Last April, the Securities and Exchange Commission unveiled a package of disclosure rules targeted at retail investors. The commission has remained silent following the package’s 90-day comment period, but industry insiders tell “Advisors Magazine” the so-called “fiduciary rule” is bound to appear in headlines again, especially after the Department of Labor’s own version was squashed in court earlier this year.

The Securities and Exchange Commission remains quiet about a potentially forthcoming “fiduciary rule” aimed at increasing transparency for retail investors. Advisors across the financial services industry, meanwhile, hold mixed feelings toward the increased disclosure requirements, with some describing the rules as long overdue and others concerned about the impact to smaller, less affluent investors.

“As a fiduciary advisor, we must put your interest ahead of our own. We tell [clients] that disclosures help them identify conflicts of interest, so they are not being left in the dark when it comes to how we advise them,” said George McCuen, president and founder of Napa Wealth Management, adding that while he acts as a fiduciary with his clients, he sees the value in some commission-based services that adhere to arguably weaker disclosure standards. “That’s another business model that, frankly, has its place for investors. If financial advisors that get paid commissions ceased to exist, and investors only could get advice from [fee-only] advisors, a large population of investors that won’t meet the fee-only advisors’ minimums would not be served.”

McCuen, in an interview with “Advisors Magazine,” also noted that some investors — without support from a commission compensated broker-dealer — might turn to new technologies such as the so-called “robo-advisors” or other do-it-yourself investing tools. Many investors, however, would be too risk-adverse to manage their own investments using an online platform, he said, meaning that many would-be investors and retirement savers would simply find themselves excluded.

Other advisors, however, highlighted the benefits fiduciary advisors bring to all clients, regardless of asset level, and the pitfalls of dealing with commission-based broker-dealers.

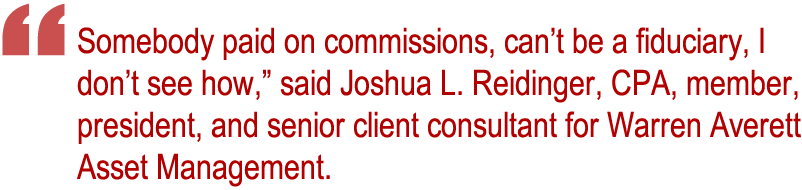

Reidinger added, during a phone interview, that he has recently seen firms selling proprietary products describing themselves as a fiduciary, a problem he described as “disappointing” and potentially harmful to investors. “I’m not casting all non-fiduciaries in a certain light, but I think [fiduciary] is a better solution for clients, I really do.”

The commission unveiled the enhanced disclosure rules last April with Regulation Best Interest comprising the proposal’s core. Regulation Best Interest, in its proposed form, required broker-dealers to “Act in the best interest of a retail customer when making a recommendation of any securities transaction of investment strategy involving securities to a retail customer,” the commission stated in a news release. The release added that Regulation Best Interest made clear that broker-dealers cannot put their own interests ahead of customers’.

The proposal also included a new one-page disclosure document that financial services professionals would be required to use, and restricted use of the term “advisor.”  “The tireless work of the SEC staff has proven to me that we can increase investor protection and the quality of investment services by enhancing investor understanding and strengthening required standards of conduct,” SEC Chairman Jay Clayton said in April. “Importantly, I believe we can achieve these objectives while simultaneously preserving investors’ access to a range of products and services at a reasonable cost. The package of rules and guidance that the Commission proposed today is a significant step to achieving these objectives on behalf of our Main Street investors.”

“The tireless work of the SEC staff has proven to me that we can increase investor protection and the quality of investment services by enhancing investor understanding and strengthening required standards of conduct,” SEC Chairman Jay Clayton said in April. “Importantly, I believe we can achieve these objectives while simultaneously preserving investors’ access to a range of products and services at a reasonable cost. The package of rules and guidance that the Commission proposed today is a significant step to achieving these objectives on behalf of our Main Street investors.”

A similar Department of Labor proposal, floated during the waning days of the Obama Administration, included similar rules but eventually was overturned in court. The DOL rule sparked contentious debate among financial services professionals, with many welcoming the news as good for clients and others concerned that it would pressure advisors to stop accepting smaller investors, or even prompt frivolous lawsuits over reasonable financial plans that simply failed to work out.

The SEC has not released any further statements following the April release, but other news hints at the commission’s mindset.

The SEC, for example, charged a Connecticut-based investment advisory with pocketing hefty commissions off risky investments without disclosing its compensation details to clients. While misrepresentation to clients always has been aggressively pursued by the SEC, the statement that accompanied the charges is telling.

“Investment advisers must put clients’ interests ahead of their own,” said Paul Levenson, director of the SEC’s Boston Regional Office. “[The Connecticut firm] violated that duty by placing clients in risky private placements while downplaying the risk of those investments and concealing the financial conflicts that motivated the recommendations.”

It remains to be seen how the financial services community will react to the SEC’s proposed regulations. The Department of Labor’s rule prompted a backlash, but that was because many wealth managers felt the agency overstepped its boundaries — the DOL had left regulation of financial professionals to the SEC prior to that.

“It really bothered me that the DOL was getting into the business,” Michael B. Keeler, CFP®, AIF®, president and chief executive officer of Peak Financial Solutions told “Advisors Magazine” during the DOL debate. “Let’s do everything through the SEC. I think it’d be great if we could get insurance and everything under one organization so that we’re all playing by the same rules.

The average investor doesn’t understand that this guy’s going to do things one way, and I’m going to do things another way because I’m securities-licensed and that guy’s insurance-licensed.”

The DOL rule was overturned by the 5th Circuit Court of Appeals earlier this year. The rule had garnered the support of organizations such as AARP, the Financial Planning Association, and the National Association of Financial Planners. The U.S. Chamber of Commerce and Securities Industry Financial Markets Association, however, opposed the measure alongside several other trade groups and several, eventually successful, lawsuits were filed to overturn it.

Many financial services firms already act as fiduciaries and use the distinction as a marketing tool. The firms that do, tend to be quick to tell clients. For the firms that already act as fiduciaries, the lack of SEC regulations is a competitive advantage. Other firms, meanwhile, adhere to a fiduciary standard because it improves the client-advisor relationship.

“Some of the things that were instituted for the [fiduciary rule] we are keeping,” said Cathy Vasilev, founding member of Red Oak Compliance Solutions, LLC, a firm that assists wealth managers in complying with regulations. “We’ve kept them even though it’s not required because it’s just a good educational tool that all clients should be provided by their advisor.”

“Within the investments, we really focus on we’re not stockbrokers, we’re not trying to push them into stocks,” said Jeff Brown, president of San Diego-based Brown Wealth Management, adding that his firm explains to clients why working with a fiduciary advisor matters.

“This fiduciary rule came about because so many bankers and brokers took advantage of so many people with variable annuities, for example,” said Brian Decker, chief executive officer of the fiduciary firm Decker Retirement Planning, Inc. earlier this year. “They get paid every year you own that variable annuity. The insurance company gets paid every year … The mutual funds get paid every year you own it. It’s three layers of fees that add up to 5 or 7 percent [annually] before you make a dime.”

“You should be able to have the correct assumption that any advisor working for you is required to have your best interests at heart,” he said, adding that his firm educates clients on the differences between fiduciary and non-fiduciary advisors.

Fiduciary firms’ fee-only model also foregoes considerable earnings to keep clients’ best interests front and center.

“Fiduciaries can only charge fees,” Reidinger said. “If you follow the dollars, generally speaking, there is money being left on the table to be a fiduciary.”