The student debt crisis that has saddled millions of Americans with staggering loans can provide opportunities for financial advisors to help families reduce the impact of college financing.

Most mid and upper income families believe there is no alternative to paying nearly full price for private colleges. Fortunately, there are some effective strategies to help. The COVID-19 situation has also surfaced a silver lining to reduce tuition – some welcome good news that advisors can share with their clients.

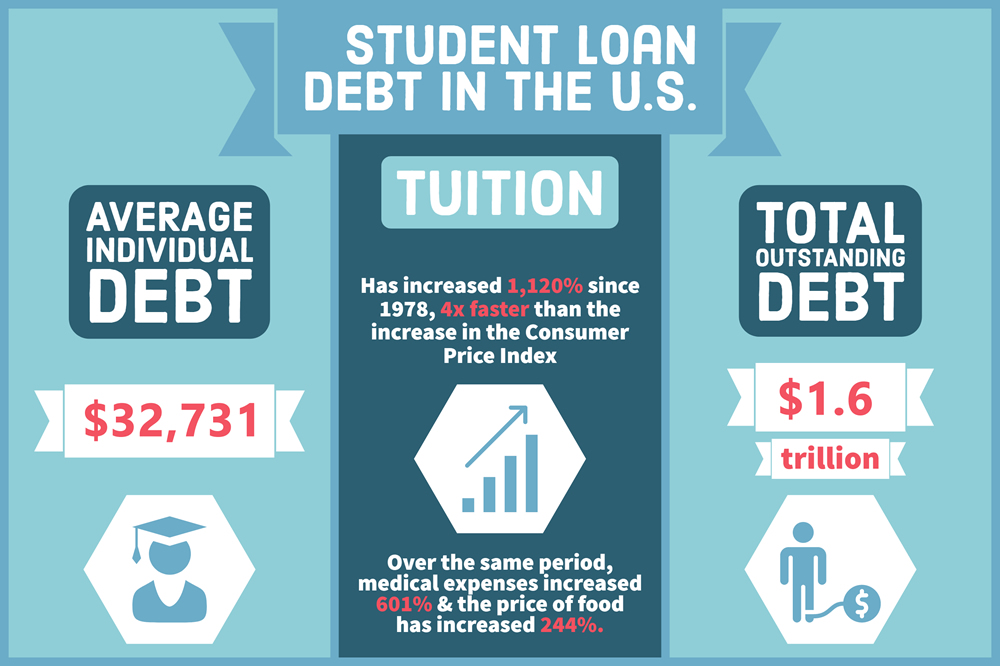

Some 44.7 million U.S. adults (14.4 percent) had student loans averaging $32,731 in the third quarter of 2019, according to statistics from the U.S. Federal Reserve and the New York Federal Reserve. More than $1 trillion of outstanding loans were held by Americans ages 25-49, while 8.1 million people ages 50 and older owed more than $316 billion.

Over the past 12 years, tuition has increased by 63 percent, far outpacing inflation, according to U.S. News and World Report. Another study by industry research firm EAB indicated financial concerns led 40 percent of students to turn down their first choice for college. Sixteen years ago, when CEO Paul Celuch founded College Assistance Plus, based in in Honeoye Falls, New York, U.S. student loans totaled $200 billion. Today it reaches $1.6 trillion. Experts project the sum will pass $2 trillion by 2024.

Sixteen years ago, when CEO Paul Celuch founded College Assistance Plus, based in in Honeoye Falls, New York, U.S. student loans totaled $200 billion. Today it reaches $1.6 trillion. Experts project the sum will pass $2 trillion by 2024.

When financial advisors focus on growing assets under management, they often overlook the impact of college debt, Celuch said. However, those loans can have a significant impact on how much money someone saves for retirement and when they can retire.

Partnering with a college expert to address student debt provides opportunities for financial advisors to expand their businesses among parents and grandparents of high school students, according to John Decker, financial advisors’ liaison and sales consultant with College Assistance Plus.

Reducing Tuition Regardless of Income

Celuch uses a car-buying analogy to help families understand the process. After a student selects their preferred school, the firm recommends applying to competing schools. Students can then use financial offers from those schools to pursue a financial appeal for lower costs at their preferred college. Over the past three years, the firm has helped families land $2.5 million in additional scholarship funding.

College Assistance Plus also tracks the algorithms colleges use to rate candidates. They help students tailor their applications and essays to maximize those factors. The firm also uses videoconferencing technology so students can rehearse for interviews with department heads.

Decker said most people do not realize that they can leverage lower college costs – even well-to-do families. Having worked with 5,000 clients, College Assistance Plus has developed a proprietary database detailing which colleges compete against each other for students based on factors such as geography, diversity, or majors.

Celuch explains that the COVID-19 outbreak is removing many international students from enrollment numbers. As a result, colleges are responding at historically high levels to appeals from high school seniors and current college students.

College Assistance Plus approaches preserving assets “in a different way” than financial advisors, Celuch said. Many people face massive student balances for decades. Those debts can reduce savings or impact the ability to buy a new home. “When you have to sell your house pay back student loans, it’s not a pretty picture,” he said.

Decker noted that College Assistance Plus focuses on taking the emotion out of the college process while getting the entire family on the same page. “Consultants realistically balance the college investment versus the career benefit. Balance those two things and you’ll stop this horrible runaway debt,” he said.

Many financial advisors refer clients to College Assistance Plus as a way to deepen fiduciary relationships while reducing client costs and helping more families, Decker explained. The company also partners with advisors to offer seminars and webinars, helping them meet potential new clients.

College debt is “a hot topic,” Decker added, so addressing the issue helps improve a firm’s financial literacy posture. Advisors are then viewed as people who want to help families educationally. He noted offering assistance with college planning can also draw more people are drawn to a firm’s website.

More than 50 percent of College Assistance Plus’s new clients come from referrals, either by recent customers or, increasingly, from individual advisors. As life expectancies increase, Celuch said, more grandparents are paying for his firm’s services to help their grandchildren. The firm has also begun working with national associations of financial advisors and other non-profits to offer seminars.

Guiding Parents and Students

College Assistance Plus offers programs to help families create a college budget; choose the right schools and majors; prepare for admissions; and make informed financing decisions. Celuch calls the firm’s approach “payment of loans to future income.” The model creates a family budget for college that contrasts the cost of a college education with the expected career income to retire that debt. He added the firm believes that degree/income relationship should be a major factor in how much money a family borrows.

“Your decision on where you should go to school should be contingent on two factors,” Celuch explained. “Do they offer the degree you want? Can you afford to go to that school?” Most people looking at schools do not link the degree with affordability, he explained. His firm helps families understand “you not going to school to get a degree; you're going to school to launch a career.”

The firm’s Career Insight Program helps high school students choose their career before they select a school. The average student changes majors three to four times, Celuch said, and 30 percent drop out in the first two years. The program helps students and parents zero in on the right career before choosing a college.

Celuch said the main insight his firm provides is breaking down financial aid offers to spell out exactly what they mean to family finances. He said colleges and universities use the term “financial aid” for both scholarships and loans. When colleges “say they are going to give you a great financial aid package, 80 percent of it is loans,” he added.

Student loans can impact a graduate’s finances for decades. Parent or grandparents who co-sign loans for their children are also burdened for years. “The pain goes on forever,” Celuch said. “You can’t get rid of these loans, and they cannot be discharged in bankruptcy.” The government can also garnish Social Security benefits to recoup the cost of defaulted loans.

College Assistance Plus strives to bring more transparency to the entire process of financing upper education, Decker added. “I believe we are changing the national conversation about student debt.”

For more information, on College Assistance Plus visit: collegeassistanceplus.com.

You can reach out to Paul Celuch at This email address is being protected from spambots. You need JavaScript enabled to view it. or Advisor Liaison John Decker at This email address is being protected from spambots. You need JavaScript enabled to view it.