Pandemic moves financial lessons from the classroom to home

The importance of teaching financial literacy to America’s youth has been given a booster shot by the COVID-19 pandemic. April is National Financial Literacy Month and it appears for the second consecutive year, a large portion of school-based financial education programs won’t occur because students aren’t in class.

This worries economic educators and financial advisors who are concerned that missed opportunities for today’s students to learn basic monetary lessons may lead to costly financial errors in decision-making as they move into adulthood.  “Financial literacy and handling wealth wisely doesn’t just impact one person; it impacts entire families and generations after them. It’s something that can literally change destinies,” said Victoria Bogner, CEO of McDaniel-Knutson Financial Partners based in Lawrence, Kansas. “It can change the world for the better if we know how to apply it. But it all starts with education and a knowledge of what is possible, both good and bad.”

“Financial literacy and handling wealth wisely doesn’t just impact one person; it impacts entire families and generations after them. It’s something that can literally change destinies,” said Victoria Bogner, CEO of McDaniel-Knutson Financial Partners based in Lawrence, Kansas. “It can change the world for the better if we know how to apply it. But it all starts with education and a knowledge of what is possible, both good and bad.”

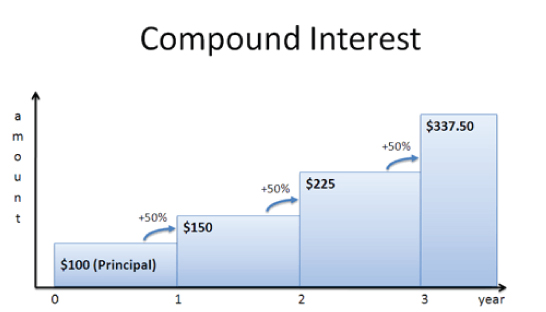

The Value of Compounding Interest

Students might not be in school, but they can still learn a lesson from Dr. Albert Einstein about the power of compounding interest. And it is one parents can teach.

“Albert Einstein called compounding interest the eighth wonder of the world,” said Joshua Simpson, vice president of operations at Lake Advisory Group in The Villages in central Florida. “Learning to use it for your benefit instead of the credit card company’s benefit will only help you.”

Simpson echo’s Einstein who also reportedly said of compound interest, “He who understands it, earns it; he who doesn’t, pays it.”

Here are a few suggestions for parents on how to introduce compounding interest to your kids during the COVID-19 pandemic:

Have the Money Talk

Turn the kitchen table into a short-term classroom by going over the household bills together while passing the potatoes.  Brian Carlson, a wealth manager at GCG Financial in Arlington Heights, Illinois, told the Kitchen Table Economist of TheStreet.com, “The starting point is to have open discussions at the dinner table about financial items. Whether it’s about the groceries, cable bill, mortgage, or even toys, anytime kids hear their parents discussing money, it’s a lesson.”

Brian Carlson, a wealth manager at GCG Financial in Arlington Heights, Illinois, told the Kitchen Table Economist of TheStreet.com, “The starting point is to have open discussions at the dinner table about financial items. Whether it’s about the groceries, cable bill, mortgage, or even toys, anytime kids hear their parents discussing money, it’s a lesson.”

If you have any overdue bills, take the opportunity to show kids the interest rate and the associated dollar amount written on the bill. Letting them see that the extra $20 of interest on a late bill takes away money that could have been allocated to a trip to the ice cream parlor may make an impression on their young minds.

Starting Young

“Financial literacy is important among young teenagers and adults because it is the foundation of making good decisions,” said Mark Cortazzo, senior partner at MACRO Consulting Group in Parsippany, New Jersey.

He goes on to explain: “As a young adult, you have a tremendous amount of human capital that is unharvested and typically very little financial resources. You convert human capital into financial capital over time by making smart decisions such as paying off debt, investing and incorporating tax-smart strategies. The most valuable impact on a young investor’s portfolio is compounding and time.”

So, most likely your 14-year-old is not going to have a need for “tax-smart strategies,” but he or she might want to buy a car in a couple of years. Starting a savings account – one that most likely will include a modest interest rate – is an effective tool to demonstrate how interest on savings adds money to their balance. Even if the interest rate is only two or three percent, your daughter or son will see the benefit of leaving money in the account over time.

“The better they understand the impact of saving early and not getting into debt, the greater the magnitude of the benefit on the tail end,” said Cortazzo.

The Long-Term Value of a Pepperoni Pizza

Sure, that gooey, cheesy large size pepperoni pizza satisfies the taste buds, but it is also a terrific gateway to chatting about finance. Grab a pencil and paper and do some calculating with your children while you wait for the delivery driver to show up. Or cheat like this author did and use an online calculator such as on the one found at www.savings.org.

Grab a pencil and paper and do some calculating with your children while you wait for the delivery driver to show up. Or cheat like this author did and use an online calculator such as on the one found at www.savings.org.

Put that same $20 for the pizza in a three-percent savings account on a weekly basis and leave it there for ten years: Bam, that becomes $12,124.41. How about the same scenario over 20 years? That becomes $28,489.21 or for a 14-year-old now in her or his mid-30s, a sizable down payment on a house.

There is the power of compounding interest. By sticking to the same savings plan for twice as long, one will earn more than double: In this example, a bit more than an extra $4,000.  “Whether it’s using a credit card to pay for a pepperoni pizza, applying for a mortgage to buy a home, or understanding which investments make the most sense, every day we make big and little financial decisions that impact our lives,” said V. Henry Astarjian, managing director of Waterstone Advisors, LLC, located in Walpole, Massachusetts. “Understanding what each decision means for our future is key to staying financially healthy.”

“Whether it’s using a credit card to pay for a pepperoni pizza, applying for a mortgage to buy a home, or understanding which investments make the most sense, every day we make big and little financial decisions that impact our lives,” said V. Henry Astarjian, managing director of Waterstone Advisors, LLC, located in Walpole, Massachusetts. “Understanding what each decision means for our future is key to staying financially healthy.”