals struck the regulation down entirely last June. At issue, the meaning of the word fiduciary and the mechanics of compelling everyone from insurance brokers to financial planners to act according to their clients’ “best interest,” which is a difficult-to-define concept. Clayton, in testimony to the Senate, said as much.  “There have been a lot of buzzwords, like fiduciary. Fiduciary can mean a lot of different things in a lot of different contexts. I wanted to make sure we level-set on that,” Clayton said at the annual Financial Industry Regulatory Authority conference last May. He added that fiduciary’s vague definition was the reason the SEC’s proposed Regulation Best Interest’s draft language left the term out.

“There have been a lot of buzzwords, like fiduciary. Fiduciary can mean a lot of different things in a lot of different contexts. I wanted to make sure we level-set on that,” Clayton said at the annual Financial Industry Regulatory Authority conference last May. He added that fiduciary’s vague definition was the reason the SEC’s proposed Regulation Best Interest’s draft language left the term out.

Under “Proposed Rule: Regulation Best Interest,” the SEC would require broker-dealers to put investors’ best interests ahead of their commission concerns or bottom-line. The proposal, however, does not define what best interest means and appears to say that the rule will not be as strict as the fiduciary standard used by Certified Financial Planners and other financial advisors.

Clayton, months later, further explained his comments in a meeting of the Senate Committee on Banking, Housing, and Urban Affairs. During the December meeting, Sen. Elizabeth Warren (D-Mass.) criticized the SEC for hesitating to use the term fiduciary.

“When your own study shows that disclosures don’t work to help regular investors to make informed decisions, will you move away from a disclosure-based approach in your final rule and just adopt a uniform fiduciary standard for both advisors and brokers as Congress instructed in [Dodd-Frank]?” Warren said.

Warren, who officially announced New Year’s Eve 2018 that she is exploring a run for president, backed the implementation of the DOL rule and has repeatedly sought to impose a fiduciary standard. Warren’s office did not return a request for comment by press-time.

Responding to Warren, Clayton said that the fiduciary standard often falls short in protecting investors as advisors can “contract around it” using “informed consent.” Clayton conceded that the SEC still may use the fiduciary for all finance professionals, but that changes would wait until after the public comment period closed.

“While the two standards are based on common principles, under the proposal, some obligations of broker-dealers and investment advisers will differ because the relationship models of these financial professionals differ,” Clayton said during prepared testimony at the meeting. “But – importantly – the principles are the same, and I believe the outcomes under both models should be the same: retail investors receive advice provided with diligence and care that does not put the financial professional’s interests ahead of the investor’s interests.”

“Advisors Magazine” reached out to the SEC for more information regarding fiduciaries contracting “around” their obligations, but the agency did not respond by press-time. Within the fiduciary advisor community, however, some assets do not require the rigorous disclosures afforded to others. Unqualified assets – those which, unlike a 401(k) plan or other retirement account, for example, cannot receive any sort of tax deferments or incentives – were apparently not covered under the DOL’s proposed rule.

“[The DOL rule] only affects the qualified asset base, not the unqualified asset base … It only applies to half their assets,” said Wes Morris, managing member of Morris Financial, Inc. Morris added that he prioritizes investor education so that his clients are aware of how their decisions can affect their finances.

The reality, however, is that even new SEC regulations by themselves likely will do little to improve investor awareness. Even tighter fiduciary rules may still leave investors open to unfair contracts or to advisors with no intention of acting in the client’s best-interest. That begs the question, how can investors protect themselves?

Roles, responsibilities, and titles—how many is too many?

Wealth managers routinely tell “Advisors Magazine” that the industry’s proliferation of titles, licenses, and documents written in legalese can confuse even experienced investors. Not only does the term “fiduciary” lack an agreed upon definition, but so do the wide variety of job titles prospective investors have to wade through when selecting an advisor. Is every service-provider who calls himself or herself a financial advisor or wealth manager really one? No, not always, several long-time wealth managers have said throughout the years.

“These people were selling themselves as investment advisors and they’re just insurance people … We see it all the time, people have been sold [indexed annuities], but there’s nothing backing them up,” said Mark Larsen CFP®, CMFC, founding partner, managing director and chief executive officer of Purus Wealth Management.  Larsen, whose firm is a Registered Investment Advisor, added that many commission-driven brokers provide little, if any, support to clients after making a sale. Many non-fiduciary service providers also possess thin credentials, Larsen said, highlighting how California insurance brokers only need to complete a 52-hour course. Some of these providers then represent themselves to clients as “investment advisors,” and few investors know the industry’s nuances well enough to question these labels.

Larsen, whose firm is a Registered Investment Advisor, added that many commission-driven brokers provide little, if any, support to clients after making a sale. Many non-fiduciary service providers also possess thin credentials, Larsen said, highlighting how California insurance brokers only need to complete a 52-hour course. Some of these providers then represent themselves to clients as “investment advisors,” and few investors know the industry’s nuances well enough to question these labels.

The RAND Corp. study also touches on the confusion caused by the industry’s complexity, stating that “retail investors should not have to parse through legal distinctions to determine” the type of advice they are going to receive.

“Instead, retail customers should be protected uniformly when receiving personalized investment advice about securities regardless of whether they choose to work with an investment adviser or a broker-dealer,” the report states.

Not all advisors agree that its wise – or even possible – to provide uniform protections, however. Many non-fiduciary advisors worry that a uniform standard could expose them to lawsuits. And there is also the possibility that compliance costs will rise and create pressure on current fiduciaries to move upmarket. If fiduciaries move upmarket, investors with fewer assets may find themselves without access to solid financial advice.

“I don’t think that you can make a regulation that forces everybody to put their clients’ best interests at heart. Whatever regulation there is, there will be people that find ways to violate it,” said Victor Connor, CRPS®, WMS, branch manager at Connor Financial Group. “The overwhelming majority of brokers truly have their clients’ best interests at heart … [But] they’re not the ones that make the news.”

The government may justify increased regulation by invoking high-profile cases like that of disgraced investment advisor, Bernie Madoff now serving life in prison for his infamous multi-billion-dollar Ponzi scheme, but many advisors counter that outliers, both good and bad, should not steer the policy debate.

“The target, the playing field is always moving because of that exception, because of that one guy, that one gal who wants to bend the rules or step over the line,” Morris said. “We’re seeing a moving target for guys like me who are doing it the right way.”

Follow the money.

Follow the money.

Investors interviewing prospective advisors for the first time need to ask the right questions. It is said that forewarned means forearmed, but navigating the complex investment landscape requires considerably more forewarning than buying a car, or even a home. Investors need to do their research before they meet with an advisor, understand the differences between the various professional licenses and designations, and know how to spot a vague answer.

Not an easy task, and one that becomes even more difficult when the investor is a first-timer or lacks confidence in their ability to understand financial issues. An advisor who wants to can often get around investors’ concerns with vague or overly complicated answers that leave them feeling overwhelmed. In contrast, an honest advisor is probably going to be open to investor challenges, follow-up questions, and will likely lay everything out in simple language.

“I encourage people, ‘Don’t just talk to just me, there are other good advisors out there, with my firm with other firms that you should probably talk to,’” Morris said. “I have no problem sharing with them that I’m a human being, I make mistakes, and here’s where you can find that I’ve made professional mistakes, which have never hurt the client.”

Many prospective investors approach financial advisors with either minimal, or incorrect, knowledge regarding what a fiduciary does and how they are paid. And many investors can be made vulnerable by the assumption that all financial professionals are fiduciaries.

“I don’t know what clients assume,” said Richard Moran, CFP®, senior financial advisor at Moran, Hesing & McElravey, LLC. Moran said few clients come to him with any understanding of fiduciary.

Moran suggested that new investors need to ask their prospective investor about their experience, credentials, and to explicitly explain the costs involved. Morris, furthermore, said that investors should look to the FINRA website to check advisors’ complaint history and how those issues were resolved.

Following the money is key, many advisors said. If an advisor declines to fully explain how they are paid, investors would be better served elsewhere. Additionally, not relying on the law to provide guarantees remains a prudent choice for investors. Advisors who describe themselves as devoted to the fiduciary mindset all tend to say the same thing: they do it because they want to, not because they have to.

“It’s the unbiased, unwavering, non-apologetic placement of my clients’ interest above mine,” Morris said. “I assured my clients that we’re not going to do anything different because of [the proposed regulation], not that it doesn’t apply to us, but we’re already doing that.”

Questions to ask your financial advisor.

Meeting a financial advisor for the first time can be stressful. It can also be difficult to keep in mind all of the questions you want, and need, answered. The following list was compiled by “Advisors Magazine” after we spoke to more than a dozen financial services professionals and asked them what the best initial meeting questions are. And, if you already are working with an advisor, discussing some of these questions at your next meeting may give you further insight to their philosophy, processes, and what fees you are paying.

1. What is your experience and what credentials do you hold? (again, remember, knowing the differences between the various financial designations is key here)

2. How much would I pay per year for an advisory account? How much for a typical brokerage account? What would make those fees more or less? What services will I receive for those fees?

3. Are there any additional costs that we did not cover in the last question? What are those costs for?

4. Tell me how you and your firm make money in connection with my account. Do you or your firm receive any payments from anyone besides me in connection with my investments?

5. Can you describe to me any conflicts of interest you may possibly have and what your criteria are for determining whether something is, or isn’t, a conflict of interest?

6. What is your investment process? How will you choose the products you recommend to me?

7. Has your firm ever been disciplined? For what type of conduct?

8. Who is the primary contact person for my account, and is he or she a representative of an investment advisor or a broker-dealer? What can you tell me about his or her legal

obligations to me? If I have concerns about how this person is treating me, who can I talk to?